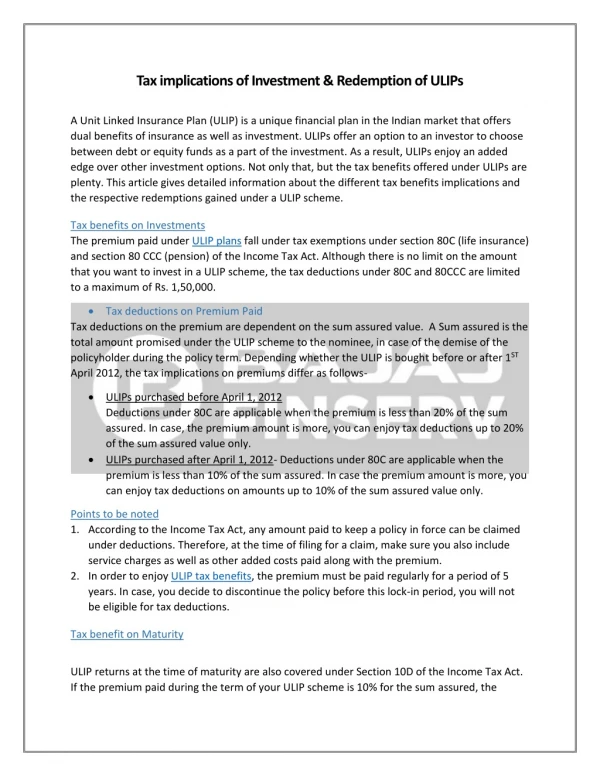

Download

1 / 45

460 likes | 652 Views

Behavioral Theory and Investment Implications. Cem Demiroğlu Serdar Sayman. “Seyir Defteri” of the Presentation. Differences between classical investment selection and behavioral theory, and issues with the mean-variance analysis

E N D

Behavioral Theory and Investment Implications Cem Demiroğlu Serdar Sayman Koç University

“Seyir Defteri” of the Presentation Koç University Differences between classical investment selection and behavioral theory, and issues with the mean-variance analysis Behavioral biases, concepts, and heuristics that are associated with individual investors’ investment selection Criticisms of behavioral theory The influence of demographics, culture, and media on investment selection Implications for the YKB’s “Seyir Defteri” project Koç University 2

Role of behavioral theory Behavioral decision making recognizes and builds on the fact that economic behavior and decision making is subject to emotions, biases, and irrationality. Role of behavioral theory • in developed markets, understanding the clients’ needs and what drives their behavior service quality • in Turkey, help more clients have investment options other than deposit accounts Koç University

Classical theory of investment selection(mean-variance analysis) efficient investment opportunity set (efficient frontier) EXPECTED RETURN Low risk aversion High risk aversion 1. desired rate of return? 2. important to have quick access to money? 3. maximum risk to take? Optimal risky portfolio T-bills RISK (σ) Koç University Koç University 4

What is wrong with mean-variance analysis? Koç University Equity Premium Puzzle? Equity premium: difference between return on stocks and the return on a risk-free asset Equity premium is too large as per standard economic models (Mehra & Prescott, 1985) [ one explanation: Myopic loss aversion ] Risk? Considers only the standard deviation (is not concerned with the shape) Asset allocation puzzle? Two-fund separation theorem (Tobin) suggests that investors should only differ in terms of the fraction of risk-free assets not in terms of the mix of risky assets. In practice, however, mix of risky assets are adjusted • ignores behavioral biases

Expected Utility Theory (EUT)? Koç University Expected Utility Theory is the standard rational theory of decision under risk derived from a set of assumptions (completeness, transitivity, continuous, independence) These assumptions are shown to be violated form of utility function is understood as the “risk preference” a recent paper by Rabin shows that diminishing marginal utility of wealth cannot explain risk aversion

Standard vs. Behavioral Theory (or Finance) Koç University Risk attitude - gain vs. loss against a reference point - different risk attitudes in gain (+) and loss (-) domains - loss aversion (different slopes in (+) and (-) domains) Integration of assets / mental accounting (across which diversification may not be optimally adjusted) Definition of risk difference to the investor’s reference point?

Heuristics, Biases, Concepts Information processing Decision evaluation Information selection Decision • Recognition • Representativeness • Extrapolation • Anchoring • Reference effects • Framing • Probability weighting • Overconfidence • Illusion of control • Affect, mood • Mental accounting • Endowment • Status Quo bias • Familiarity • House money effect • Disposition effect • Ambiguity aversion • Self attribution bias • Hindsight bias • Regret avoidance • Time inconsistency Koç University Availability

Availability Bias Koç University Individuals judge the relevance of information depending on how easy it is to recall it. e.g. which of the following increased the life expectancy in the US more? A: antibiotics B: refrigerator e.g. in 12 months which one is more likely? A: stock market crash B: bond market crash e.g. stocks in the news, stocks with extreme short term returns overreaction but the price is likely to come down experienced investors are less likely to purchase due to attention • Show long-term results to discourage from jumping on recent news.

Recognition heuristic Koç University If one of two objects is recognized, infer that it has a higher value under certain conditions knowing less and recognizing some options may be beneficial Gigerenzer & Todd (1999) report a study where stock portfolios are chosen based on recognition of laypeople and experts; these portfolios outperformed mutual funds, market indices and portfolios of unrecognized stocks. … majority of sophisticated experts perform worse than the market. Warren Buffet (1987) : “the only value of stock market forecasters is to make fortune tellers look good”

Representativeness and Gambler’s Fallacy Koç University Representativeness:individuals estimate probabilities depending on prior beliefs e.g. current assets of a company is twice its liabilities, equity is equal to debt, share price equals book value, reports of serious management inefficiencies. which is more likely? A: value stock B: value stocks that go bankrupt believe that small samples represent bigger sets (populations) e.g. assume that a fund manager beats the market in 2 out of 3 years. Which sequence is more likely? BLBBB or LBLBBB

Representativeness cont’d Koç University Gambler’s fallacy:individuals misperceive randomness • Recent occurrence of an outcome increases the odds that the next outcome will be different: e.g. people avoid a lottery number that was a winner in the recent few days. but in Turkey, a newspaper reported the most common winning numbers before the New Year’s lottery. • When prices move modestly, investors buy at dips and sell on rises. Hot hand fallacy or trend-chasing: or ignore the random aspect of an event • When prices start fluctuating or exhibit trends, investors switch to trend-chasing Trend chasing is likely to be more dominant in Turkey given the volatility of market prices. but trading on momentum is not easy • increased flow into funds with exceptional short term performance; part of performance is random. Advise clients to invest after waiting a reasonable time

Extrapolation Koç University Base decisions on recent events or heavily rely on certain facts and ignoring some other relevant information Mainly due to cognitive errors Assuming most recent trends will continue (good or bad)

Anchoring Koç University Anchoring: people’s assessments can be influenced by quantities mentioned in the problem statement, even though the quantity is not informative. e.g. - would Dow Jones be above or below 6500 at the end of the year? - would Dow Jones be above or below 8000 at the end of the year? following the above, each group is asked their guess of the index Anchoring may lead to underreaction (conservatism), if investors are influenced by initial or current value as anchors. e.g. abnormal earnings news is not quickly incorporated into the stock price • if there are changes in fundamentals, make sure that the client’s expectations respond

Reference effects Koç University utility or value is based on gain / loss with respect to a reference point not simply the absolute level of the payoff. It is important to understand to what extent investor compares investment’s return with the market or alternative products not chosen. If the alternative products perform better, people experience regret. Multiple reference points are possible (initial price aspiration level) • RMs should make sure that they only offer the client a limited set of products with similar payoff characteristics to prevent future regret and dissatisfaction

Framing Effects Koç University Alternative descriptions of a problem lead to different preferences e.g. 600 people affected by a hypothetical deadly disease: • option A saves 200 peoples' lives • option B has a 33% chance of saving all 600 people and a 66% possibility of saving no one. 72% of participants chose option A Another group of participants chose between: • option C in which 400 people die • option D has a 33% chance that no people will die but a 66% probability that all 600 will die. 78% of participants chose option D • Show an alternative frame / representation to see whether the decision changes

Probability weighting weight of probability probability such a favorite long shot bias can be observed in derivatives markets • advise investors a fund consisting of “favorites” Koç University Long-shots are valued “more” Favorites are valued a little too little

Overconfidence Koç University People believe that their knowledge is more accurate (or skills are better) than it actually is e.g. better than average effect: everyone is a better than average driver e.g. miscalibration effect …

Overconfidence: e.g. Miscalibration Trivia Quiz: For each of the following 10 items, provide a low and high guess such that you are 90% sure the correct answer falls between the two. Your challenge is to be neither too narrow (i.e., overconfident) nor too wide (i.e., underconfident). If you successfully meet this challenge you should have 10% misses-that is exactly one miss. Low High 36 6590 12 90 3476 179 1756 610 9588 11033 Koç University

Overconfidence - cont’d excess trading can be explained by overconfidence -- who trade most makes the least (Barber & Odean, 2000) incompletely informed players makes worse than uninformed players (Huber, 2006) Koç University Gallup survey on 1,000 investors, asked the investors how much they thought the market and their personal portfolios would rise over the next 12 months (Fisher & Statman, 2002):

Illusion of Control Koç University Belief that people can favorably influence chance events e.g. people value lottery tickets that they choose more than the ones given to them • could we make investors to choose from a small set alternatives, rather than offering one suggestion? is it a good idea to

Affect, Moods, and feelings Koç University • People who are in a good mood are more optimistic about their choices • Anger is found to increase risk seeking • Offer clients new products when the weather is good, after their favorite team wins an important game etc. • help the client to avoid spontaneous trades

Mental Accounting Koç University process referring to organize, evaluate and keep track of decisions and payoffs implicit methods to code and evaluate financial outcomes e.g. better to integrate a loss into a big gain. people prefer to have retirement payments withdrawn from salary, as opposed to paying separately • clients should not focus on loss from one fund / vehicle, make them focus on the gains from the whole portfolio

Endowment effect Koç University individuals value an item more when it is part of their assets. willingness to accept (selling price) is more than the willingness to pay (buying price) research suggests that endowment effect is not applicable for assets owned for trade purposes in the first place. may explain the disposition effect (discussed later) and why investors may not part easily with stocks they inherited this tendency can be explained by “omission bias” as well

Status Quo Bias Koç University people tend not to change an established behavior unless there is strong incentive can be explained by loss aversion and endowment effect e.g. invest only in time deposits e.g. many people refuse to exchange lottery tickets for an equivalent one + cash regret aversion, and habitual adherence to self imposed rules may also play a role

Familiarity bias Koç University • Investing in what you are familiar with • Most investors think that companies that they don’t know are riskier • So, they invest in companies that: - they work for (bad idea for diversification purposes!) - they are customers of - are located close to where the investor lives Home Bias: French & Paterba (1991) find that about 90% of investors in USA, UK, and Japan invest in their own respective country • Providing a firm’s home base in addition to name increases investment to it does it makes sense to provide names & places of firms in fund? • show the benefits of international diversification

Previous Wins / Losses? Koç University House money effect • Greater willingness to gamble with money recently won. • So, approach the client for selling riskier products (that are also more lucrative for YKB) right after the client’s portfolio produces good returns. • At the same time people tend to become more risk seeker as they lose e.g. long-shot horses are bet on more later in the day as losses slowly accumulate

Sell Winners Early, Keep Losers(Disposition Effect) Koç University people hold on to losing positions for too long. Can be explained by - loss aversion: when in the loss, investor becomes risk seeker and accepts further gambles - mental accounting: if sold, a “paper loss” becomes a real loss and it is recognized - sunk cost effect: cannot see the fact that the purchase price is bygone • If explained a client may be convinced and sell off losing positions -- may even invest in riskier products to make up for earlier losses. • Frame the sales as “transfer your assets” (Gross, 1982)

Ambiguity Aversion Koç University • People prefer a gamble with known probabilities to an equivalent gamble but with unknown probabilities (ambiguity) A: urn contains 50 red 50 white balls B: urn contains 100 red and white balls with unknown numbers you win if the drawn ball is red. would you play A or B? (Ellsberg’s paradox) • People prefer gambles that give them a sense of understanding and competence. • People perceive gambles that they don’t understand well as riskier. • Training the client about the risk-payoff structure of potential products will increase his likelihood of trading. SHOW THEM the risk information, not just boundaries…

Self Attribution Bias Koç University People tend to attribute good outcomes to own abilities and bad outcomes to external circumstances Overconfidence + self attribution self deception • $1 invested in Microsoft’s IPO in 1986 is worth roughly $350 today -- an annual return of roughly 125% (or 12 times the historical average annual return of S&P 500). People who invested in Microsoft’s IPO brag about their investment skills, but most just got lucky. • Enron’s market cap plummeted from above $60 billion to almost nothing in less than 2 months. Investors who got burned defended themselves by arguing that “no one could have seen it coming”. • Might provide interesting insights in understanding RM-client relationships • Record how the decision is made, and RM’s role

Hindsight bias • Past events seem easy to predict after the fact “How could I have been so stupid?” • We have selective memory of our past thoughts and feelings that led us make a certain decision • Peaks and dips seem obvious after the fact and we wonder why we did not see them coming • record the information context, risk and chances when a decision is made, and recall later Koç University

Regret Aversion (Avoidance) Koç University Some investments “leave a bad taste in the investor’s mouth” and they never want to make similar investments to avoid experiencing the same bad feeling For example, an investor who invested in the stock market just before a market crash might never want to come back to the market even after the market recovers The investor rationalizes why he should not invest in the stock market, although he should not focus or put too much weight on a particular outcome

Time inconsistency - Intertemporal effects Koç University Discounted Utility Theory (intertemporal version of EUT) involves constant discount rate, or exponential discounting. However some studies suggest declining impatience -- discount rate decreases as the time period is further in the future (as judged from the present) e.g. a client buys a contract to pay (5, t1) for receiving (6, t2) when t1 comes the idea may seem as a bad one

What is wrong with behavioral theory? Koç University Does not always explain when a particular bias / behavior is prevalent Small changes in the context / problem description may lead to different results Apparently different characterizations may be offered for the same context e.g. investors may be overconfident and ignore probability of loss or give over weight to a low probability event ? Criticized as not being coherent

Demographics Koç University In order of importance in affecting trading: Age Income level Gender Occupation Marital status Family size Educational background

Age Koç University Young investors… prefer assets with capital gains (e.g., growth stocks) while old investors prefer assets with regular distributions (e.g., dividend paying stocks, bonds) are more optimistic about pre-tax returns that they can attain with their portfolio. more strongly believe that future stock prices are predictable reveal greater willingness to take risks in their financial investments. hold less diversified portfolios. hold a smaller fraction of their personal assets in common stock portfolios.

Income level Koç University Investors with high regular income … prefer assets with capital gains and not those with distributions are more likely to have multiple brokerage accounts spend more time conducting investment research trade (slightly) more hold more diversified portfolios invest a smaller fraction of their wealth in common stocks

Gender Koç University Relative to women, men … are less likely to select assets with regular distributions rely less on broker advice and more on personal analysis tend to exhibit more “overconfidence” spend more time on investment analysis have more brokerage accounts trade more

Culture Koç University Culture can influence - risk attitude - probabilistic thinking - overconfidence Individualistic cultures overconfident, self attribution, but better in probability calibration Collectivist cultures influenced by framing, hindsight bias more risk seeker, better in detecting associations / correlations Ambiguity aversion is linked to culture (Gupta, Hanges, Dorfman 2002) equity premium is higher in countries where ambiguity aversion is higher Loss aversion is lower in Turkey compared to the average of 50 countries

The effect of media in feeding these biases Koç University

Implications for the YKB project Koç University The first step in changing the client’s trading habits is to educate and familiarize him about the new products being offered by YKB. Explain to the client why sticking with past investment habits might not be in his best interest going forward. Providing education through a trustworthy individual or someone that the client likes and respects increases the chances of success in changing the client’s habits. Along similar lines, make sure that the client likes and trusts the RM that he works with. Rather than imposing a particular product to the client, give him (a narrow set of) alternative options and allow him make choices out of alternatives. Survey and the relevant offer would help reduce the impression that advise received from the bank is arbitrary Just like many banks would offer different recommendations, RMs probably give different recommendations or in different ways; this initiative may reduce variation.

Attention, memory, ease of processing • Habitual adherence to self-imposed rules • Helps economize on thinking. • Example: Consume only out of dividend payments but not price appreciation • Halo effect • Causes someone who likes an outstanding characteristic of an individual to extend this favorable evaluation to the individual’s other characteristics. • Example: Continue to work with an unsuccessful RM because he is a good guy. • Example: Investing in a stock because you ideologically agree with the CEO. • Illusion of truth • person is more likely to consider a familiar statement as true than an unfamiliar one • can occur without explicit knowledge (even when it was previously told that it was “false”) Koç University

Koç University • Social Interactions • People often take an investment in their radar screen or trade based on suggestions from friends and family. • When clustering clients it might be worthwhile trying to assign them into various social networks.

Investor performance Koç University A 20 year study conducted by Dalbar, Inc. finds that individual investors underperform the S&P 500 Index by 6.5% and inflation by 1%. Any explanations? They buy high and sell low (unsuccessful market timing) “Buy-and-hold” investors earn more than those who try to time the market

Most retail investors don’t understand the riskiness of their investment choices Koç University