Download

1 / 9

90 likes | 213 Views

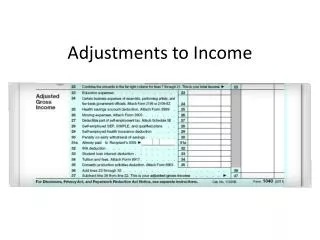

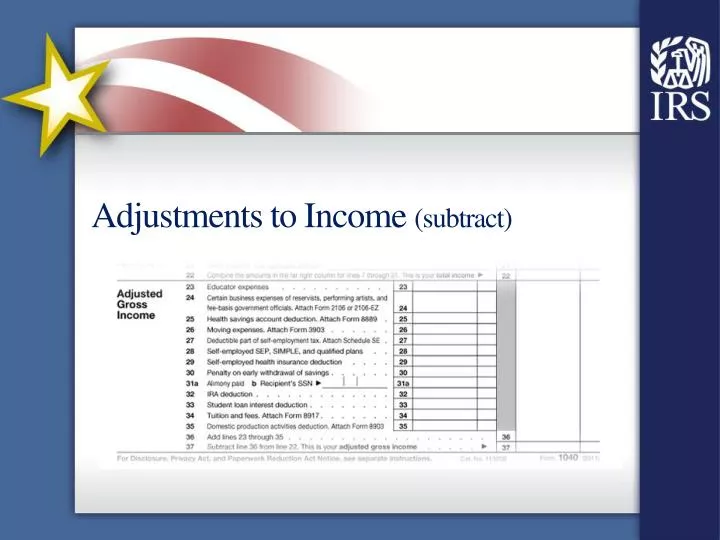

Adjustments to Income (subtract). Key Terms. Adjusted Gross Income (AGI) Alimony Coverdell ESA Modified Adjusted Gross Income (MAGI) Nondeductible Traditional IRA Contributions Qualified Tuition Program Traditional IRA Tuition and Fees . Line 23 - Educator Expenses.

E N D

Key Terms • Adjusted Gross Income (AGI) • Alimony • Coverdell ESA • Modified Adjusted Gross Income (MAGI) • Nondeductible Traditional IRA Contributions • Qualified Tuition Program • Traditional IRA • Tuition and Fees

Line 23 - Educator Expenses • Teacher, instructor, counselor, principal, or aide for grades K-12, employed at least 900 hours are eligible • How much can an educator deduct for 2012? • $250 per eligible taxpayer • Ask the taxpayer if they received reimbursements that would reduce their educator expenses • See Pub 17, Chapter 19, Education-Related Adjustments

Line 28 - Self-Employment Tax • A portion of self-employment tax can be subtracted from income • For 2013, rate = 7.65% (6.20 Social Security; 1.45 Medicare) • The self-employment tax is automatically calculated from Schedule SE

Line 30- Penalties for Early Withdrawal • Form 1099-INT, Interest Income, or Form 1099-OID, Original Issue Discount, document this penalty • The penalty amount is entered on the interest statement in TaxWise

Line 31a - Alimony Paid • Alimony payments: subtracted from income by the payer, reported as income by the recipient • Can be direct payments to the ex-spouse, or payments to cover expenses for the ex-spouse (such as medical bills, housing costs) • Do not confuse alimony payments with child support payments, which are not deductible (and are not taxable for the recipient) • See Pub 4012 (Tab E) Alimony Requirements, the Alimony chapter in Pub 17, and Pub 504, Divorced or Separated Individuals

IRA Contributions • Only contributions to traditional IRAs are deductible • Taxpayers may contribute and deduct up to $5,500 ($+1000 if age 50+) • Contributions cannot be more than taxpayer’s yearly compensation • Deductions can be “phased out” depending on income (MAGI), filing status, and availability of employer-provided retirement plan

Line 33 - Student Loan Interest • Generally the smaller of $2,500 or the interest paid that year on a qualified student loan • Gradually phased out or eliminated based on the taxpayer’s filing status and MAGI • Reported to the taxpayer on Form 1098-E, box 1 Resources • See Pub 4012 (Tab E): • Student Loan Interest Deduction at a Glance • The Effect of MAGI on Student Loan Interest Deduction Chart • See Pub 970, Tax Benefits for Education • Refer to the Student Loan Deduction Worksheet from Form 1040 Instructions or from TaxWise, link to the Student Loan Interest worksheet from Form 1040, line 33

Line 34 Tuition and Fees • Up to $4,000 in qualified tuition and related expenses can be deducted, depending on taxpayer’s filing status, MAGI, and other factors • TaxWise will automatically complete the part of Form 8917 needed to compute the taxpayer’s Modified AGI for this deduction • If taxpayers claim the tuition and fees deduction, they cannot claim the education tax credit for the same expenses • Use the tax benefit that is most advantageous: tuition and fees deduction or the education credit • See Pub 4012 (Tab E) Tuition and Fees Deduction at a Glance, and (Tab 13) Highlights of Education Tax Benefits