Download

1 / 31

330 likes | 492 Views

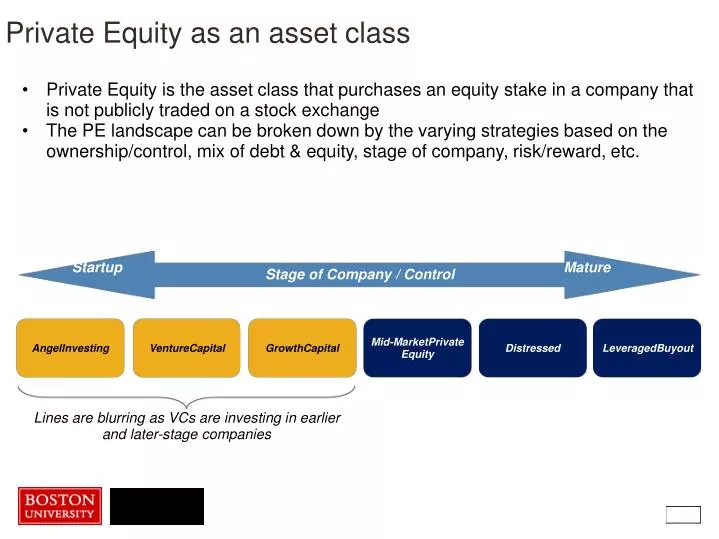

Private Equity as an asset class. Stage of Company / Control. Startup. Mature. Private Equity is the asset class that purchases an equity stake in a company that is not publicly traded on a stock exchange

E N D

Private Equity as an asset class Stage of Company / Control Startup Mature Private Equity is the asset class that purchases an equity stake in a company that is not publicly traded on a stock exchange The PE landscape can be broken down by the varying strategies based on the ownership/control, mix of debt & equity, stage of company, risk/reward, etc. AngelInvesting VentureCapital GrowthCapital Mid-MarketPrivate Equity Distressed LeveragedBuyout Lines are blurring as VCs are investing in earlier and later-stage companies

Background – Mo Yang • •BU SMG Class of 2009 • •J.P. Morgan – Analyst • •Healthcare Investment Banking (NY) • •Cressey & Company LP – Associate • •Private equity firm focused on investing and building leading healthcare businesses • •Successor fund of GTCR and Thoma Cressey • •Based in Chicago, IL and Nashville, TN with over $1bn of committed equity capital Introduction • Background – Carolyn Arida • BU CAS and SMG Class of 2009 • GE Energy Financial Services – Senior Analyst • Domestic Power and Renewables Underwriting • Based in Stamford, CT, with over $20bn of committed debt and equity capital

What is private equity? • •An asset class that consists of equity investments in companies that are not publicly traded • •Investment strategies include: leveraged buyout, venture capital, growth capital, distressed investments, PIPEs, mezzanine capital • •“Private equity” generally refers to later-stage investments • •Typically control investments with management teams as partners • •Private equity firms invest on behalf of Limited Partners (“LPs”) over a 3-7 year investment horizon

How do PE firms generate/realize returns? • •Returns on private equity investments are created through • •Multiple expansion • •Operational improvements – topline growth / margin improvements • •Leverage • •Strategies to drive returns: acquisitions, de-novos, financial engineering, etc. • •Exit strategies: • •Sale to strategic/sponsor • •IPO • •Levered recap

“Mega funds”: Multi-billion dollar funds that invest across all industries • •Invests in mature companies with strong cash flows via leveraged buyouts • •Examples: Blackstone, KKR, Carlyle, TPG, etc. • Middle-market: $500mm to $5bn funds that invest within specific sector or across all industries • •Typically invests in small to mid-cap companies via equity commitments ranging from $25mm to $100mm • •Examples: Advent International, Golden Gate, Avista Capital, HIG Capital, etc. • Growth equity: funds that invest in earlier-stage companies • •Typically invests in smaller targets via platform or “build-and-buy” investing • •Examples: General Atlantic, TA Associates, Summit Partners, etc. • Sector-specific: funds that invest in one or two industries • •Typically middle-market / growth equity or distressed • •Examples: Silver Lake (tech), Lone Star (financials / real estate), Cressey & Co. (Healthcare), Energy Capital Partners (Power) • Financial Institutions: private equity subsidiaries that invest across all industries • •Typically invest in mid-stage to mature companies with commitments ranging from $25mm to $1bn with more of a net income focus than other shops • •Examples: GE Capital, Goldman Sachs, Barclays, etc. Types of private equity firms

“Mega-funds” “Equity check” size Private equity landscape Growth equity Financial institution-backed Middle-market Stage of Company / Strategy Early-stage / Growth Mature / LBO

Private equity market overview Note: $ in billions; excludes venture capital, real estate and other funds • •Need to deploy capital is the big theme in PE • •More demand than supply of assets • •Valuations are being driven higher • •Low PE fundraising activity Note: $ in billions

Private equity market overview • •Investment professionals spending more time on diligence and evaluating investment opportunities vs. fundraising and portfolio company management • •1st half of 2011 activity impacted by volatile credit markets • •Lots of activity expected in 2nd half of 2011 and 2012

Responsibilities of a private equity associate: • •Evaluate new investment ideas (modeling, investment memos, due diligence) • •Perform valuation analyses of potential targets and portfolio companies • •Attend portfolio company board meetings • •Evaluate and manage portfolio company divestiture and acquisition processes • •Execute exit transactions (sale, IPOs, recaps) and acquisitions • •Attend industry conferences and meet with potential target management teams • •Coordinate with portfolio company management, bankers, lawyers, etc. Life of a private equity associate • Lifestyle of a private equity associate: • •Hours: depends on the firm… • •Less structure / more control over hours, deadlines, etc. • •Formal lunches, dinners, etc. • •Traveling

PE associate program overview • •Typically two-year commitment for pre-MBAs • •Some firms offer ability to stay without MBA or return post-MBA • •Ability to co-invest available at certain firms Career in private equity • What do private equity firms look for? • •Most firms typically require background experience in investment banking or consulting for pre-MBAs • •Strong analytical / modeling skills (excel modeling test) • •Excellent communication skills • Life after private equity • •Top-tier business school • •Lateral to other PE shops, hedge funds, etc.

Background – Michael Glick • •BU SMG Class of 2006 • •Merrill Lynch Technology Investment Banking - Analyst • •Safeguard Scientifics – Associate • •58 Year-old Venture Firm Investing in Technology & Life Sciences • •Publicly Traded (NYSE: SFE) • •~$500mm Fund • •Vocap Ventures – Senior Associate • •Newly Formed Early-Stage Venture Fund focused on Software & Internet Companies Introduction

Venture Capital: Subset of The Private Equity Asset Class Stage of Company / Control Startup Mature Private Equity is the asset class that purchases an equity stake in a company that is not publicly traded on a stock exchange The PE landscape can be broken down by the varying strategies based on the ownership/control, mix of debt & equity, stage of company, risk/reward, etc. AngelInvesting VentureCapital GrowthCapital Mid-MarketPrivate Equity Distressed LeveragedBuyout Lines are blurring as VCs are investing in earlier and later-stage companies

What is Venture Capital? Deploys capital directly into private companies to fund growth Value creation vs. financial engineering Purchase a minority stake vs. majority stake VCs take an active role supporting portfolio companies by assisting with: Development of strategy Hiring/building out the management team Making introductions Future financing Tuck-in acquisitions Exit strategy

Venture Capital Investment $ Billions *Source: National Venture Capital Association Yearbook 2010. Includes statistics from the PricewaterhouseCoopers/National Venture Capital Association MoneyTree™ Report based on data from Thomson Reuters.

LPs (Limited Partners) * Endowments, Pension Funds, Fund of Funds Flow of Funds Exits (IPO or M&A) Portfolio Companies VC Funds VC Firms / GPs (General Partners) *Manage Multiple Funds

Profile of 2009 VC Investments: Industry *Source: National Venture Capital Association Yearbook 2010. Includes statistics from the PricewaterhouseCoopers/National Venture Capital Association MoneyTree™ Report based on data from Thomson Reuters.

Profile of 2009 VC Investments: Stage *Source: National Venture Capital Association Yearbook 2010. Includes statistics from the PricewaterhouseCoopers/National Venture Capital Association MoneyTree™ Report based on data from Thomson Reuters.

Stages of Companies Early-Stage Seed: Deployment of a relatively small amount of capital for the entrepreneur / company to prove out a concept before qualifying for Start-up financing Product Development, Market Research, Build Management Team, Develop a Business Plan Start-up: Complete development of product & initial marketing efforts. Technology / product / market risk Growth-Stage Capital for initial expansion – sales & marketing, continued technology development, hiring, and working capital Risk migrates from technology / product risk to execution / market risk Later-Stage After companies have proven their ability to execute at a limited scale they will look to raise a larger round of capital to scale the business while continuing to fund sales & marketing Ultimately this stage of financing should enable the company to position themselves for an exit

Profile of 2009 VC Investments: Geographic *Source: National Venture Capital Association Yearbook 2010. Includes statistics from the PricewaterhouseCoopers/National Venture Capital Association MoneyTree™ Report based on data from Thomson Reuters.

Internet Clean Tech Profile of VC Investments: Internet & Clean Tech *Source: National Venture Capital Association Yearbook 2010. Includes statistics from the PricewaterhouseCoopers/National Venture Capital Association MoneyTree™ Report based on data from Thomson Reuters.

Distribution of FirmsBy Assets Under Management 2009 Profile of VC Firms Summary Statistics $ in Millions *Source: National Venture Capital Association Yearbook 2010. Includes statistics from the PricewaterhouseCoopers/National Venture Capital Association MoneyTree™ Report based on data from Thomson Reuters.

The Exit Funnel:Outcomes of the 11,686 Companies First Funded 1991 - 2000 The Reason To Play The Game: EXITS *Source: National Venture Capital Association Yearbook 2010. Includes statistics from the PricewaterhouseCoopers/National Venture Capital Association MoneyTree™ Report based on data from Thomson Reuters.

Venture-Backed IPOs The Reason To Play The Game: EXITS (Cont’d) # of IPOs Offer Amount ($B) Offer Amount ($Billions) Number of IPOs Year *Source: National Venture Capital Association Yearbook 2010. Includes statistics from the PricewaterhouseCoopers/National Venture Capital Association MoneyTree™ Report based on data from Thomson Reuters.

Venture-Backed M&A(1) The Reason To Play The Game: EXITS (Cont’d) (1) This chart is prepared by analyzing all deals where total venture investment and acquisition price are confirmed. Each deal is classified as a ratio of company acquisition (exit) price to total venture investment from all rounds. This chart compares the number of deals in each category. An acquisition where deal price is less than the total venture investment (“<TVI”) clearly did not result in a good return. Four times the investment to 10 times the investment can be a good outcome. An acquisition for more than 10 times venture investment is usually a nice outcome. *Source: National Venture Capital Association Yearbook 2010. Includes statistics from the PricewaterhouseCoopers/National Venture Capital Association MoneyTree™ Report based on data from Thomson Reuters.

My Stack What Do VC’s Do? • Researching industry trends & opportunities; building domain expertise • Prospecting: Identifying companies of interest to proactively contact • Sourcing • Reaching out to companies proactively or tapping the network to make first contact with CEOs/Companies • Networking with other VCs, law firms, accounting firms, and entrepreneurs 30% Research / Prospecting / Sourcing 25% • Process to determine if the firm should bid (and at what price) on a company/deal: • Relationship building, diligence, deal structuring & returns analysis, firm buy-in, term sheet construction, negotiations • Summary Diligence: Management, Market, Company / Product, Technology, Barriers to Entry, Financials Pre Term Sheet Diligence 10% • The company has selected our firm and we enter into a period of exclusivity where the firm spends a significant amount of time conducting diligence on every aspect of the business before completing the transaction • Full model; transaction memo; legal documents; continued negotiations Post Term Sheet Diligence 15% • Attend board meetings • Support companies with strategy, hiring, future financing, and exits • Ad hoc projects Portfolio Company Support 15% • Fundraising • Reporting on company, deal, and fund performance • Ad hoc projects Internal Projects / Reporting

Recommended Resources Books Venture Deals – Brad Feld The Startup Game – William Draper Mastering the VC Game – Jeffrey Bussgang Done Deals: Venture Capitalists Tell Their Stories – Udayan Gupta Crossing The Chasm – Geoffrey Moore Venture Capital and the Finance of Innovation – Andrew Metrick Venture Capital Due Diligence – Justin Camp News & Other Resources Fortune’s The Term Sheet peHUB.com Business Insider – SAI (Silicon Alley Insider) Techcrunch.com Xconomy.com NVCA.org VC & Entrepreneur Blogs