Download

1 / 36

370 likes | 542 Views

Competition. First, the Economist’s View. Market Structure Continuum. Monopolistic Competition. Perfect Competition. Kinked Demand. Monopoly. Oligopoly. Many Buyers. Many Sellers. Few Sellers. One Seller. Small Sellers. Large Sellers. Large Seller. Homogeneous Product.

E N D

Competition First, the Economist’s View

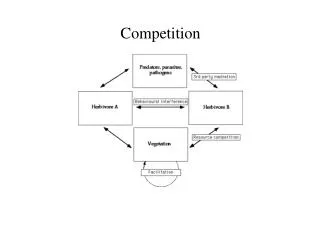

Market Structure Continuum Monopolistic Competition Perfect Competition Kinked Demand Monopoly Oligopoly Many Buyers Many Sellers Few Sellers One Seller Small Sellers Large Sellers Large Seller Homogeneous Product Some Differentiation Unique Product Some Barriers Free Entry & Exit Strong Barriers Perfect Information Price Taker Price Searcher Impersonal Competition Personal Competition My Market LR Π = 0 LR Π > 0

1.Many Small Buyers 2.Many Small Sellers 3.Homogeneous product RESULT 4.No Barriers to Entry 5.Perfect Information No market power on the buying side Many alternative vendors No product loyalty (very elastic) EXTREMELY ELASTIC DEMAND Price Taker (takes price as given) Profits will induce entry Losses will induce exit Zero economic profit in Long Run No mis-steaks (oops, no mistakes) Perfect Competition IMPLICATION: Firm & Market have different elasticities. Separate Firm and Market graphs needed

Firm • Firm (assumed to be one plant for simplicity) • Cost curves • Profit maximizes at Q where • Marginal Revenue = Marginal Cost • Given Price (assumed fixed), sets Quantity • Determines profit and whether to produce

Industry • Collection of individual buyers determine Demand • Collection of firm decisions determines Supply • Equilibrium price set where Quantity demanded = Quantity Supplied • Total Equilibrium Quantity set • For Competition, Firm assumes market results as given • Need • One graph for industry (to set market price) and • One graph for firm (to set quantity for typical firm)

The Role of Price • Rationing– • chase low-valued-use customers away • Allocate (scarce) resources to “best” use • Allocation - • Move resources from surplus markets to shortage markets • Result: The Invisible Hand Independent Individual Actions in Response to Incentives • Resources used where most valuable • By those valuing the use the most

Market and Firm :Competitive Industry/MarketLong Run Equilibrium Market Firm P P S MC ATC P=Dfirm=MRfirm P1 AFC TFC AVC D TVC Q Qfirm Q1 Q1 firm

Competitive Firm with profit P MC P=Dfirm=MRfirm π ATC TFC AVC TVC Q Qfirm MC = P => Qfirm Profit (Π) = (P-ATC) x Q Creates incentive for entry of new firms

Competitive Firm with a Loss P MC ATC AVC Π(negative) P=Dfirm=MRfirm TFC TVC Contribution to Overhead Qfirm Q MC = P => Qfirm Profit (Π) = (P-ATC) x Q < 0 Creates incentive for exit of new firms

Competitive Market and Firm:Effect of a Demand Increase Market Firm P P P2=D=MR S1 S2 MC P2 ATC π P1=Dfirm=MRfirm P1 TFC TVC D2 D1 Q Qfirm Q1 Q2 Q3 Q1 firm D increase MC = P2 => Qfirm rises Q2 firm Industry P and Q increase Profit (Π) = (P-ATC) x Q rises Firm’s Demand (P) Rises Creates incentive for entry of new firms Entry occurs until Long Run is re-attained. Π=0

Competitive Market and Firm:Effect of a Demand Decrease Market Firm P S2 P S1 MC ATC P=Dfirm=MRfirm P1 Π(negative) P2 P2 TFC TVC D1 D2 Q3 Q2 Q Qfirm Q1 Q1 firm Q2 firm D decrease MC = P2 => Qfirm falls Industry P and Q decrease Profit (Π) = (P-ATC) x Q falls (< 0) Firm’s Demand (P) Falls Creates incentive for exit of firms

Market Adjustments • Short Run • Industry price adjusted to get Qs = QD • Firms raise or lower Q to equalize MC = P • Profits or Losses are earned • Long run • Firms respond to Profits (enter) or losses (exit) • Price adjusts to change in supply • Firms adjust to new price • Eventually π = 0 and entry or exit stops

Competition Implications • Long Run Profits are zero • Due to entry and exit • Maximum surplus (producer + consumer) • Price serves as signal for resource allocation • Presumed when “invisible hand” invoked • May not give “best” distribution or output • Public goods, externalities, equity

Inter-industry Adjustments • Profits draw firms into industries decreasing profits for firms already in industry • Losses drive firms out increasing profits for those remaining • Relative profitability may attract firms from one industry to another • Toys-r-us (according to Jay Leno) says it may sell its toy business (??) • Risk differences (etc.) may leave some differences in profitability across industry

Efficiency (Presumes Competitive Market)

Efficiency • Cannot help one without hurting another • If Marginal benefit > Marginal cost, • increase output • If Marginal benefit < Marginal cost, • decrease output • Efficiency<=>Marginal Benefit=Marginal Cost • In markets happens at D,S intersection • Efficiency is most output, given input • Equity is “fairness”

Why and How Efficiency? • Why? • Maximum surplus • Buyers and Sellers satisfied • Why is market equilibrium best? • The following affect output => efficiency down • Price ceilings • Price floors • Taxes and Subsidies • Monopoly • External benefits and costs (effects on others: e.g., pollution) • Price vs non-price allocation

Efficiency, graphically P Consumer Surplus S Benefit for which the consumer does not pay. P1 Producer Surplus D Revenue without associated opportunity cost. Q Q1

Effect of a Tax on Efficiency This is called dead weight loss because these (not produced) units are more valuable than their cost. That is, lost benefit without saved cost. S + tax Consumer Surplus P S Tax P2+tx Tax Revenue Deadweight Loss P1 Notice price consumer pays goes up (P1 to P2 + tax) P2 Producer Surplus Notice price supplier receives goes down (P1 to P2) D Q Q2 Q1

Monopoly The Firm as Market

Many Small Buyers One Seller “Unique” product RESULT Barriers to Entry Perfect Information No market power on the buying side No alternative vendors No close substitutes LESS ELASTIC DEMAND Price Setter (must choose price) Profits will not induce entry Losses will not induce exit No mis-steaks (oops, no mistakes) Monopoly IMPLICATION: FIRM IS MARKET (one graph)

Monopoly decision process • Profit maximization • Marginal Cost = Marginal Revenue • Recognize effect of price on quantity demanded • MC = MR < P (society’s value of product) • Sources of Monopoly Power • Control of resources • Government intervention • Economies of Scale • Network economies (first mover, setting the standard)

Decision Process • How Much? • MC = MR => Q* • Given Q*: • P set on demand curve at Q* • Ave. Total Cost determined from ATC at Q* • Ave. Var. Cost determined from AVC at Q* • Ave. Fixed Cost = ATC – AVC at Q* • Whether? • If Price > Ave. Var. Cost at Q*, net cash flow + • So produce—better off producing than not

Marginal Revenue for Monopoly • MR = ΔTR/ΔQ =revenue change per unit added Net change in revenue is blue box minus yellow ΔTR= P x ΔQ (+) + Q x ΔP (-) MR = {20 x (40-20) + 20 x (20-30)}/(40-20) = 10<20 = {40 x 20 – 30 x 20}/20 = 10 Price Revenue at higher price 30 (-) Revenue at lower price 20 (+) Revenue received at either price D MR 20 40 Quantity

Profit Maximization for Monopolistic firm Contribution Margin Monopoly Qfirmbased on MR = MC P P1 => max, given Qfirm MC TR = P1 x Qfirm P1 Notice: Q set using only marginals π ATC ATC1 ATC1, given Qfirm TFC AVC AVC1 TR AVC1, given Qfirm TVC = AVC1 x Qfirm TVC MR D TFC = (ATC1 - AVC1) x Qfirm π (profit)= (P1 – ATC1) x Qfirm Qfirm Q Because of barriers to entry, these profits can persist.

Monopoly with a Profit P TC=TFC+TVC TR = P x Q Π = TR – TC = TR – TVC - TFC MC P1 ATC π ATC1 AVC TFC TVC D MR Qfirm Q

Monopoly with a Loss Still wanting to Produce P Π < 0 MC ATC ATC1 P1 AVC TFC Contribution to overhead. TVC MR D Qfirm Q

Monopoly with a Loss Wanting to Shut Down P MC ATC1 ATC Π < 0 AVC TFC AVC1 NegativeContribution to overhead. P1 TVC D MR Qfirm Q

Effect of Monopoly on Efficiency Monopoly Qfirmbased on MR = MC P P1 => max, given Qfirm MC Notice: P and Q set using only marginals P1 P1 is value of last unit sold MC @ Qfirm is the cost of the last unit sold. P>MC @ Qfirm so society loses this surplus As long as P>MC, surplus exists MR D Lost surplus is the triangle Qfirm Q Dead Weight Loss Notice that Setting P=MC (competitive result) will cause no lost surplus

Natural Monopoly πMon The key issue is the size of the firm relative to the market. P LMC PMon Economies of Scale are significant Preg LAC ATC1 Demand is such that only one firm has room to be profitable. MR D πReg Profits would occur without regulation QReg Q Qfirm Profits would attract entry => both firms would lose money Rate regulations gives exclusive right to one firm, keeps price down, Increases Q, & assures π

Price Discrimination • Separable Markets • Otherwise, people will buy in one market and well in the other. • Different Elasticities • Otherwise, there is no advantage to price discrimination • Raise price in inelastic (P insensitive) market • Lower price in elastic (P sensitive) market • Until MR is the same in each

Price Discrimination: Movies Adults Kids P Lower maximum price P Kids are distinguishable PAdults Demand more elastic PKids MC D D MR MR QKids QAdults Q Q Construct MR (MR <P) for each segment in same way as monopoly Assume constant Marginal Cost for simplicity. Find Qfirm as we always do => MC = MR for each section of market Set Price based upon Qfirm and the relevant demand curves. Notice: PAdults > PKids because adult Demand less elastic

Competition The Practical Aspects

Competition Basics • Know your competitors (knowledge) • Selectively communicate • Preannounce price increases • SHOW willingness to defend • Educate competitors (not worth price war)

When to Compete • Cost competitive advantage • Niche (claim the whole niche) • Complementary products • VERY Elastic market

To React or not to React • Think Long Term • Is there a better response than price? • If not: • Focus on @ risk customers • Focus on incremental value • Focus on competitor’s high margin area • Raise cost to competitor (educate his/her cust.) • Second round? • Is it worth it? • Mk Share worth Saving?