Download

1 / 13

130 likes | 303 Views

Commercial Banks: Ownership Commercial Banks are owned by private investors, called stock holders Or by companies called bank holding companies. They are sometimes owned by the government (especially in third world countries).

E N D

Commercial Banks: • Ownership • Commercial Banks are owned by private investors, called stock holders • Or by companies called bank holding companies. • They are sometimes owned by the government (especially in third world countries) • According to holding company banking system , a group of banks are brought under • One centralized management and this centralized management exerts control over • All the units. • Although each bank has got a separate entity, its affairs are controlled by a holding • Company .

Principles of Banking: • Profitability: The objective of profitability should be tempered with caution • and prudence • 2) Liquidity: A banker should take necessary steps to keep its fund liquid. By • liquidity we mean the capacity to produce cash on demand. But liquid cash • does not earn anything and remains idle. • The conclusion is that commercial bankers, while employing their funds, should • pay attention to both profitability and liquidity. A wise policy would, therefore, be • to follow a golden mean to earn profits without sacrificing the need for keeping • a reasonable amount of liquid assets.

Items on the asset side of the Balance Sheet of a bank: • Cash in hand: it also includes cash reserve at the central bank and money deposited • In other banks. This is the most liquid asset. A banker should try to minimize cash • Holding . • Money at call and short notice: this item represents money lent to other banks which • are recoverable either on short notice or on demand. This assets is advantageous • Than cash reserve. • Bills discounted : it is a highly earning liquid asset. It has got a fixed maturity and • it is less risky • Loans and advances: Loans and advances are the most profitable assets of a bank. • The loans can’t be easily recalled . • As a rule of thumb the bank should lend only for short term commercial purposes. • Because there should be a problem of maturity matching.

Services rendered by banks I) Collection of deposits and lending: It is the fundamental function of a bank There are various types of deposits Demand deposit /Current account : It can be withdrawn on demand at any time and in any amount up to the full amount. It is generally a non interest bearing account. They provide perfect liquidity. Savings Accounts: This account pays interest to the depositor, but have no specific maturity date on which the funds need to be withdrawn or reinvested. Time deposit: It is such type of deposit on which the depositor and bank have agreed that the money will not be withdrawn without substantial penalty to the depositor before a specific date. These are known as FDR (Fixed deposit receipts). Time deposit require a minimum deposit amount.

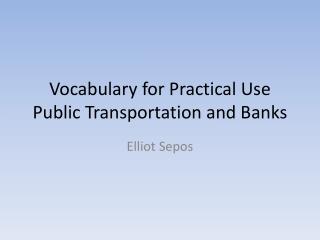

ii) Cash management and other services: This include cheque cashing , foreign currency exchange, safety deposit boxes, Electronic wire transfer (TT). iii) Letter of credit service/ Foreign trade financing A LC is a guarantee issued by a banker , authorizing some other banker , to whom It is addressed, to honor the cheques or a bill of a person named in the document , to the extent of a stated amount. vi) Agency Services: Dividend collection, manager to the issue, rents and collection of cheques v) General Utility services: vi) Safe deposit of valuables:

vii)Credit cards: Users are issued with a credit on production of which their signature is accepted on Bills in shops participating in that scheme. The banks guarantee to meet the bill and Recover from the cardholder. viii) Online banking: Online banking enables the banks to accept deposits or honour customer cheques at The counter of any of the bank’s branches regardless of the branch with which he or She maintains the account. ix) Collection of cheques through clearing houses: X) Information and other services: Many banks acts as a major source of information on overseas trade . Some banks produce regular bulletin on trade and economic conditions at home and abroad, Special reports commodities and markets.

1. Purchase Order Exporter Importer 5.Shipment of goods 6.shipping documents & time drafts 4.L/C notification 2.L/C application 4.4 3. L/C Bangladeshi Bank (Importers bank) Indian Bank (Exporters bank) 7. Shipping documents &Time draft Draft accepted (B/A Acepted)

Financial Systems of Bangladesh • The formalfinancial sector in Bangladesh is comprised of • Bangladesh bank -------- The countries central bank • b) Commercial banks • Commercial banks can be categorized in three groups • Government owned nationalized commercial banks (NCB 4 ) • Domestic private commercial banks (30) • Foreign banks (10) • c) Government owned Development financing institution (5) • 2 industrial finance companies, BSB, BSRS, Basic Bank • One house building finance companies. (HBFC) • One employment generation bank . ( Karma Sangasthan Bank) • d) One Government owned investment company (ICB) • e) Finance and Leasing company (28)

Closely related to financial sector are an assortment of insurance companies and • Two stock exchanges at Dhaka and Chittagong. • Among other players most important are the 150 micro finance institutions. • The prime micro finance institution is Grameen Bank, • Bangladesh Rural Development Board (BRDB), • Palli Karma Shayahak Fund (PKSF), • Bangladesh Rural Advancement Committee (BRAC), • Association for Social Advancement (ASA) And Proshika • The MFI’s play an important role in the financial sector especially to meet • the need of the rural and poor people.

Micro Finance Institutions A MFI form a group of village people, encourage the group to make small weekly savings , supplement these savings with MFI’s own funds and arrange disbursements through the groups to pursue one or other income generating activities on the basic coverage of recommendation of the group. The borrowers are required to repay the loan in small installments at short intervals, usually a week. In 2003-04 Grameen bank and other three big NGO’s disbursed a sum of tk 7600 crores. Banking Coverage Two clearly distinct trends are seen between NCB and PCB in terms of their outreach and nature of lending. One is ,NCB’s maintain branches throughout the country in urban as well as in rural areas, the PCB’s operate mainly in urban areas. Again Dhaka accounts for bulk of shares of the country’s financial resources.

The other is the NCB’s mainly lend to relatively unremunerative and relatively risky Socio economic sub sector , often at the behest of the government. The PCB’s concentrate primarily on financing trade especially foreign trade and working capital for industries • After it’s independence Bangladesh started with only 6 nationalized commercial • banks (NCB), a few Development financing institution and a handful of foreign • bank branches..