Download

1 / 1

10 likes | 167 Views

Jeremy A. Woods 1 , Hanqing Fang 2 , Esra Memili 3 , Renyong Chi 4 , & Daniel T. Holt 5.

E N D

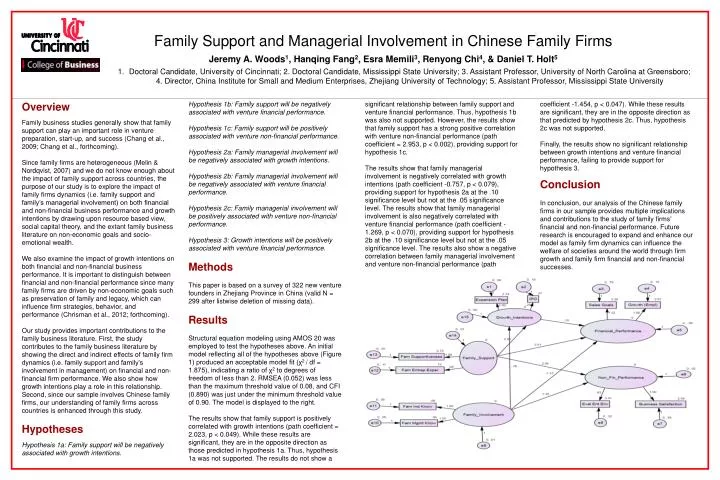

Jeremy A. Woods1, Hanqing Fang2, Esra Memili3, Renyong Chi4, & Daniel T. Holt5 Doctoral Candidate, University of Cincinnati; 2. Doctoral Candidate, Mississippi State University; 3. Assistant Professor, University of North Carolina at Greensboro; 4. Director, China Institute for Small and Medium Enterprises, Zhejiang University of Technology; 5. Assistant Professor, Mississippi State University Overview Family business studies generally show that family support can play an important role in venture preparation, start-up, and success (Chang et al., 2009; Chang et al., forthcoming). Since family firms are heterogeneous (Melin & Nordqvist, 2007) and we do not know enough about the impact of family support across countries, the purpose of our study is to explore the impact of family firms dynamics (i.e. family support and family’s managerial involvement) on both financial and non-financial business performance and growth intentions by drawing upon resource based view, social capital theory, and the extant family business literature on non-economic goals and socio-emotional wealth. We also examine the impact of growth intentions on both financial and non-financial business performance. It is important to distinguish between financial and non-financial performance since many family firms are driven by non-economic goals such as preservation of family and legacy, which can influence firm strategies, behavior, and performance (Chrisman et al., 2012; forthcoming). Our study provides important contributions to the family business literature. First, the study contributes to the family business literature by showing the direct and indirect effects of family firm dynamics (i.e. family support and family’s involvement in management) on financial and non-financial firm performance. We also show how growth intentions play a role in this relationship. Second, since our sample involves Chinese family firms, our understanding of family firms across countries is enhanced through this study. Hypotheses Hypothesis 1a: Family support will be negatively associated with growth intentions. significant relationship between family support and venture financial performance. Thus, hypothesis 1b was also not supported. However, the results show that family support has a strong positive correlation with venture non-financial performance (path coefficient = 2.953, p < 0.002), providing support for hypothesis 1c. The results show that family managerial involvement is negatively correlated with growth intentions (path coefficient -0.757, p < 0.079), providing support for hypothesis 2a at the .10 significance level but not at the .05 significance level. The results show that family managerial involvement is also negatively correlated with venture financial performance (path coefficient -1.269, p < 0.070), providing support for hypothesis 2b at the .10 significance level but not at the .05 significance level. The results also show a negative correlation between family managerial involvement and venture non-financial performance (path coefficient -1.454, p < 0.047). While these results are significant, they are in the opposite direction as that predicted by hypothesis 2c. Thus, hypothesis 2c was not supported. Finally, the results show no significant relationship between growth intentions and venture financial performance, failing to provide support for hypothesis 3. Conclusion In conclusion, our analysis of the Chinese family firms in our sample provides multiple implications and contributions to the study of family firms’ financial and non-financial performance. Future research is encouraged to expand and enhance our model as family firm dynamics can influence the welfare of societies around the world through firm growth and family firm financial and non-financial successes. Hypothesis 1b: Family support will be negatively associated with venture financial performance. Hypothesis 1c: Family support will be positively associated with venture non-financial performance. Hypothesis 2a: Family managerial involvement will be negatively associated with growth intentions. Hypothesis 2b: Family managerial involvement will be negatively associated with venture financial performance. Hypothesis 2c: Family managerial involvement will be positively associated with venture non-financial performance. Hypothesis 3: Growth intentions will be positively associated with venture financial performance. Methods This paper is based on a survey of 322 new venture founders in Zhejiang Province in China (valid N = 299 after listwise deletion of missing data). Results Structural equation modeling using AMOS 20 was employed to test the hypotheses above. An initial model reflecting all of the hypotheses above (Figure 1) produced an acceptable model fit (χ2 / df = 1.875), indicating a ratio of χ2 to degrees of freedom of less than 2. RMSEA (0.052) was less than the maximum threshold value of 0.08, and CFI (0.890) was just under the minimum threshold value of 0.90. The model is displayed to the right. The results show that family support is positively correlated with growth intentions (path coefficient = 2.023, p < 0.049). While these results are significant, they are in the opposite direction as those predicted in hypothesis 1a. Thus, hypothesis 1a was not supported. The results do not show a Family Support and Managerial Involvement in Chinese Family Firms