Download

1 / 7

70 likes | 242 Views

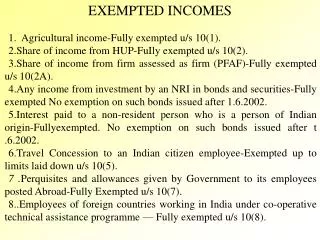

Incomes exempt from tax. Incomes exempt under section 10. Agriculture income [sec 10.1] Receipts by a member from a HUF [Sec10.2]..example Share of profit from a partnership firm [sec 10.2a] Casual (5000) and non recurring receipts [sec 10.3] Interest to non-residents [sec 10 4, 4b]

E N D

Incomes exempt from tax Incomes exempt under section 10

Agriculture income [sec 10.1] • Receipts by a member from a HUF [Sec10.2]..example • Share of profit from a partnership firm [sec 10.2a] • Casual (5000) and non recurring receipts [sec 10.3] • Interest to non-residents [sec 10 4, 4b] • Leave travel concession to an Indian citizen[sec 10.5] • Value of concessional passage to foreign national employee • Remuneration received by a foreign diplomat and other foreign nationals • Remuneration of a technician in India • Salary received by a ship’s crew • Remuneration of a foreign trainee • Exemption from tax paid on behalf foreign companies in respect of certain income • Tax paid on behalf of non residents/foreign companies in respect of other income

Technical fees received by a notified company • Foreign allowance • Income of a foreign govt. employee under cooperative technical assistance programmes • Remuneration or fees received by non resident consultants and their foreign employees • Income of a family members of an employee serving under a cooperative technical assistance programme • Gratuity • Pension and leave salary • Retrenchment compensation • Compensation received by victims Bhopal gas leak disaster • Compensation on account of any disaster • Payment from an approved public sector company and other entities at the same time of voluntary retirement • Tax on perquisite paid by employer • Amount paid on life insurance policies • Payment from provident funds

House rent allowance • Payment from an approved superannuation fund • Special allowances • Income received as exchange risk premium • Interest on securities • Lease rent of aircraft • Educational scholarship • Daily allowance of Members of parliament • Awards • Pension to gallantry award winners • Exemption of family pension received by the family members of armed forces • Former rulers of Indian States • Income of local authority • Income of housing authority • Income of Scientific research association • Income of educational institutions • Income of hospitals

Income of specifies news agencies • Income of games associations • Income of professional institution • Income received on behalf of Regimental Fun • Income of fund established for welfare of employees • Income of pension fund • Income from khadi or village industries • Income from khadi or village industries Boards • Income of statutory bodies for the administration of public charitable trust • Income of European Economic Community • Income of SAARC • Income of Insurance Regulatory Authority • Income of certain National funds, educational institutions and hospitals • Income of a mutual fund • Income of investor protector fund • Income of Venture Capital fund or venture capital company • Income of an infrastructure capital fund • Income of trade union

Income of provident funds • Income of Employees State Insurance fund • Income of a member schedule Tribe • Income of resident of Ladakh • Income of a “sikkimese” individual • Income of an agricultural produce marketing company • Income of National Minorities Development and Finance Corporation • Income of Ex-servicemen • Income of Minor • Subsidy received by planters • Capital gain on transfer of US 64 • Long term capital on transfer of listed equity shares • Income of notified non profit body

Special provisions in respect of newly established undertakings in free trade zone • Special provisions in respect of newly established undertakings in Special Economic Zone • Special provisions in respect of newly established hundred per cent export oriented undertakings • Special provisions in respect of artistic hand made wooden articles