Download

1 / 30

350 likes | 743 Views

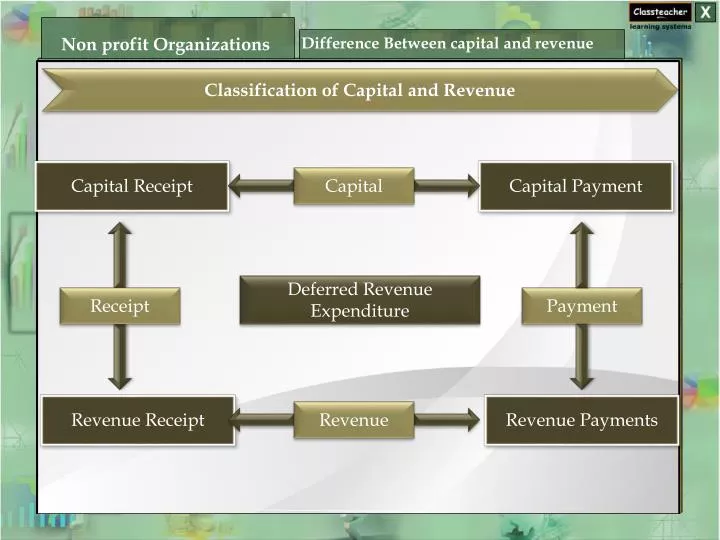

Non profit Organizations. Difference Between capital and revenue. Classification of Capital and Revenue. Capital Receipt. Capital Payment. Capital. Deferred Revenue Expenditure. Receipt. Payment. Revenue Receipt. Revenue Payments. Revenue. Non profit Organizations.

E N D

Non profit Organizations Difference Between capital and revenue Classification of Capital and Revenue Capital Receipt Capital Payment Capital Deferred Revenue Expenditure Receipt Payment Revenue Receipt Revenue Payments Revenue

Non profit Organizations Difference Between capital and revenue Capital receipt are those receipt which are not revenue in nature. Capital Receipt Sale of Land and Building other than a dealer Raising of loans Accounting Treatment These are credited to the respective account of Capital nature.

Non profit Organizations Difference Between capital and revenue Revenue receipt are those receipt which arise in the normal course of business. Revenue Receipt Sale of Land and Building by a dealer Raising of loans by a person engaged in the same business Accounting Treatment These are credited to the Trading and Profit & Loss Account.

Non profit Organizations Difference Between capital and revenue Expenditure incurred to increase the productivity and earning capacity. Capital Payment Cost of Land and Building Cost of Plant and Machinery Accounting Treatment It is debited to the respective asset account.

Non profit Organizations Difference Between capital and revenue Expenditure incurred to maintain the productivity and earning capacity. Revenue Payment Repair to Building Wages Accounting Treatment It is debited to the Trading and Profit & Loss Account.

Non profit Organizations Difference Between capital and revenue Expenditure for which expenditure has been made or the liability has been incurred which will benefit over a subsequent period. Deferred Revenue Expenditure Expenditure on Advertisement Accounting Treatment Normally such expenditure will be written off over a period of 3 to 5 years.

Accounting Treatment for Special Items Closing Stock In Balance sheet Balance Sheet for the year ended 31st December 2012

Accounting Treatment for Special Items Outstanding Expense When expenses of an accounting period remain unpaid at the end of an accounting period, they are termed as outstanding expenses. Accounting Treatment: Shown on the Liability side of the balance sheet Added to the Concerned Expense

Accounting Treatment for Special Items Outstanding Expense In Trading P&L A/c Trading a/c for the year ended 31st December 2012 + Outstanding Amount Concerned Expense

Accounting Treatment for Special Items Outstanding Expense In Balance sheet Balance Sheet for the year ended 31st December 2012

Accounting Treatment for Special Items Prepaid Expense These are expenses which are paid in advance in the normal course of business operations and may be carried forwarded to the next year. Accounting Treatment: Shown on the Asset side of the balance sheet Deducted from the Concerned Expense

Accounting Treatment for Special Items Outstanding Expense Trading a/c for the year ended 31st December 2012 Prepaid Amount Concerned Expense

Accounting Treatment for Special Items Outstanding Expense Balance Sheet for the year ended 31st December 2012

Accounting Treatment for Special Items Accrued Income Some times certain items of income such as interest on loan, commission, rent, etc. are earned during the current accounting year but have not been actually received by the end of the same year. Such incomes are known as accrued income. Accounting Treatment: Shown on the Liability side of the balance sheet Added to the Concerned Income

Accounting Treatment for Special Items Accrued Income Trading a/c for the year ended 31st December 2012

Accounting Treatment for Special Items Accrued Income Balance Sheet for the year ended 31st December 2012

Accounting Treatment for Special Items Income Received in Advance Sometimes, a certain income is received but the whole amount of it does not belong to the current period. The portion of the income which belongs to the next accounting period is termed as income received in advance or an UnearnedIncome. Accounting Treatment: The total amount will be deducted from the concerned income in the credit side of the P&L a/c. Shown on the Liability side of the balance sheet

Accounting Treatment for Special Items Income Received in Advance Balance Sheet for the year ended 31st December 2012

Accounting Treatment for Special Items Depreciation Depreciation is the decline in the value of assets on account of wear and tear and passage of time. It is treated as a business expense and is debited to profit and loss account. Accounting Treatment: It is treated as a business expense and is debited to profit and loss account. Deducted from the concerned Asset.

Accounting Treatment for Special Items Income Received in Advance Trading a/c for the year ended 31st December 2012

Accounting Treatment for Special Items Depreciation Balance Sheet for the year ended 31st December 2012

Accounting Treatment for Special Items Bad Debts Bad debts refer to the amount that the firm has not been able to realize from its debtors. It is regarded as a loss and is termed as bad debt. Accounting Treatment: When the bad debts is given in P&L a/c and Trial Balance (Further Bad Debts) Amount of further bad debts is added to the existing bad debts in the debit side of the P&L a/c. Deducted from the existing debtors amount

Accounting Treatment for Special Items Bad Debts Trading a/c for the year ended 31st December 2012

Accounting Treatment for Special Items Bad Debts Balance Sheet for the year ended 31st December 2012

Accounting Treatment for Special Items Provision for Bad Debts Provision for bad and doubtful debt is the estimated loss provided upon the debtors for the future. Accounting Treatment: Debited to the P & L a/c Deducted from the existing debtors amount after further bad debts

Accounting Treatment for Special Items Provision for Bad Debts Trading a/c for the year ended 31st December 2012

Accounting Treatment for Special Items Provision for Bad Debts Balance Sheet for the year ended 31st December 2012

Accounting Treatment for Special Items Managers Commission This is the amount of commission allowed to the managers on the net profit of the company. Managers Commission Net Profit after commission Net Profit before Commission Suppose the net profit of a business is Rs. 110 before charging commission. If the manager is entitled to 10% of the profit before charging such commission, the commission will be calculated as : In case the commission is 10% of the profit after charging such commission, it will be calculated as : = Profit before commission × Rate of commission/ (100 + commission) = Rs. 110 × 10/100 = Rs. 11 = Rs. 110 × 10 = Rs. 10 110

Accounting Treatment for Special Items Provision for Bad Debts Trading a/c for the year ended 31st December 2012

Accounting Treatment for Special Items Provision for Bad Debts