Download

1 / 19

650 likes | 2.73k Views

Variance Analysis. Types of variances Variance Analysis and Performance Report Accounting for variances. Types of Variances. Direct Material Variance Material price Material usage/quantity variance Direct Labour Variance Rate variance Efficiency variance Overhead variance

E N D

Variance Analysis Types of variances Variance Analysis and Performance Report Accounting for variances

Types of Variances • Direct Material Variance • Material price • Material usage/quantity variance • Direct Labour Variance • Rate variance • Efficiency variance • Overhead variance • Variable overhead variance • Fixed overhead variance • Sales variance • Sales contribution variance • Sales margin price variance • Sales margin volume variance • Yield and Mixed variance

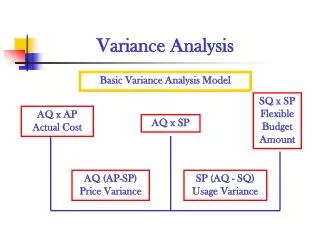

Direct Material Variance • Material Price Variance • Formula: (SP –AP) X AQ • Possible causes • Should AQ be quantity purchased or quantity used? • Computing price variance at the time of purchase because it provide more timely information that proper managerail action can be taken

Direct Material Variance • Material Usage Variance • Formula: (SQ – AQ) x SP • Possible causes • Speedy reporting required • Total Material variance

Direct Labour Variance • Labour Rate variance • Formula: (SR –AR) x AH • Possible causes • Labour efficiency variance • Formula: (SH –AH) x SR • Possible causes

Variable Overhead Variance • Variable overhead Efficiency variance • Formula: (AH- SH)x SVOR • Possible causes: generally the same as those for direct labour efficiency variance

Variable Overhead Variance • Variable overhead Expenditure variance • Formula: (AVOR – SVOR) x AH • Variable overehad is not a homogeneous input and thus the std overhead rate represents a with the average for all the overhead

Fixed Overhead Variance • Total fixed overhead variance is the difference between actual fixed overhead and the applied fixed overhead • Fixed overhead expenditure/spending variance • Formula: (AFOH - BFOH) • Applied fixed overhead = std fixed overhead rate x standard hours

Fixed Overhead Variance • Fixed overhead volume variance • Formula : • BFOH – AFOH • {std fixed o/head rate xSHD} – {std fixed overhead rate x SH) • SHD = std hrs allow. For the denominator output volume used to compute predet. Std fixed o/head rate • SH = std hours allowed for the actual output volume • Possible causes

Fixed Overhead Variance • Fixed overhead volume variance occurs whenever actual output differs from the denominator output volume • Volume variance measures the effect of actual output differing fem the output used to determine the std fixed overhead rate • Volume variance occurs because the actual output differs from the predicted output volume. May represent: • A prediction error • A measure of capacity utilization

Accounting for Variances • In a standard costing system all inventories are carried at standard costs • In recording variances, • all unfavourable variances are always debits • Favourable variances are always credits

Accounting for Material variances • Journal entry associated with the purchase of DM (assuming adverse MPV) DR Materials SP x AO DR Materials Price Variance (SP-SP)AQ CR Accounts Payable AP x AQ • Journal entry associated with the use of DM (assume unfavourable MUV) DR WIP SQ x SP DR MUV (AQ-SQ) x SP CR Materials AQ x SP

Accounting for Direct Labour Variance • Assumes favourable DLR variance • Assumes unfavourable DLE variance DR WIP SH x SR DR DLE Var. (AH –SH) x SR CR. DLR Var (AR-SR)x AH CR. Payroll AH x AR

Mix and Yield Variance • If it is possible to substitute one direct material input for another or one type direct labour for another, variances can occur • A mix variance results whenever the actual mix of inputs differ from the standard mix • A yield variance results whenever the actual yield (output) differs the standard yield