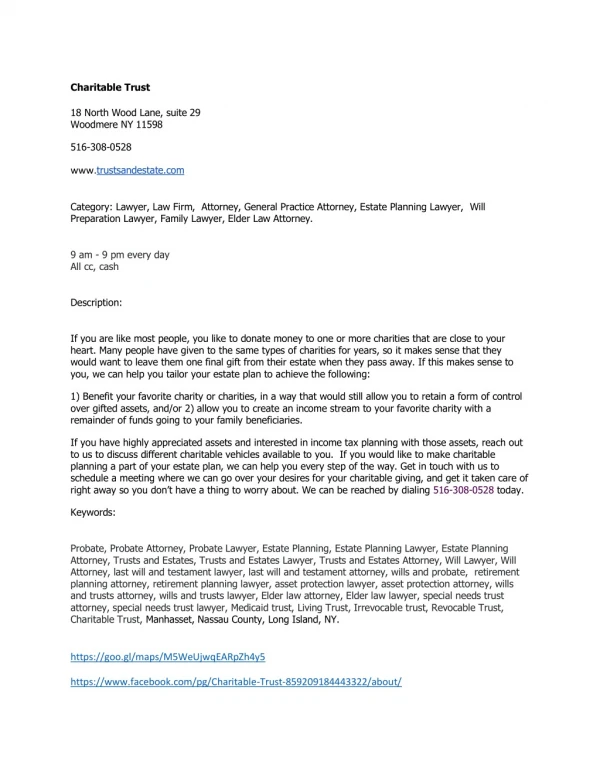

Charitable Trust

If you are like most people, you like to donate money to one or more charities that are close to your heart. Many people have given to the same types of charities for years, so it makes sense that they would want to leave them one final gift from their estate when they pass away. If this makes sense to you, we can help you tailor your estate plan to achieve the following:1) Benefit your favorite charity or charities, in a way that would still allow you to retain a form of control over gifted assets, and/or 2) allow you to create an income stream to your favorite charity with a remainder of funds going to your family beneficiaries.Our team will work with you to make the right decisions based on the amount you want to leave to a charity, and any specific requirements you may have in mind.If you have highly appreciated assets and interested in income tax planning with those assets, reach out to us to discuss different charitable vehicles available to you. If you would like to make charitable planning a part of your estate plan, we can help you every step of the way. Get in touch with us to schedule a meeting where we can go over your desires for your charitable giving, and get it taken care of right away so you donu2019t have a thing to worry about. We can be reached by dialing 212-464-7315 today.

141 views • 2 slides