Download

1 / 36

560 likes | 1.36k Views

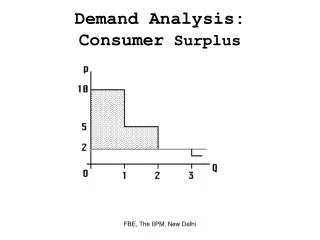

Demand Analysis. By: Prof. Vani Dhawan. MEANING OF DEMAND. Demand signifies the ability or the willingness to buy a particular commodity at a given point of time or at a specified price. Demand for commodity implies on three things: Demand is the desire or want backed up by money.

E N D

Demand Analysis By: Prof. VaniDhawan

MEANING OF DEMAND • Demand signifies the ability or the willingness to buy a particular commodity at a given point of time or at a specified price. • Demand for commodity implies on three things: • Demand is the desire or want backed up by money. • Demand is always related to price & time. • Demand may be viewed ex-ante (before the event) or ex-post (after the event). DEMAND = DESIRE + ABILITY TO PAY + WILL TO SPEND

PRODUCERS’ GOODS CONSUMERS’ GOODS

Durable and Non-durable Goods Consumers’ Durable Consumers’ Non-Durable Producers’ Durable Producers’ Non-Durable

AUTONOMOUS DEMAND DERIVED DEMAND

INDUSTRY DEMAND COMPANY OR FIRM’S DEMAND

SHORT-RUN DEMAND & LONG-RUN DEMAND

Factors Influencing Individual Demand • Price of the Product. • Income of the Consumers: • Normal Goods, and • Inferior Goods. • Tastes & Preferences of the Consumers. • Prices of Other Products: • Substitute Goods, and • Complementary Goods. • Consumer’s Expectations. • Advertisement Effect.

Factors Influencing Market Demand • Price of the Product. • Distribution of Income & Wealth in the Community. • Community’s Common Tastes & Preferences. • General Standards of Living & their Spending Habits. • Future Expectations. • Inventions & Innovations. • Fashions. • Climate or Weather Conditions. • Customs. • Advertisement & Sales Propaganda.

LAW OF DEMAND • It is the functional relationship between the quantity demanded of a particular product and its price in the market. The equation can be written as: • Statement of the Law: According to Alfred Marshall The law of demand states that, “ ….. The amount demanded increases with a fall in prices & diminishes with a rise in prices.” Qdx = f (Px)

Assumptions of the Law • Law of Demand based on fundamental assumption ceteris paribus (i.e; other things remains the same) are as follows: • No change in Consumer’s Income. • No change in Consumers Tastes & Preferences. • No change in the Prices of related Goods. • No change in Fashions. • No change in Government Policy. • No change in the Distribution of Income & Wealth. • No change in Weather Conditions.

Cont………. • DEMAND SCHEDULE :: • A Tabular Statement of price or quantity relationship is called the demand schedule. • It shows the quantity of goods that a consumer would be willing and able to buy at specific prices under the existing circumstances. • DEMAND CURVE :: • A Graphical presentation of a demand schedule is known as demand curve. • It expresses the relation between the price charged for a product & the quantity demanded , holding constant the effects of all other variables. Individual Demand Schedule and Curve. Market Demand Schedule and Curve.

Individual Demand Schedule & Demand Curve D Price D Quantity Demanded

Market Demand Schedule & Demand Curve DD is the Market Demand Curve , which is the summation of all individual demand curves. D D

Why does the Demand Curve Slope Downwards from Left to Right ??

Exceptions to the Law Of Demand (Upward Sloping Demand Curve) • Giffen Goods. • Speculation. • Articles of snob appeal (Expensive Commodities). • Consumer’s psychological bias or illusion. • Goods with no substitutes. D Price Demand

ELASTICITY OF DEMAND • Alfred Marshall defines:: “The Elasticity of Demand in a market is ………. Great or small according to the amount demanded………... Increases much or little for a given fall in price, and diminishes much or little for a given rise in price.” Elasticity of Demand = % age Change in Quantity Demanded % age Change in Determinant of Demand

PRICE ELASTICITY OF DEMAND • Price elasticity of demand is a measure used in economics to show the responsiveness of the quantity demanded of a good or service to a change in its price. Price Elasticity of Demand = Proportionate Change in Quantity Demanded Proportionate Change in Price • Types of Price Elasticity of Demand:: • Perfectly Elastic Demand. • Perfectly Inelastic Demand. • Unitary Elastic Demand. • Relatively Elastic Demand. • Relatively Inelastic Demand

1. Perfectly Elastic demand When the demand for a product changes …… increases or decreases even when there is no change in price, it is known as perfect elastic demand. e = ∞ Price D D Q Q’ Quantity Demanded

2. Perfectly Inelastic demand e = 0 When a change in price …… how so ever large or small, there is no change in quantity demanded, it is known as perfect inelastic demand. D Price P’ P D Quantity Demanded

3. Unitary Elastic demand When the proportionate change in demand is equal to proportionate changes in price, it is known as unitary elastic demand. D e = 1 Price P P’ D Q Q’ Quantity Demanded

4. Relatively Elastic demand When the proportionate change in demand is more than the proportionate changes in price, it is known as relatively elastic demand. D Price e > 1 P P’ D Q Q’ Quantity Demanded

5. Relatively Inelastic demand When the proportionate change in demand is less than the proportionate changes in price, it is known as relatively inelastic demand. D e < 1 Price P P’ D Q Q’ Quantity Demanded

INCOME ELASTICITY OF DEMAND • Income elasticity of demand measures how much the quantity demanded of a good responds to a change in consumer’s income. Income Elasticity of Demand = Percentage Change in Quantity Demanded Percentage Change in Income • Types of Income Elasticity of Demand:: • Unitary Income Elasticity. • Income Elas. Greater than Unity. • Income Elas. Less than Unity. • Zero Income Elasticity. • Negative Income Elasticity.

1. Unitary Income Elasticity e = 1 When an increase in income brings about a proportionate increase in quantity demanded, then it is known as unitary income elasticity. D Income Y’ Y D Q Q’ Quantity Demanded

2. Income Elasticity Greater than Unity e > 1 When an increase in income brings about a more than proportionate increase in quantity demanded, it is known as income elasticity greater than unity. D Income Y’ Y D Q Q’ Quantity Demanded

3. Income Elasticity Less than Unity e < 1 When income increases ….. quantity demanded also increases but less than proportionately, it is known as income elasticity less than unity. D Income Y’ Y D Q Q’ Quantity Demanded

4. Zero Income Elasticity e = 0 When quantity demanded remains the same……even though income increases, it is known as zero income elasticity. D Income Y’ Y D Quantity Demanded

5. Negative Elastic demand When there is increase in income……then quantity demanded falls, it is known as negative elastic demand. D e < 0 Income Y Y’ D Q Q’ Quantity Demanded

CROSS ELASTICITY OF DEMAND The cross elasticity of demand or cross-price elasticity of demand measures the responsiveness of the demand for a commodity to a given change in the price of some another commodity. Cross Elasticity of Demand = Percentage Change in Quantity Demanded of X Percentage Change in Price of Y

1. Substitute Goods A substitute good is a good with a positive cross elasticity of demand. This means a good's demand is increased when the price of another good is increased. For example: Tea and Coffee e > 0 D Price P’ P D Q Q’ Quantity Demanded

2. Complementary Goods A complementary good is a good with a negative cross elasticity of demand. This means a good's demand is increased when the price of another good is decreased. For example: Bread and Butter. D e < 0 Price P P’ D Q Q’ Quantity Demanded

3. Unrelated Goods e = 0 The unrelated goods have zero cross elasticity of demand. This means a change in the price of one good has no effect on the demand of another good. For example: Razor Blade & Petrol D Price P’ P D Quantity Demanded