Download

1 / 42

420 likes | 556 Views

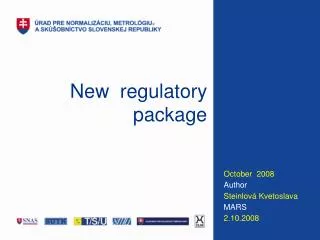

NEW REGULATORY FRAMEWORK. Karsten Meinhold Siemens AG, Munich. Operators. Traffic Volume. The battle is going on. Explosion. Telecom Tariffs. Consolidation. Source: Gartner Group. Restructuring. 97. 98. 99. 00. 01. 02. 03. Time. 04. COMPETITION GOES ON.

E N D

NEW REGULATORY FRAMEWORK Karsten Meinhold Siemens AG, Munich

Operators Traffic Volume The battle is going on Explosion Telecom Tariffs Consolidation Source: Gartner Group Restructuring 97 98 99 00 01 02 03 Time 04 COMPETITION GOES ON

IMPACT OF COMPETITION ON ECONOMY • Model: • Competition shall • drive prices down • give incentives for innovative services and infrastructure • allow users, consumers better choice • Consequence: • Electronic communication is more readily used, • market volume goes up. This increased use of electronic communications is basis for a more competitive and dynamic economy in general.

PRICES EU weighted average tariff reduction for national calls(variation 1997 – 2000) • Residential users - 9.5 % • Business users - 20.0 % • EU weighted average reduction for international calls(variation 1997 – 2000) • Residential users - 32 % • Business users - 34 % Source: European Commission 6th implementation report 12/2000

Annual growth in % + 17 + 26 + 10 1997/1998 1998/1999 1999/2000 Traffic growth in fixed networks; Germany Source: Annual Report RegTP

More choice Fast-growing market Some prices down Incumbents still dominate +20% 191 bn Euro 557 +155% 160 bn Euro Prices 1997 / 1999 96% 91% 218 + 7% - 40% local 1999 2000 Telecoms servicesmarket 1998 1999 Network operators Incumbents’market share 1997 / 1999 International Telecom liberalisation: Work in progress, results

Sixth Report on the Implementation of the Telecommunications Regulatory Package - Summary • growth continues at an average rate of 9% over 1999 • marketsize €191 billion in 2000. • for mobile services market : • penetration increased 36% to 55% • 194 million subscribers • 54 operators licensed • for the fixed line service market: • 461 operators are offering public voice telephony for long-distance calls, up 89% on 1999 • 468 for international calls, up around 67% • 388 for local calls, up 74%. • 861 operators have been allocated access codes for carrier selection. • Tariffs continue to move downwards • national calls decreased 10.5% on 1999 for business, 4.6% for residential • international calls decreased 15.1% for business, 13.5% for residential

MATTERS TO BE ADDRESSED • licensing procedures are still in some cases cumbersome • timing of the licensing of 3G in a number of countries too slow • tariff rebalancing has still to be completed • supervision of cost accounting systems • full range of carrier pre-selection services • negotiation of the physical requirements for the installation of new entrants’ equipment at local exchanges for the provision of local access services may require decisive regulatory intervention • difficulties in obtaining rapid and equitable interconnection • call termination tariffs in mobile networks are in some cases still not competitive • timely delivery of leased lines • the incumbent continues to enjoy first mover advantage in the roll-out of ADSL • continued concern at the lack of monitoring at national level of consumer issues

Seventh Report on the Implementation of the Telecommunications Regulatory Package - Summary • growth continues at an average rate of 9.5% for 2001 • marketsize €218 billion in 2001. • for mobile services market : • penetration increased to 73% • Revenue growth 22.3% • 36% more subscribers • Tariffs continue to move downwards • Long distance calls decreased 45% since 1998 for 3 min. Call • Long distance calls decreased 47% since 1998 for 10 min. Call • Advanced Services: • Internet penetration in EU households was 36% in June 2001 • Some Regulatory bottlenecks still to be addressed: • Local Loop Unbundling • Development of Broadband Services

x 7 x 10 x 5 bottlenecks of the 7th Implementation report

EXISTING REGULATORY PACKAGE • Services Directive (90/388/EEC) • extended to: Satellite (94/46/EC) • Cable (95/51/EC) • Mobile (96/2/EC) • Full competition (96/19/EC) • Cable ownership (1999/64/EC) • ONP Framework Directive (90/387/EEC amended by 97/51/EC) • Licensing Directive (97/13/EC) • GSM Directive (87/372/EEC) • ERMES Directive (90/544/EC) • DECT Directive (91/287/EEC) • S-PCS Decision (97/710/EC) • UMTS Decision (99/128/EC) • European Emergency NumberDecision (91/396/EC) • International Access Code Decision(92/264/EEC) • ONP leased lines Directive(92/44/EEC amended by 97/51/EC) • TV standards Directive (95/47/EC) • Interconnection Directive(97/33/ EC amended by 98/61/EC) • Voice telephony Directive (98/10/EC) • Telecoms data protection Directive(97/66/EC)

THE NEED TO OVERHAUL THE 1998 TELECOMS FRAMEWORK • Respect review obligations from current directives • Amplify the benefits of competition for users (choice, prices, quality) • Adapt the framework to technology changes (convergence, Internet, etc.) and to market changes (e-commerce, changes in competition, etc.) • Meet the demands of the Lisbon Summit, to have the package adopted by the end of 2001

GOAL OF THE REVIEW PROCESS • to continue the liberalisation process which was started in 1998 • to adapt the regulation to the technological evolution • to cope with the aspects of convergence • to harmonise the EU landscape, and • to simplify the regulatory framework (from 20 to 8)

Amount of regulation Pro-competitive sectorial telecoms Laws Regulation & governance of EC Competition Law 1990 1998 2001 Monopoly Towards full competition EC: electronic communication RELY INCREASINGLY ON COMPETITION RULES

Voice telephony FixedMobile Data Fixed Mobile Broadcasting Cable Satellite Terrestrial Service Internet Type of network WirelessSatelliteCaTVTelecom Wire-line Cu or Optical Electronic Communication Terminal CONVERGENCE REMOVES SECTOR BOUNDARIES

Framework Directive (Art. 95) Authorisation Directive Liberalisation Directive (Art. 86) Access & Interconnection Directive Unbundled local loop Regulation Users’ Rights Directive Spectrum Decision (Art. 95) Data Protection Directive EU‘s NEW REGULATORY FRAMEWORK

THE NEW FRAMEWORK CONTAINS • 1 Regulation: in force from 31/12/2000 • unbundled access of the local loop • 5 Directives: to be in force by 25/07/2003 (one exception tobe in force by 31.10.2003) • a common regulatory framework for electronic communications networks and services • the processing of personal data and the protection of privacy in the electronic communications sector • the authorisation of electronic communications networks and services • universal service and users’ rights relating to electronic communications networks and services • access to, and interconnection of, electronic communications networks and associated facilities

EQUALLY IMPORTANT DOCUMENTS • A draft Commission Liberalisation Directive • A Decision on Community RadioSpectrumPolicy The documents can be found on the EU web at: http://www.ispo.cec.be/infosoc/telecompolicy/review99/Welcome.html

SIMPLIFICATION, CLARIFICATION Services Directive (90/388/EEC) extended to: Satellite (94/46/EC) Cable (95/51/EC) Mobile (96/2/EC) Full competition (96/19/EC) Cable ownership (1999/64/EC) ONP Framework Directive (90/387/EEC amended by 97/51/EC) Licensing Directive (97/13/EC) GSM Directive (87/372/EEC) ERMES Directive (90/544/EC) DECT Directive (91/287/EEC) S-PCS Decision (97/710/EC) UMTS Decision (99/128/EC) European Emergency Number Decision (91/396/EC) International Access Code Decision (92/264/EEC) ONP leased lines Directive (92/44/EEC amended by 97/51/EC) TV standards Directive (95/47/EC) Interconnection Directive(97/33/ EC amended by 98/61/EC) Voice telephony Directive (98/10/EC) Telecoms data protection Directive (97/66/EC) Liberalisation Directive Framework Directive Authorisation Directive Access & Interconnection Directive Unbundled local loop Regulation/Ordinance Users’ Rights Directive Data protection Directive Quelle: http://www.europa.eu.int/comm/information_society/policy/framework/index_en.htm

FRAMEWORK DIRECTIVE I • Scope: electronic communications services, electronic communications networks, associated facilities (incl. fixed, mobile satellite and broadcast networks/services) • Aim: tasks of NRAs, harmonised application of the regulatory framework • NRAs legally distinct and functionally independent from all organisations providing communications services, networks,... • Policy Objectives and Regulatory principles: • maximum benefit for users (choice, price, quality) • no distortion or restriction of competition • efficient investment in infrastructure, promoting innovation • efficient usage of radio frequencies and numbering resources

FRAMEWORK DIRECTIVE II • Significant Market Power (SMP): definition criteria: power to behave to some extend independently of competitors, customers and ultimately consumers.Criteria for such assessment in Annex II. • Where an undertaking has SMP it may be also deemed to have SMP on a closely related market • Market definition according to Annex I (minimum coverage of services of other directives) • Standardisation: • The Commission shall draw up and publish in the Official Journal of EC a list of standards/specifications (CEN, CENELEC, ETSI, ITU..) • Member States (MS) shall encourage the usage of these standards

Main obligations: applicable to ‘electronic communications networks’ increased power of NRA’s installation of Appeal Body definition of ‘significant market power’ installation of ‘Communications Committee’ Important consequences: impact on activities in transmission, switching, routing and other resources conveying signals by wire, radio or optics in satellite, fixed (CS, PS, IP), mobile, radio and TV broadcasting, CATV and PL networks Brings Europe in the lead on Liberalisation of Telecom COMMON REGULATORY FRAMEWORK

UNIVERSAL SERVICE DIRECTIVE I • Aim & Scope: Publicly available serviceswith good quality, to which all users have access at an affordable price: • establishment of rights of end-users, including oncorporate networks: • includes retail provision of leased lines • Definitions: • public telephone network, • network termination point (NTP), • geographic and non-geographic numbers

UNIVERSAL SERVICE DIRECTIVE II • Member States shall ensure that the following services of the directive are made available to all end-users at affordable price: • Connection at fixed location • telephone, fax, data communications with rates sufficient for internet access • telephone directory • European call number 112, 00, 3883 • measures for disabled users • Quality of service parameters according to Annex III (ETSI Quality Standards) • Transparency and publication of information on prices, standard terms,.. (Annex II)

UNIVERSAL SERVICE DIRECTIVE III • Specific facilities and services according to Annex I: • Itemised billing • Selective call barring for outgoing calls, free of charge • Pre-payment systems • Phased payment of connection fees • Appropriate measures against non-payment of bills • Tone dialling or DTMF (dual-tone multi-frequency operation) • Calling-line identification • Consumer equipment for digital TV reception shall allow the de-scrambling according to ETSI standards, > 30 cm screen: DVB common interface connector • Interoperability between analogue and digital TV sets • Minimum set of non-discriminatory leased lines, cost based

Main obligations: covers speech, fax and data services (including internet) at a fixed location, wireless or by wire-line connection to all users in the territory for reasonable price by at least one operator special measures for disabled users Obligations for NRA’s control prices/ transparency Important consequences: number portability, CS and CPS applicable to fixed and mobile networks US obligations can also be fulfilled by New Operators numbering issues: 112, 00, 3883 in all member states UNIVERSAL SERVICE AND USER‘S RIGHTS

ACCESS DIRECTIVE I • Aim: harmonisation of access to and interconnection of electronic communications networks and associated facilities for sustainable competition and interoperability • Scope: rights and obligations for operators and undertakings seeking access to and interconnection of their networks (incl. local loop and broadcast especially access to wide screen 16:9 television services) and associated facilities. • Operators of public communications networks have the right and obligation to negotiate interconnection. Operators shall offer access and interconnection to other undertakings on terms and conditions consistent with obligations imposed by NRAs • Networks for digital TV shall be capable of 16:9 wide-screen

ACCESS DIRECTIVE II • Duty to maintain wide screen format • Conditional Access (CA): Conditions of Annex I: Operators of CA services who provide access to digital TV are to: • offer to all broadcasters on fair, reasonable and non-discriminatory basis compatible with competition law • keep separate financial accounts regarding their activities as CA provider • Other facilities to which conditions apply: • Access to application program interfaces (API) • Access to electronic program guides (EPG)

ACCESS DIRECTIVE III • Concerning unbundled access: NRA’s shall ensure the publication of reference offer containing at least the elements of Annex II: • local sub-loop, unbundled access to the local loop, • full unbundled access • shared access • conditions for unbundled local loop: • network elements to which access is offered • Collocation services: physical and virtual collocation, equipment restrictions in collocation space, security issues, access conditions for staff of competitive operators, rules for allocation of space, inspection • Supply conditions: Lead time for responding to requests, service level agreements, fault resolutions, standards contract terms, pricing for all aforementioned points

Main obligations for Notified Operators: publish detailed and transparent Reference Offer Obligations for NRA’s control pricing impose accounting separation impose to grant access resolve disputes Important consequences: accelerate the market penetration of New Operators increases the market volume for ADSL technology by Notified and New Operators potential impact on IP network interconnection ACCESS AND INTERCONNECTION

AUTHORISATION DIRECTIVE I • Aim: Harmonisation and simplification of authorisation rules and conditions. • Scope: Authorisations for the provision of electronic communications services and networks • The provision of electronic communications may only be subject to general authorisation: Notification yes, but not explicit decision or administrative act by NRA. • General Authorisation: gives right to install facilities, negotiate interconnection, to contribute to universal service, to use general authorised frequencies, where risk of harmful interference is negligible • Where necessary: individual rights of use for radio frequencies and numbers shall be granted to general authorised undertakings through open, transparent and non-discriminatory procedures (incl. broadcast)

AUTHORISATION DIRECTIVE II • Conditions attached to general authorisation and right of use for radio frequencies and numbers may contain only the conditions of the Annex: • financial contributions to U.S. obligation • administrative charges • interoperability and interconnection • accessibility of numbers from national numbering plan • use of public and private land • collocation and facility sharing • financial and technical guarantees to ensure the proper execution of infrastructure works

AUTHORISATION DIRECTIVE III • „must carry“ obligations • personal data and privacy protection • consumer protection • restriction of illegal content • information duties • legal interception, security measures • special access • frequency usage and usage of standards • Limitation of number of right holders: objective, transparent and non-discriminatory selection criteria

Main obligations: generalauthorisation and notification by undertaker commercial activities can start immediately after notification measures to facilitate the exercise of ‘rights of way’ and ‘rights of interconnection’ Important consequences: Simplifies the process and start-up for New entrence extensively changes the importance and the role of NRA accelerate the market penetration of New Operators increases the market volume AUTHORISATION

Processing of personal data,protection of privacy Scope: Processing of personal data in connection with electronic communication services Aim: Protect fundamental rights and freedoms with respectto processing of personal data; complement to directive 95/46/EC. Not covered: issues outside the Treaty, like defence, state security Covered: Security of services Confidentiality of communications Handling of traffic data Itemised billing Calling and connected line identification Automatic call forwarding Directories Unsolicited communications

Main obligations: restricted use and storage of trafficdata calling- and connected-line identity control by user restricted use and storage of locationdata measures againstunsolicited communications Important consequences: Protecting the privacy of citizens by limiting storage of data Powers to act against spamming Potential impact on functional implementation in networks and products PERSONAL DATA AND PRIVACY PROTECTION

Main obligations for Notified Operators: full unbundled access shared access collocation conditions in place by 31/12/2000 Obligations for NRA’s control pricing - cost based resolve disputes Important consequences: increases the market volume in general Enforced collaboration between incumbent and new operator on basic infrastructure accelerate the market penetration of New Operators Stimulate penetration of Broadband Band connections increases the market volume for ADSL technology by Notified and New Operators UNBUNDLED ACCESS TO THE LOCAL LOOP

Number of customers (million) 45 Total 40 35 30 N. America 25 20 15 Europe 10 Asia 5 0 2000 2001 2002 2003 FORECAST FOR DSL EQUIPMENT (FEB. 2000) Sources: Cahners, IDC, Yankee Group

Situation • The European Parliament and the Council of the European Union approved the Regulation on ULL Dec.2000, immediately applicable in all member states • The European Parliament and the Council of the European Union approved 4 out of 5 of the Directives which are to be implemented into National law by the member states by 24/7/2003 • The ‘Personal Data & Privacy Protection’ was approvedin mid July 2002. The implementation period lasts until 31/10/2003.

Situation (cont.) Commission recommendation on definition of relevant Product and service markets: in consultation Commission gudeline on assessment of SMP: adopted Committees for harmonised application Communications committee European regulators Group Radio spectrum committee Radio spectrum policy group