Download

1 / 11

150 likes | 1.58k Views

Accounting vs. Economic Profit. Accounting Profit = Revenue - Explicit CostsEconomic Profit = Revenue - Opportunity (Explicit Implicit) CostsEcon Profit accounts for owner's next best alternativee.g.., implicit costs=$15K, explicit costs=$100K, revenues=$300K:Accounting Profit = ??Econ

E N D

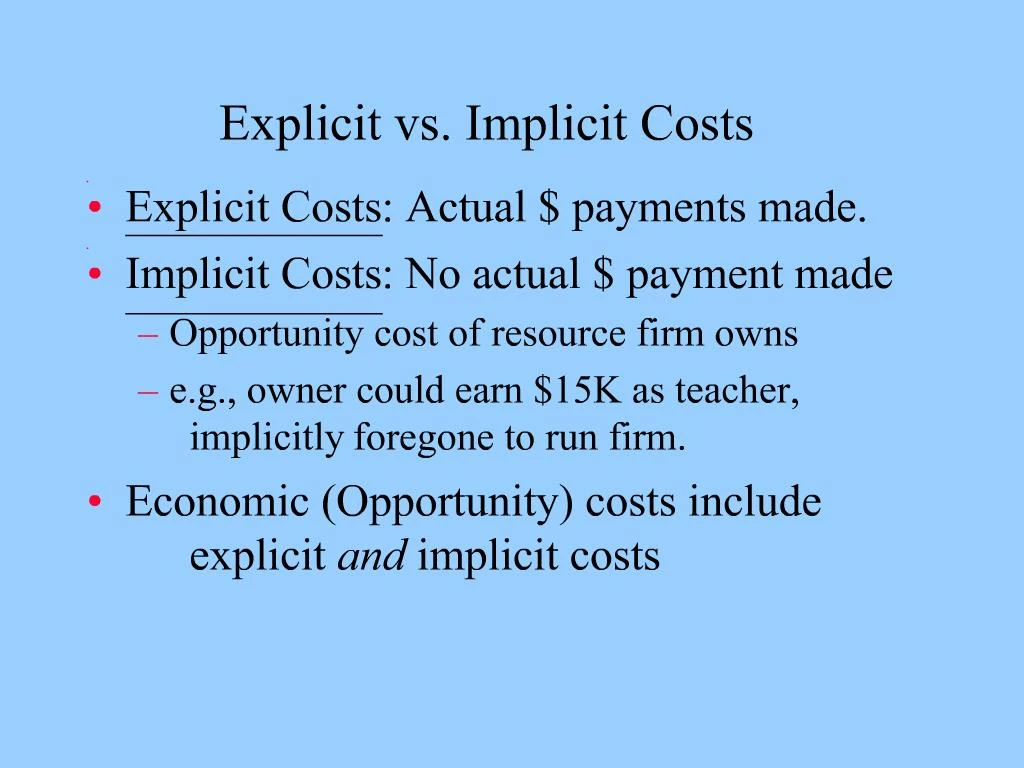

1. Explicit vs. Implicit Costs Explicit Costs: Actual $ payments made.

Implicit Costs: No actual $ payment made

Opportunity cost of resource firm owns

e.g., owner could earn $15K as teacher, implicitly foregone to run firm.

Economic (Opportunity) costs include explicit and implicit costs

2. Accounting vs. Economic Profit Accounting Profit = Revenue - Explicit Costs

Economic Profit = Revenue - Opportunity (Explicit + Implicit) Costs

Econ Profit accounts for owner�s next best alternative

e.g.., implicit costs=$15K, explicit costs=$100K, revenues=$300K:

Accounting Profit = ??

Economic Profit = ??

3. Zero (normal) economic profit:

Just enough to keep owner in business and resources employed there

Just equal to its next best alternative.

e.g.., owner earned $115K revenues, econ profit = 0

Sunk costs:

Irrelevant to decision-making

Incurred by past decisions, can�t be undone

Examples?

4. Production and Costs Producing goods requires resources, time, and incurring costs

We�ll focus on 3 costs: Total Cost (TC), Average Total Cost (ATC), Marginal Cost (MC)

TC = Cost of using inputs to produce given output

ATC = (Total Cost) / (Output)

MC = D in TC from producing one more unit of output = (D TC) / (D Output)

5. Numerical examples:

Total Cost of 1st unit = 150

Total Cost of 2nd unit = 180

Then for 2nd unit produced:

ATC = 180 / 2 = 90

(NOTE: Total Cost = ATC x Output = 2 x 90 = 180)

Marginal Cost = TC of 2nd unit (180) - TC of 1st unit (150) = 30

6. Marginal Physical Product (MPP), Diminishing Marginal Returns, and MC MPP = Extra output from hiring another unit of input (e.g., labor hour):

MPP = (D Output) / (D Input)

Law of Diminishing Marginal Returns

As more input added (to fixed inputs), it�s additional productivity declines

Adding another unit increases output by less than previous one.

MPP at some point declines

7. Diminishing Marginal Returns Underlies Concept of Marginal Cost (MC) MC = D in cost associated with D in Output = (D TC) / (D Q)

Changing output means hiring extra inputs

If MPP increases, MC of producing declines

But as diminishing marginal returns sets in, MPP declines

8. Diminish. marginal returns means MC rises

As input�s productivity (MPP) declines, why must (MC) increase?

What happens to firm�s MC if diminishing marginal returns never set in?

9. MPP & MC move in Opposite Directions (using examples in text)

10. Shape of ATC Curve: Average-Marginal Rule Marginal > average means average rises

Marginal < average means average falls

�Marginal� pulls �Average� in same direction

Example: Average of 3 quizzes = 80, & 4th quiz = 90

Does Marginal Quiz (4th) pull average up/down?

11. Relation Between Average Total Cost and Marginal Cost ATC decreasing when MC < ATC

ATC increasing when MC > ATC

At minimum ATC, MC = ATC

Minimized per unit cost

12. Shifts in Cost Curves Taxes per unit produced

Input Prices

Improved Technology