Download

1 / 15

200 likes | 466 Views

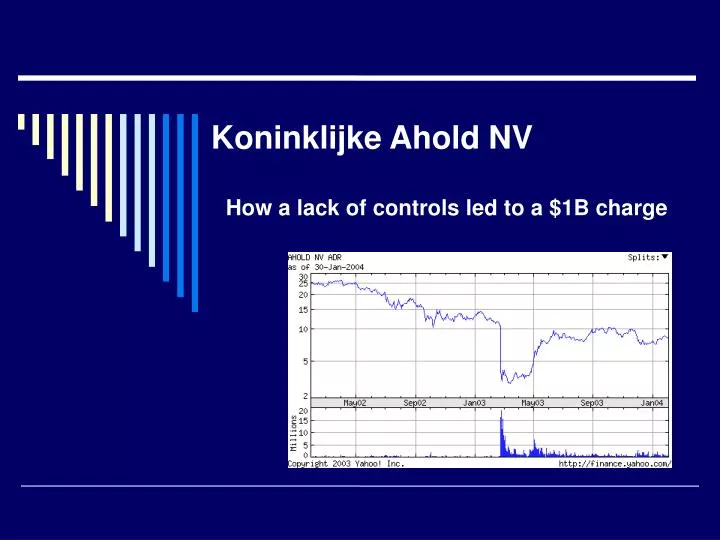

Koninklijke Ahold NV. How a lack of controls led to a $1B charge. Koninklijke Ahold NV. Overview. Royal Ahold acquires US Foodservice for $3.6B in April 2000 Fraud revealed in February 2003 Players: Mark Kaiser and Timothy Lee

E N D

Koninklijke Ahold NV How a lack of controls led to a $1B charge

Overview • Royal Ahold acquires US Foodservice for $3.6B in April 2000 • Fraud revealed in February 2003 • Players: Mark Kaiser and Timothy Lee • Scheme: Exploit lack of controls to over-accrue for vendor rebates • Results: Overstatement of acquisition balances $90M, 2000 earnings $110M, 2001 earnings $260M, 2002 earnings $510M

Aftermath • Fired – Mark Kaiser, Chief Marketing Officer • Fired – Timothy Lee, Exec. VP Purchasing • Resigned – James Miller, CEO • Resigned – Cees van der Hoeven, Ahold CEO • Resigned – Michael Meurs, Ahold CFO • Stock drops 61% on 2/24, 17% on 2/25 • Earnings overstated $880M, Pre-Tax Charge $1B ''It is a very disappointing result,'' said Dudley Eustace, Royal Ahold's interim chief financial officer

How Was It Detected? • ConAgra • Late January/Early Feburary, accounting dept found unqualified sales representatives verifying inaccurate US Foodservice rebates • Alerted US Foodservice and Deloitte & Touche • Ahold Internal Investigation • Discovered irregularities in February • Deloitte & Touche • Discovered irregularities during its 2002 audit • Gave Ahold a clean bill of health in 2001 (~$250M in fraud)

Cause 1: Company Culture • Acquisition Race • CEO, Hoeven, spent $19 billion over 10 yrs to buy companies in 30 countries • Opening balances at the US Foodservice was reduced by $90 million due to the fraud • Due diligence conducted by Merril Lynch and Ahold • Pressure to Increase Profit • “go-go” atmosphere gone too far

Cause 2: Personal Gain • Inflate earnings to increase bonuses • Sales representatives at suppliers may have been paid off

Cause 3: Shady Industry Practice • Lack of Transparency • Improper acceleration of revenue recognition • Rebates for volume/time/shelf-space sales • False inflation of retailer's profits • Explains the magnitude and the duration of the fraud

Cause 4: Weak Control Mechanism • At acquisition, US Foodservice warned Ahold that internal control systems on promotional allowances were “not good at all” • Efforts were made to improve control systems but no significant improvements

Due Diligence & The Issue of Fraud • The Financial Times, dated 5/9/03, reported that Dudley Eustace, Ahold then interim CFO, commented that “the fraud should have been detected during the process of due diligence.” • Eustace further comments that “The company [Ahold] has been flying blind with inadequate control systems. Once you added collusion to create fraud, you had a recipe for disaster.” • “When you are doing due diligence, you are not looking for fraud.”

If Conducting Due Diligence, Then Questions To Be Asked Consist Of… • What is the company’s current policy for tracking and accruing for rebates receivable? • Are rebates receivable currently tracked or estimated? • How does your company currently ensure that rebates receivable are monitored by the internal audit function for adequacy? • What are the current procedures for approving rebate programs?

Financial Statement Analysis • Examine & compare the ratio of rebate income to gross sales to previous year and budget • Examine & compare the ratio of gross sales to rebates receivable to previous year and budget

In General, Questions To Consider • Company receive rebates from vendors? If so, in what capacity? • Vendor rebates based on complex & opaque formulas linked to specified volume targets? • Company accrue for rebates receivable? • An unexplained increase in rebate income? • Rebate income increased as a percentage of gross sales? • Rebates receivable increased as a percentage of gross sales?