Download

1 / 52

520 likes | 664 Views

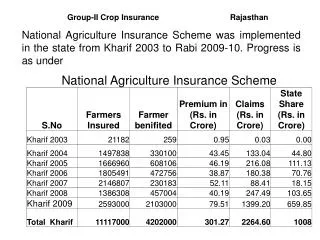

KBC Bank & Insurance Group. 2000 Results. Presentation for financial analysts 5 March 2001. KBC Bank & Insurance Group. Group results and key features Results - Banking Results - Insurance Activities Retail bancassurance Asset management Corporate services Market activities

E N D

KBCBank & Insurance Group 2000 Results Presentation for financial analysts 5 March 2001

KBC Bank & Insurance Group • Group results and key features • Results - Banking • Results - Insurance • Activities • Retail bancassurance • Asset management • Corporate services • Market activities • Central Europe • Strategy • Investor Considerations

Year 2000 Highlights • Net group profits increase : 87.7% (+20.2% excl. gain on CCF) • EPS up : 19.5% (excl. gain on CCF) • ROE increases to 23.3% • Central Europe established as second home market • Strong increase of assets under management • Merger integration progressing as planned • Strategy updated and objectives enhanced

Key Figures In millions of EUR 1999 2000 % Consolidated profit - Group share *excl. gain on CCF -Banking *excl. gain on CCF - Insurance - Holding companyKey figures per share (in EUR)- Net earnings *excl. gain on CCF - Net asset value - Net dividend 969.7 969.7 714.7714.7 271.3 -16.33.263.26 33.8 0.9225 1820.7 1165.5 1520.9876.7 320.6 -20.96.093.90 35.2 1.065 87.7 20.2 112.822.7 18.2 - - 19.5 4.1 15.4

+87.7% 1821 incl. CCF +20.2% +21.6% +12.8% +34% In millions of EUR 23.3% 20.5% 16.1% 16.2% Increased Profitability

Solid solvency ratios 1998 1999 2000 7.4% 12.8% 298% 9.5% 16.0% 307% • Bank • Tier-1 ratio • CAD ratio Insurance • Solvency ratio (1) 7.2% 11.5% 311% (1) excluding unrealized capital gains

KBC Bank & Insurance Group • Group results and key features • Results - Banking • Results - Insurance • Activities • Retail bancassurance • Asset management • Corporate services • Market activities • Central Europe • Strategy • Investor Considerations

BankingSummary In millions of EUR 1999 2000 % Organic % Gross operating incomeGeneral expenses Operating result Value adjustments and provisionsExtraordinary result Profit before tax Taxes Minority interests Profit after tax Profit after tax excl. CCF 3868-2524 1344 -565207 986 -183 -88 715 715 4656-3094 1562 -334693 1922 -243 -158 1521 877 20.422.6 16.3 -41.0- 95.0 32.8 - 112.7 22.7 8.76.5 13.0 -43.0- 26.1 25.3 - - 17.1

BankingIncome Stream +20.4% Total 4656 Total 3868 +9% Total 3435 +37% +31% In millions of EUR +13% % of total income 1999 2000 Other income 8% 8% Commission income 20% 22% Profit on financial transactions 16% 18% Net interest income (incl. dividends) 56% 52%

BankingProvisioning for credit risks In millions of EUR 2000 1999 Specific provisions Domestic International Loan loss ratio Domestic International Gen. prov. for international loans Provisions for country risks Provisions for dioxin crisis -270.4 -103.2-167.1 0.24%0.48% -12.0 -34.0 -25.2 -283.7 -253.0-30.7 0.53%0.09% -24.5 48.0 18.9

KBC Bank & Insurance Group • Group results and key features • Results - Banking • Results - Insurance • Activities • Retail bancassurance • Asset management • Corporate services • Market activities • Central Europe • Strategy • Investor Considerations

InsuranceSummary In millions of EUR 1999 % 2000 Gross marginGeneral expenses Operating result Non-recurring resultExtraordinary result Profit before tax Taxes Minority interests Profit after tax 658-344 312 16-12 316 -41 -4 271 13.78.8 19.1 -- 29.6 80.3 - 18.2 748-374 374 25-5 392 -74 2 321

InsuranceBusiness mix 1999 Gross premiums 2144.5 million EUR 2000 Gross premiums 2704.7 million EUR (+26.1%) group life 4% group life 4% other non-life 8% other non-life10% fire 8% fire 7% accepted business 6% accepted business 8% motor 10% motor 12% individuallife 58% individuallife 65%

InsuranceContribution to recurring result +18.9% Total 371 Total 312 Total 236 +28.4% -3.1% In millions of EUR +37.6% % of total recurring result 1999 2000 Non-technical 22% 23% Non-life 41% 33% Life 38% 43%

KBC Bank & Insurance Group • Group results and key features • Results - Banking • Results - Insurance • Activities • Retail bancassurance • Asset management • Corporate services • Market activities • Central Europe • Strategy • Investor Considerations

+28% 1999 2000 452 353 In millions of EUR 306 -36% +90% +36% 196 +44% 173 148 131 +230% 109 91 91 66 20 % profit contribution 36% 39% 2% 6% 11% 13% 9% 11% 9% 15% 32% 17% Retailbancassurance CentralEurope Corporateservices Assetmanagement Marketactivities Groupitems Profit Contribution by Activity

Retail Bancassurance Overview 1999 2000 • Profit contribution • Allocated equity • Percentage of equity • ROE • Progress in bancassurance and e-commerce • Merger operations on track Prospects 353.2 m EUR 2091.6 m EUR 49.6% 16.8% 452.3 m EUR 2115.0 m EUR 36.6% 21.0%

Retail Bancassurance in BelgiumCross-selling penetration Total clients bank 1 337 204 (=) Total clients insurance 743 716 (+6.1%) 510 896 mutual clients • Cross-selling • 510 896 clients holding at least 1 bank AND 1 insurance product • 32.5% of overall client base • 38.2% of bank client base • 155 750 clients holding at least 3 bank AND 3 insurance products • 9.9% of overall client base • 11.6% of bank client base

planned-408 achieved-165 Merger Process UpdateIntegration of bank branches

E-commerce • Expansion of e-banking & e-insurance a top priority • September 2000 : all retail KBC clients have free access to online Internet banking serviceson request • Mid-September 2000 : launch of ‘My KBC’Internet applications via e-mail, SMS • January 2001 : acquisition of Etrasoft e-commerce trading platform • KBC-Online : • End of 2000 : 90 000 clients • Target by end of 2002 : 300 000 clients

AssetManagementFurther growth in assets under management 69.6 (+34.1%) 51.9 (+41%) 36.8 (+18.3%) In billions of EUR 31.1 % of total AUM 1999 2000 KBC AM ltd. (Ireland) - 12% Private Banking 10% 7% Institutional funds 19% 19% Mutual funds 71% 62%

Asset Management Overview 1999 2000 • Profit contribution • Market share in Belgium,31 Dec. 2000: • Acquisition of UBIM : investment 105 m EUR or 1.35% of AUM Prospects 90.7 m EUR 28.2% 131.2 m EUR 29.2%

Corporate Services Overview 1999 2000 • Profit contribution • Allocated equity • Percentage of equity • ROE • Focus on small- & mid-caps Prospects 109.1 m EUR 1979.5 m EUR 46.9% 5.9% 148.0 m EUR 2188.3 m EUR 37.9% 7.1%

Market Activities Overview 1999 2000 • Profit contribution • Allocated equity • Percentage of equity • ROE • Strong performance by KBC Securities and KBC Financial Products • Acquisition of Peel Hunt key to building European platform Prospects 90.8 m EUR 848.3 m EUR 20.1% 9.8% 172.4 m EUR 557.3 m EUR 9.6% 24.6%

Acquisition of Peel Hunt • Leading UK securities house specialized in small- & mid-caps • Offer price 260 m £ (450 p per share) • Acquisition funded with excess capital • Consistent with strategy to expand corporate finance activities

Central Europe Overview 1999 2000 • Profit contribution • Allocated equity • Percentage of equity • ROE Prospects 20.3 m EUR 603.9 m EUR 14.3% 7.6% 66.3 m EUR 795.1 m EUR 13.8% 10.4%

Central Europe Ownership (*) investmentin millions of EUR market share 213.4 7.2 123.2 Poland Kredyt Bank Agropolisa Warta 49.9% (+1.4%) 49.9% (+26.6%) 40.0% (+40%) 5.8%0.6% 12% 1361.9 11.9 49.0 23.4% 0.5% - Czech & Slovak Rep. CSOB CSOB Pojist’ovna Patria 81.5% (-0.8%) 75.8% (=) 91.9% (+91.9%) 132.1 - 2.5 23.9 8.8% 15.1% 0.5%3.1% Hungary K&H Bank K&H Bank after merger K&H Life Argosz 73.3% (+40.7%) 60% 50% 95.4% (=) (*) change in ownership compared to 1999

IPB • IPB’s assets total 7.5 billion EUR • Assets acquired by CSOB with 100% guarantee from Czech government • 75% of IPB loan book is non-performing • Strong client base (3 million retail clients) • Integration on track • Payment : recapitalization at 7% of RWA +20% • Negotiation to acquire IPB Insurance

KBC Bank & Insurance Group • Group results and key features • Results - Banking • Results - Insurance • Activities • Retail bancassurance • Asset management • Corporate services • Market activities • Central Europe • Strategy • Investor Considerations

Group Strategy • To be an independent, medium-sized bancassurer in Europe. • To achieve high, sustainable growth in shareholder value.

Strategic Focus • Focus on 4 activities • Retail bancassurance • Corporate services • Asset management • Market activities • Focus on Europe • Belgium : home market • Central Europe : second home market • Western Europe : smaller countries/regions, niches. Other regions if higher return than general targets • Focus on ‘local’ clients • Retail • SME

ROE and Capital Allocation • ROE target per activity • Capital re-allocated : activities with low or volatile ROE activities with high or stable ROE Corporate lending - Market activities Retail bancassurance Asset management Corporate finance

Creation of shareholder valueROE Targets per activity MinimumROE target ROE realized Cost of capital Retailbancassurance Corporate services Asset management Market activities Central Europe TOTAL at operational level TOTAL at group level 8.5% 10.5% 8% 11.5% 13% 9.5% - 20.0% 12.5% 13.0% 21.0% 15.0% 17% 22% 21.0% 7.1% - 24.6% 10.4% 17.4% 23.3%

KBC Bank & Insurance GroupOverall financial targets Realized 31 Dec. ‘00 Minimum Target ROE at holding-co. level EPS growth Cost/income ratio bank Combined ratio insurer Tier-1 ratio bank CAD ratio bank Solvency ratio insurer 22% 15% p.a. 55% by 2004 103% by 2004 7% 11% 200% 23.3% 19.6% 64.2% 106.6% 9.5% 16% 307%

KBC Bank & Insurance Group • Group results and key features • Results - Banking • Results - Insurance • Activities • Retail bancassurance • Asset management • Corporate services • Market activities • Central Europe • Strategy • Investor Considerations

KBC Bank & Insurance GroupInvestor considerations • Fundamentals • Strong market shares - diversified income • Unique bancassurance concept • Sound solvency ratios • Strategy • Focus • ROE-based capital allocation • Shareholder-value-driven • Outlook • Merger benefits starting to realize • Central Europe : solid base for expansion • Continued high profitability in niches

KBCBank & Insurance Group 2000 Results Presentation for financial analysts 5 March 2001

Lending Consumer creditMortgages Deposits Savings depositsSavings certificates Mutual Funds Insurance Life (total)Unit-linkedNon-life Market Shares in BelgiumRetail Bancassurance 31-12-00 Dec 99 26.7%25.2% 19.4%17.9% 29.2% 12.8%18.1%8.6% +1.8%+0.9% -0.5% +0.2% +1% +0.9%-1.9%-0.3%

Banking Lending Customer deposits Belgium Abroad Total107.2 Total93.2 Total85.0 Total79.0 Total64.6 +60% Total53.5 +50% -6% +8% In billions of EUR

Banking Asset quality 31-12-98 31-12-99 31-12-00 • Non-performing credits versus total portfolio • Domestic • International (*) • Coverage of non-performingcredits by specific provisions • Domestic • International (*) 1.8% 2.0% 1.3% 67.2% 69.3% 60.9% 2.1% 2.1% 2.1% 64.0% 64.5% 63.2% 2.1% 2.5% 1.7% 67.7% 67.2% 68.6% (*) Excluding the ‘historic portfolio’ of CSOB, which is fully covered by (state) guarantees and provisions.

Efficiency Ratios 31-12-98 31-12-99 31-12-00 Cost / Income ratio Net expense ratio ° Non-life Net loss ratio Combined ratio 60.0% 33.4% 70.0% 103.4% 65.3% 33.6% 72.5% 106.1% 66.5%(*)64.2% 34.0% 72.6% 106.6% (*) excl. impact change in consolidation scope

Insurance Evolution of gross premiums (+56%) (+1.6%) In millions of EUR (=) (+14%)

InsurancePremium distribution by channel Non-life Life In %

KBC Bank & Insurance GroupMerger NPV Total: 1268 mn EUR + 37 % Total: 926 mn EUR Merger NPV better than planned thanks to increased income synergies Cross-selling to CERA clients NPV revised in oct 2000

Merger process updateCreation of the KBC ITplatform on target IT-workload 100% remaining 20% is spread over time to close down old KB system 80% 60% 37% Done 18% 3Q‘99 h100 h200 h101

KBC Group structure Almanij NV Free Float 28.5% 67.8% KBC Bank & Insurance Holding NV 100% 100% 55% KBC Bank KBC Asset Man KBC Insurance 45% As controlling shareholder, Almanij is committed to support KBC

KBC Bank & Insurance GroupGroup key features • Staff: 35 000 • Customers: • in first home market (Belgium): +/- 2.6 million • in second home market (C-Europe): +/- 4.5 million • Branches: • domestic bank branches: 1 454 (KBC+CBC) • independent insurance agents: 765 • International presence: 30 countries As per Dec. 2000

KBC Bank & Insurance GroupKey figures per share 1998 1999 2000 Net profit Net profit (excl. CCF) P/E Gross dividend Pay-out ratio Net asset value Price/NAV 2.69 25.0 1.09 40.6% 32.3 2.1 3.26 16.4 1.23 37.7% 33.8 1.6 6.09 3.90 11.8 1.24 36.4% 35.2 1.3

KBC Bank & Insurance GroupRanking in Europe (*) 15 Soc. Générale 27.8 16 Uni Credito 26.1 17 Abbey Natl 25.4 18 Halifax 24.7 19 Dresdner Bank 23.5 20 San Paolo - IMI 23.4 21 Banca Intesa 23.2 22 Nordic Baltic 23.1 23 Stand. Chrtd 18.0 24 Dexia 17.5 25 Bank Scotl. 15.1 26 Commerzbank 14.8 27 KBC Holdings 14.6 28 Danske Bank 14.2 1 HSBC 133.2 2 UBS 77.3 3 ING 73.2 4 Royal Bnk of Scotl. 63.5 5 Credit Suisse 60.9 6 Lloyds TSB 56.1 7 Deutsche Bank 55.8 8 Barclays 55.4 9 BBV Argentaria 51.9 10 Bco Santander 50.5 11 BNP 40.2 12 Fortis 39.9 13 ABN Amro 36.4 14 Bay Hypo Ver 35.1 (*) 01.03.01 - marketcapitalization in bn. EURO