Download

1 / 17

200 likes | 600 Views

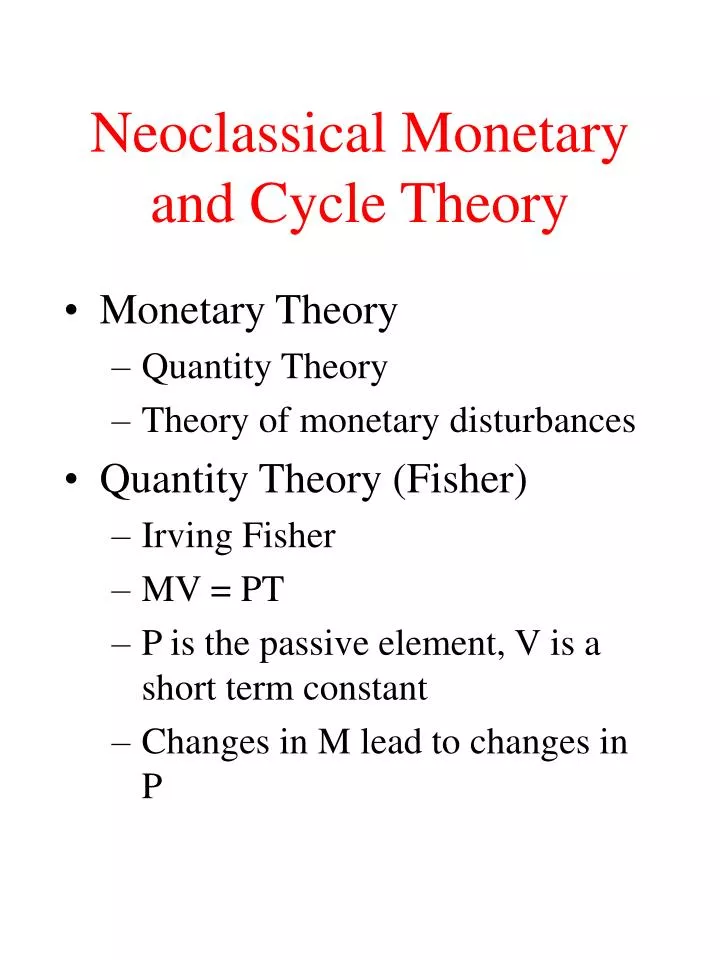

Neoclassical Monetary and Cycle Theory. Monetary Theory Quantity Theory Theory of monetary disturbances Quantity Theory (Fisher) Irving Fisher MV = PT P is the passive element, V is a short term constant Changes in M lead to changes in P. Neoclassical Monetary Theory.

E N D

Neoclassical Monetary and Cycle Theory • Monetary Theory • Quantity Theory • Theory of monetary disturbances • Quantity Theory (Fisher) • Irving Fisher • MV = PT • P is the passive element, V is a short term constant • Changes in M lead to changes in P

Neoclassical Monetary Theory • Quantity Theory (Cambridge) • Cambridge Approach: Marshall • Emphasis on monetary demand or liquidity preference • M = PTk • M is money demand and k represents the demand for money balances as a proportion of the total monetary transactions • Demand for money very largely a transactions demand • Demand for a certain real balance

Say’s Law • Say’s law part of Classical economics, but also adopted by many neoclassicals at least as a long run proposition • Say’s law is the idea that there cannot be overproduction or underconsumption (in general) • Tendency to equilibrium at full employment • Basic idea is that all income will be spent • Savings become investment • People will not (generally) hold money except for transactions purposes

Say’s Law and the Real Balance Effect • Can be departures from full employment equilibrium, but tendency to adjust back to full employment equilibrium • Real Balance Effect (Direct mechanism) • Assume desire for liquidity increases or size of money supply falls • Money demand > money supply • People try to build up their money holdings and aggregate demand falls to below FE Agg supply • Price level declines

Say’s Law and the Real Balance Effect • Fall in price level increases the real value of people’s money balances, reducing money demand • This goes on until money demand = money supply and Agg demand rises back to = Agg supply at FE • Opposite sequence of events if desire for liquidity falls or money supply rises • Also much discussion of other causes of fluctuations or cycles

Wicksell’s Monetary Theory of Cycles • Based on the “indirect mechanism” through which monetary factors might have an effect • Indirect as the mechanism works through the interest rate • Distinction between real and market rates of interest • Real rate of interest equates S and I (based on time preference and real rates of return), but is not directly observable • Market rate of interest set by banks

Wicksell’s Monetary Theory of Cycles • If the market rate is set below the real rate I > S and Agg D > Agg S • Excess of I over private S is being financed by bank lending • This bids up prices and factor incomes resulting in a cumulative upswing for as long as banks continue to lend • When banks run out of excess reserves they will raise interest rates

Wicksell’s Monetary Theory of Cycles • If market rate of interest is set above the real rate S > I and Agg S at FE > Agg D. • This generates falling prices and factor incomes and a cumulative downswing for as long as banks are willing to accumulate excess reserves • For stability need the market rate of interest to equal the real rate of interest

Neo-Wicksellian Cycle Theories: Hawtrey • Hawtrey • Cycles can be explained entirely by monetary factors • Based on the operation of an international gold standard and metallic currencies or paper currencies backed by gold • Period of depression starts with high discount rates, a reduction in the active circulation of gold, and an increase in gold reserves • As gold reserves rise, discount rates fall and have a time of “cheap credit”

Neo-Wicksellian Cycle Theories: Hawtrey and Hayek • Gradual increase in employment and commodity prices • Decline in surplus gold reserves as gold drawn into circulation • Leads eventually to higher discount rates and growing unemployment and falling prices • Hayek • Cycles due to divergences between real and market interest rates • But impact on the structure of production and overinvestment

Neo-Wicksellian Cycle Theories: Hayek • If market rate is below real rate then I > S • Borrowing demand for investment exceeds private saving • Bank lending to finance I bids resources away form consumption goods production • Higher prices for consumption goods leads to “forced saving” • Lengthening of the production period • Goes on until banks run out of excess reserves

Neo-Wicksellian Cycle Theories • This creates a crisis and unemployment • structure of production can only adjust back to compatibility with the level of voluntary savings slowly • People shed from capital intensive industries more rapidly than they can be reabsorbed • For Wicksell, Hawtry, and Hayek monetary factors can affect real variables—more than just price level effects

Schumpeter’s Cycle Theory • Joseph Schumpeter • Cycles due to real not monetary factors • Caused by innovation waves • Innovation in techniques, new trading opportunities, etc • New investment funded by bank credit leads to period of prosperity • Followers less successful and banks run out of reserves • Business failures and depression but a process of weeding out or “creative destruction”

Schumpeter’s Cycle Theory • Role of large firms and the incentive of monopoly profits • Dynamic rather than static efficiency • Schumpeter and the long run prospects of capitalism • Large corporations and the loss of entrepreneurial vitality

Debates Over Savings and Investment • Many of the theories discussed talk about saving and investment, but these terms not always closely defined • Keynes’s Treatise on Money 1930 • Defined I as the value of unconsumed output • S is income less consumption • Focus on price level stability

Saving and Investment • Savings and investment not brought into equality by interest rate adjustments • Investment decisions of entrepreneurs do not automatically match savings decisions by individuals • If I > S price level rises and increases profits and reduces real wages • This transfers income to capitalists with higher propensities to save until I = S

Saving and Investment • Stockholm School • Distinction between planned and actual saving and investment • Ex ante: planned • Ex post: actual • Savings and investment can differ from each other ex ante but have to be brought into equality with each other ex post • If S > I ex ante, retailers find themselves with greater than planned inventories • This brings about a contraction in production until • S = I ex post