Download

1 / 30

300 likes | 426 Views

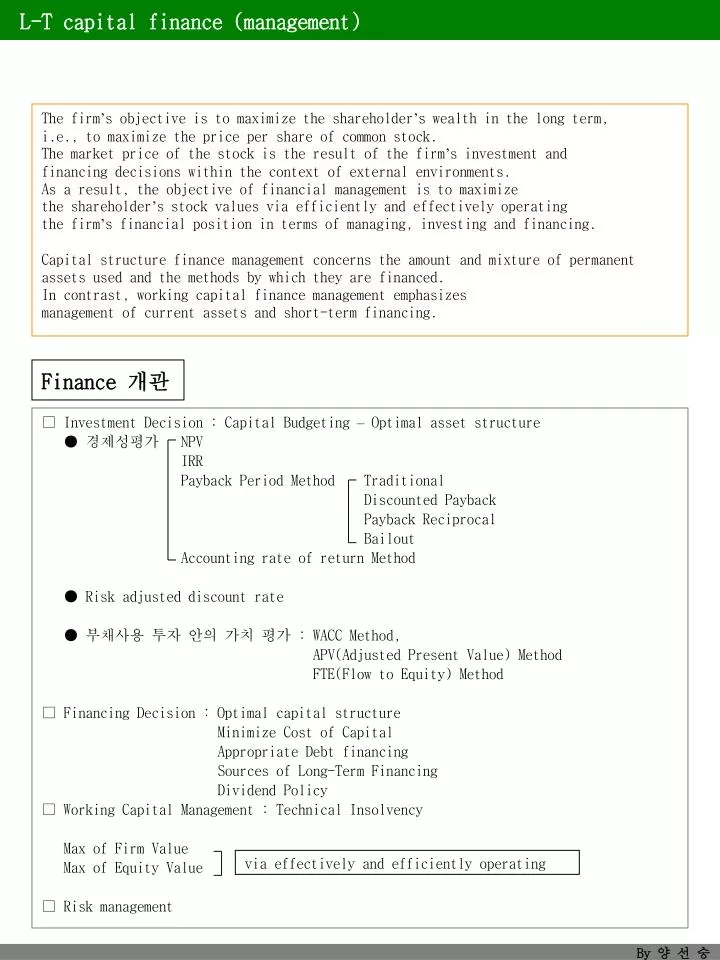

The firm ’ s objective is to maximize the shareholder ’ s wealth in the long term, i.e., to maximize the price per share of common stock. The market price of the stock is the result of the firm ’ s investment and financing decisions within the context of external environments.

E N D

The firm’s objective is to maximize the shareholder’s wealth in the long term, i.e., to maximize the price per share of common stock. The market price of the stock is the result of the firm’s investment and financing decisions within the context of external environments. As a result, the objective of financial management is to maximize the shareholder’s stock values via efficiently and effectively operating the firm’s financial position in terms of managing, investing and financing. Capital structure finance management concerns the amount and mixture of permanent assets used and the methods by which they are financed. In contrast, working capital finance management emphasizes management of current assets and short-term financing. Finance 개관 □ Investment Decision : Capital Budgeting – Optimal asset structure ● 경제성평가 NPV IRR Payback Period Method Traditional Discounted Payback Payback Reciprocal Bailout Accounting rate of return Method ● Risk adjusted discount rate ● 부채사용 투자 안의 가치 평가 : WACC Method, APV(Adjusted Present Value) Method FTE(Flow to Equity) Method □ Financing Decision : Optimal capital structure Minimize Cost of Capital Appropriate Debt financing Sources of Long-Term Financing Dividend Policy □ Working Capital Management : Technical Insolvency Max of Firm Value Max of Equity Value □ Risk management via effectively and efficiently operating

* CA WORKING CAPITAL MANAGEMENT The optimal investment in current assets is that which minimizes the sum of carrying and shortage costs. Carrying costs and Shortage costs The costs associated with managing current assets are : carrying costs, which increase with the level of investment in current assets; and shortage costs, which decrease with increases in the level of investment in current assets. Carrying costs are generally of two types. 1) Opportunity cost : Because the rate of return on current assets is low compared with that of other assets there is an opportunity cost. 2) The cost of maintaining the economic value of item : The cost of warehousing inventory belongs here etc. Shortage costs are trading (or order) costs and costs related to safety reserves. 1) Trading costs arise when the firm runs out of cash or inventory and must consequently incur the cost of restocking. 2) Costs related to safety reserves include loss of sales or customer goodwill, or production time when a stock out (or 'cash out') occurs. $ The total of Holding current assets Carrying cost The minimum cost Shortage cost CA The optimal amount of CA. This point minimizes costs

* * CA CA Flexible(conservative) policy $ Carrying cost Shortage cost CA The optimal amount of CA. This point minimizes costs 보수적인 정책은 보유비용이 부족비용에 비해 상대적으로 낮을 때 가장 적합하다. Restrictive(aggressive) policy $ Carrying cost Shortage cost CA The optimal amount of CA. This point minimizes costs 공격적인 정책은 보유비용이 부족비용에 비해 상대적으로 높을 때 가장 적합하다.

Alternative Financing Policies for Current Assets Many financing policies are feasible. An Ideal Model Short-term assets can always be financed with short-term debts and Long-term assets can be financed with long-term debts and equity. In this economy net working capital would be zero. ( Financing Policy for an Idealized Economy) $ CA = S-T debts Fixed assets L-T debts Plus Common stock Time In an ideal world, net working capital is always zero because S-T assets are Financed by S-T debts. A growing firm can be thought of as having both a permanent requirement for CA and for L-T assets. This total asset requirement will exhibit balances over time reflecting 1) A secular growth trend 2) a seasonal variation around the trend 3) Unpredictable day-to-day and month-to-month fluctuations.

Seasonal variation $ Total asset requirement secular growth in fixed Assets and permanent CA Time The Total Asset Requirement over Time - 필요한 총자산에 예측할 수 없는 일별 변동성과 월별 변동성은 보여주려 하지 않음. Total asset requirement Marketable securities $ $ L-T financing Total asset requirement S-T financing L-T financing Time Time ( Strategy Flexible ) ( Strategy Restrictive ) Strategy F always implies a S-T cash surplus and a large investment in cash and Marketable securities. Strategy R uses L-T financing for secular asset requirements only, and S-T borrowing For seasonal variation.

회사는 주기적인 자금수요에 부응하기위해 두 가지 극단적 전략이 있다. 첫째, 회사는 비교적 많은 Marketable securities을 보유할 수 있다. 재고자산과 다른 유동자산에 대한 수요가 증가함에 따라 회사는 Marketable securities 를 팔아 필요한 것들을 구매할 수 있는 현금을 마련한다. 일단 재고자산이 팔리고 보유하고 있는 재고자산이 줄어들기 시작하면 Marketable securities에 재투자한다. 이 방법은 Strategy F 로 설명되는 보수적인 정책이다. 회사는 근본적으로 필요한 유동자산의 변화에 대한 완충장치로 Marketable securities의 Pool을 이용한 점에 주목하자. 다른 극단에는 회사가 유가증권을 보유하지 않을 수 있다. 재고자산과 다른 자산에 대한 수요가 증가할 때 회사는 단순히 현금을 단기적으로 빌린다. 그리고 자산에 대한 수요가 낮아지는 주기가 되면 대출금을 상환한다. 이런 방법은 Strategy R 로 설명된 공격적인 정책이다. 두 가지 정책을 비교할 때, 주요 차이점은 필요한 자산에서 계절적 변동에 대한 자금을 조달하는 방법이다. Which Financing Policy is Best? There is no definitive answer to the question: "How much short-term borrowing is optimal?" Several factors must be considered. First, Cash Reserve Firms with flexible policies are generally less likely to experience financial distress since this policy implies less difficulty in meeting short-term obligations. However, investments in cash and marketable securities are zero NPV investments at best. Second, Maturity Hedging Most firms hedge interest-rate risk by matching debt maturities with asset maturities; a policy of financing long-term assets with short-term debt, for example, is inherently risky since frequent refinancing is needed, and short-term interest rates are more volatile than long-term rates. This type of maturity mismatching would necessitate frequent financing and is inherently risky, because S-T interest rates are more volatile than longer rates. Finally, Term Structure Short-term interest rates tend to be lower than long-term rates, so borrowing long-term is costly. This implies that , on average , it is more costly to rely on L-T borrowing than on S-T borrowing.

Seasonal variation S-T financing $ secular growth in fixed Assets and permanent CA Marketable securities ( Appropriate Finance Policy ) Time 절충재무정책에 의하면 회사는 자금이 가장 필요한 고점에서는 단기로 빌리지만, 필요량이 줄어든 시기에는 Marketable Securities 형태로 Cash Reserve 를 유지한다. 유동자산이 비축되면 회사는 단기차입을 하기 전에 Cash Reserve 를 사용한다. 이와 같이 회사는 단기차입에 의존하기 전에 어느 정도 유동자산을 늘릴 수 있다. CASH MANAGEMENT One aspect of working capital management is the evaluation of the tradeoff between the benefits of liquidity and the opportunity cost of foregone interest, i.e., cash management. Effective cash management requires that managers consider (1) how much cash to hold, (2) how to manage cash collections and disbursements, and (3) how to invest excess cash. The goals of the cash manager are simple: "Collect early and pay late" and "Never let money sit idle". The trick is to accomplish these things without (a) angering customers, (b) damaging the firm's credit rating, or (c) running short of cash.

Reasons for Holding Cash The three reasons for holding cash are: precautionary, speculative, and transactions motives. We discuss each as they apply to corporate cash management, and the role of compensating balance requirements. 1) The Speculative motive is the desire to take advantage of investment opportunities which might arise in the future. 2) The precautionary motive is the need to hold cash as a financial reserve in the event of unanticipated cash outflows or unanticipated decreases in cash inflows. Both can be satisfied by reserve borrowing ability and by holding marketable securities, as well as holding cash. 3) Cash satisfies the transaction motive i.e., for regular disbursements and collections. 4) Other business requirement motive: A firm may be required to hold cash for other purposes. This might include balances in a non-interest bearing bank account as a condition of a bank loan or other services for lower or free charges (called “compensating balance”) Finally, it must be remembered that a firm which holds cash in excess of the minimum balance required for transactions and compensating balances incurs an opportunity cost in the form of the interest income foregone by holding cash rather than securities. A firm whose cash balance is too low is subject to the risk of being unable to meet funds needs. The optimal cash balance minimizes the sum of these costs. Pay attention!) Cash not necessary for any of these four purposes should be invested in marketable securities or other interest-earning accounts including money market funds.

Cash operation strategy It should be both in direction that cash inflow should be accelerated, fast or expedited (called “reducing collections float”), whereas cash outflows should be slower or delayed (called “Increasing disbursement float”). Understanding Float The amount of cash on a firm's financial statements (i.e., the 'book' or 'ledger' balance) is not the same as the firm's bank balance (i.e., the firm's 'available' or 'collected' balance). The difference is the float. Checks written by the firm reduce the book balance immediately, but do not affect the available balance until the check is presented to the firm's bank for payment. The difference in the balances is disbursement float. Checks received increase your book balance but do not increase your available balance until payment is actually received by the bank. The difference is collection float. Net float is the sum of collection and disbursement floats. Float management involves speeding collections and delaying disbursements. Float has three parts: mail float (the time during which a check is in the mail), processing float (the time between the receipt and deposit of a check), and availability float (the time required to clear the check through the banking system). The size of the float depends on both the dollar amount and the time delay involved. Larger dollar amounts and/or longer delays increase the size of the float. The cost of float is the opportunity cost resulting from not being able to use the money. A reduction in float has value to the firm, but it is generally costly to reduce it. Procedures for reducing float are described next - adopting a technique is appropriate only if the decision has a positive NPV; i.e., the benefit derived from float reduction exceeds the cost of making the change.

Main techniques used to expedite cash inflows are as follows : The cash collection process entails three steps: mailing time, processing delays, and availability delays. Thus, collection time is equal to mailing time plus processing delay plus availability delay. Because each increases the float costs incurred by the collecting firm, techniques have been developed to reduce collection delays. 1) Invoices should be mailed promptly 2) Lockboxes and cash concentration procedures are popular cash collection techniques. In a lockbox arrangement, a firm arranges for customers to mail payments to a strategically located post office box maintained by a local bank. The bank collects the checks several times a day and deposits them in the firm's account. Lockboxes reduce mailing time as well as the time the firm would spend processing checks prior to making the deposit. Concentration banking systems operate similarly, but in this case the firm's sales offices are used to receive and process checks. Surplus funds are subsequently transferred to the firm's main bank (the "concentration bank"). 3) Electronic Data Interchange (EDI) refers to the direct exchange of data between firms electronically. Financial EDI (FEDI) is the electronic transfer of funds and financial information. Float times will become increasingly shorter as more and more firms go online. There are two kinds of applied EDI in relation to cash transfer as follows: - EFT(electronic funds transfer): is any transfer of funds that is initiated by electronic means, such as electronic terminal, telephone, computer ATM, etc.EFT transfers all payments made over electronic commerce. * Debit card: is a kind of applied EFT. It is a card allowing customers to access their deposited monies immediately and electronically, unlike a credit card, which doesn’t have any float. It is different from cash service (card) of credit card. - ACHs(automated clearing houses): is a nation-wide-electronic funds transfer networks which enables participating financial institutions to distribute bank credits and debits electronically to bank accounts via clearing of checks.

Main considerations when to delay cash outflows are as follows: Collecting firms seek to minimize float time, paying firms seek to maximize it. Doing so reduces required cash balances and the opportunity costs of liquidity. 1) the utilization of a system of zero-balance accounts Controlling disbursements can be accomplished by the utilization of a system of zero-balance accounts under which a safety stock of cash is held in a master account, while various sub-accounts are monitored to maintain a net zero balance. Alternatively, the firm may maintain a controlled disbursement account into which funds are transferred on a daily basis and only in the amount needed in order to meet payment requirements on that day. 2) Payment by draft(a three-party instrument in which the drawer orders the drawee to pay money to the payee) is also means of slowing cash outflows. A check is the most common draft. The draft can utilize the float resulting in delay of payments or cash outflows. Investing Idle Cash Temporary cash surpluses arise largely because of seasonal or cyclical activities, as well as for financing of planned expenditures. Idle cash can be invested in money-marketsecurities (i.e., securities with maturity of less than one year). Most large firms do their own investing, while smaller firms often rely on money-market mutual funds (some of which specialize in corporate cash management). The most important characteristics of short-term marketable securities are their maturity, default risk, marketability, and tax status. Most firms limit their investments in money-market securities to those with maturities of 90 days or less, which reduces interest-rate risk. Firms also prefer highly-rated, liquid securities. Below we describe some popular money-market instruments. 1) Treasury billsare direct obligations of the U.S. government. They are issued with maturities of 90, 180, 270 and 360 days, via auction. State and local governments and agencies also issue short-term debt, but with greater default risk and less marketability than Treasury debt. Since the interest is exempt from federal taxes, the pre-tax yield is lower than for Treasury securities of similar maturity.

2) Commercial paper is short-term, unsecured debt issued by businesses, short-term notes issued by big companies that are very good credit records with maturities ranging from a few weeks to 270 days. However, they may yield a higher return than CDs because it is riskier Since there is no active secondary market for commercial paper, marketability is low. Default risk varies with the issuer's strength. 3) Certificates of deposit (CDs) are time deposits in banks. a form of savings deposit that cannot be withdrawn before maturity without a high penalty. They are short- or medium-term with interest bearing under FDIC-insured debt instrument offered by banks. There is an active market for 3-month, 6-month, 9-month and 12-month CDs. negotiable CDs are sold or transferred to another party under the regulation of the Federal Reserve System. As a result, they are also traded at a secondary market. 4) Money-market accounts is a savings account that shares some of the characteristics of a money market fund. Like other savings accounts, they are insured by the Federal government. 5) Repurchase agreements are transactions involving the purchase of an instrument (usually Treasury securities) and a simultaneous agreement to sell it back at a higher price in the future. 6) Treasury note and bonds: are long-term investments, but issues near maturity are effectively short-term securities with high liquidity.

* CA The target cash balance involves a trade-off between the opportunity costs of holding Too much cash and trading costs of holding too little. ( Cost of holding cash ) Cost in dollar Of holding cash Total costs of holding cash Opportunity costs Trading costs Size of cash balance (C) The optimal size Of cash balance Trading costs are increased when the firm must sell securities to establish A cash balance. Opportunity costs are increased when there is a cash balance Because there is no return to cash. If a firm tries to keep its cash holding too low, it will find itself selling Marketable securities.(and perhaps later buying marketable securities to replace Those sold) more frequently than if the cash balance were higher. Thus trading costs will tend to fall as the cash balance become larger. In contrast, the opportunity costs of holding cash rise as the cash holding rise. at point C*, the sum of both cost, depicted as the total cost curve, it at a Minimum. This is the target or optimal cash balance.

Determination of amount of cash to keep on hand: usually depends on a consideration of • applied EOQ(economic order quantity)’s outcomes as follows: • Applied EOQ can be stated in terms of the following assumptions: • 1) Constant Disbursement Rate • 2) No Cash Receipts during the Projected Periods. • 3) No Safety Stock of Cash is allowed for • William Baumol was the first to provide a formal model of cash management • Incorporating opportunity coats and trading costs. His model can be used to • establish the target cash balance. Starting cash C = $1,200,000 $600,000 = C/2 Average cash Ending cash 0 1 2 3 4 The Opportunity Costs equal to the average cash balance cash balance multiplied by the interest rate, or Opportunity costs($) = ( C/2 ) × I Trading costs be determined by calculating the number of times that A must sell marketable securities during the year. The total amount of cash disbursement during the year is $600,000 × 52weeks = $31.2 million. If the initial cash balance is set at $1.2 million of marketable securities every two weeks. Thus trading costs are given by $31.2million $1.2million × F = 26F

Trading Costs($) = ( T/C ) × F T = Total amount of new cash needed for transactions purposes over the relevant planning periods, say, one year F = The fixed cost of selling securities to replenish cash I = The opportunity cost of holding cash : this is the interest rate on marketable securities Total cost = Opportunity cost + Trading cost = (C/2) × I + (T/C) × F The Baumol model is possibly the simplest and most stripped-down sensible model for Determining the Optimal cash position. Its chief weakness is that its assumes discrete, certain cash flows. EOQ(economic order quantity) The amount of orders that minimizes total variable costs required to Trading cost and Opportunity costs (holding cash). How to apply this EOQ formula to determine what amount of cash to be kept on hand: C* = √(2 ×T ×F) / I

The Miller-Orr Model Merton miller and Daniel Orr developed a cash balance model to deal with cash inflows and outflows that fluctuate randomly from day to day. The model assumes that the distribution of daily net cash flows(cash in flow minus Cash outflow) is normally distributed. We will assume that the expected net cash flow is zero. Buys H-Z units(or dollar) of marketable securities decrease the cash balance to Z Cash H Z Sell Z-L securities and increase The cash balance to Z L Time X Y H is the upper control limit. L is the lower control limit. The target cash balance Is Z. As long as is between L and H, no transaction is made. When the cash balance reaches H, such as at point X then the firm buys H-Z units (or dollar) of marketable securities. This action will decrease the cash balance to Z. In the same when cash balances fall to L, such as at point Y (the lower limit), The firm should sell Z-L securities and increase the cash balance to Z. In both situations, cash balances return to Z. Management sets the lower limit, L , depending on how much risk of a cash shortfall The firm is willing to tolelate.

CREDIT AND RECEIVABLES CREDIT AND RECEIVABLES Granting credit results in the creation of an account receivable for the seller and an account payable for the buyer. Credit management is an important aspect of a firm's short-term financial policy. Components of Credit Policy Credit policy entails terms of sale, credit analysis, and collection policy. 1) Terms of sale consist of: the credit period, the cash discount and the discount period, and the type of credit instrument used. 2) Credit analysis is the process of attempting to distinguish between customers who are likely to make payment on an account and those who are not. 3) Collection policy is the set of procedures the firm uses to collect payment on accounts. - The credit period is the length of time during which the customer must make payment.When a discount is offered, the credit period has two components: the net credit period, which is the total amount of time the customer has to make payment; and the cash discount period, which is the time the discount is available to the customer. Factors to consider when setting the length of the credit period include the buyer's inventory period and operating cycle, collateral value of the goods, product demand, the buyer's credit risk, size of the account, and the level of industry competition. - Cash discounts speed collections of receivables because they provide customers an incentive to pay earlier. Additionally, a discount is a way to charge higher prices to credit customers. - A credit instrument is evidence of indebtedness. Most trade credit is offered on open account, which means the credit instrument is the invoice. The customer signs the invoice when goods are received. Or, the selling firm may require a promissory note, which is a basic IOU. A commercial draft is a demand for payment sent to a customer's bank, along with the shipping invoices. The buyer signs the draft before goods are shipped. If the draft requires immediate payment, it is called a sight draft.

* C If the bank 'accepts' the draft for future payment, it is a banker's acceptance and the bank accepts responsibility for making payment. A firm can also use a conditional sales contract; in this case, the firm retains title to the goods until payment is completed, and payment is often made in installments. Optimal Credit Policy So far we’ve focused on whether a firm should grant or deny credit. Another consideration is the determination of the optimal amountof credit to be granted. We consider two types of costs: carrying costs associated with granting credit and making the corresponding investment in receivables, and opportunity costs which result from not granting credit. Carrying costs include the required return on the investment in receivables, bad debts, and costs of managing credit and collections. Opportunity costs are foregone profits from lost sales due to the refusal to grant credit. The optimal amount of credit minimizes the sum of carrying and opportunity costs. Cost 최적신용공여 Carrying costs opportunity costs 신용공여액

Credit Analysis Credit analysis is the process of estimating the probability that a customer will not pay, and deciding whether to extend credit to that customer. A key consideration is the borrower's credit history. Credit information used to assess creditworthiness can be obtained from financial statements, credit reports, banks, and the customer's payment history. Also, credit reports can be purchased from several sources. The traditional guidelines for assessing the probability of default are the five Cs of credit: character, capacity, capital, collateral, and conditions. - character : 신용채무를 이행하려는 고객의 의지 - capacity : 영업현금흐름으로 신용채무를 이행하려는 고객 - capital : 고객의 금융자산 - collateral: 채무불이행에 대비하여 고객이 담보로 잡힌 자산 - conditions: 고객이 하는 사업의 일반적인 경제상황 Credit scoring is the process of computing a numerical rating as a guideline for assessing creditworthiness. Collection Policy Collection policy is the process of monitoring receivables and obtaining payment of overdue accounts. Two tools used to "monitor" outstanding accounts are the average collection period (ACP) and the aging schedule. The relationship between the ACP and the firm's credit terms indicates whether customers are generally paying accounts when due. Collection effort generally involves a series of steps such as: (1) sending a delinquency letter, (2) calling the customer, (3) hiring a collection agency, and (4) initiating legal action.

MARKETABLE SECURIITES MANAGEMENT . MARKETABLE SECURIITES MANAGEMENT (short-term) marketable securities (e.g., T-bills, CDs, repos, commercial papers. Eurodollars, money market mutual funds of having a portfolio of short-term securities, banker’s acceptance, adjustable rate-preferred stock...etc.) are sometimes held as substitutes for cash but are more likely to be acquired as temporary investments of excess cash in order to take advantage of some reasonable interests with highly safe and high degree of liquidity . Main considerations related to choosing marketable securities are as follows - Most of companies avoid large cash balance due to cost of capital (=opportunity cost) and so prefer borrowing to meet short-term needs. - As temporary investments, marketable securities may be purchased with maturities times to meet seasonal fluctuations, to pay off a bond issue, to make tax payments, or to meet anticipated needs. As a result, short-term marketable securities are usually chosen for reasons that make high-yield, high-risk investments unattractive. - So a higher return may be forgone in exchange for greater safety. Given the various options available, a company should have an investment policy statement to provide continuing guidance to management. Thus, the speculative tactics, such as selling short, which is a borrowing a security from a broker and selling it along with mutual understanding that it must later be bought back(hopefully at a lower price) and returned to the broker, and margin trading, which is a using money borrowed from a broker to purchase a security, generally are avoided. - They should be chosen with a view to the risk of default (=financial risk or credit risk), so that choosing them should be based on the degree of security, such as T-bill is the lowest risk of default instrument. - They should be chosen with a view to the interest-rate risk, which is the possibility of a reduction in value of a security, especially a bond, resulting from a rise in interest rate, in spite that generally short-term securities are less likely to fluctuate in value because of changes in the general level of interest rates reflected already from the market. - The degree of marketability of a security determines it liquidity, that is, the ability to resell at the quoted market price. - The firm’s tax position will influence its choice of securities. Therefore, a firm with net loss carry-forwards may prefer a higher-yielding taxable security rather than tax-exempt municipal bonds.

. 1) Money market fund: is an open-ended mutual funds that will invest only in money market where short-term debt securities with highly safe and liquid , such as banker’s acceptances, commercial papers, repos, negotiable CDs, T-bills with maturity of less than one year or less than 30 days, are traded. 2) Banker’s acceptance: is a short-term credit investment which is created by non-financial firm and whose payment is guaranteed by a bank at its maturity. It is often used in importing and exporting. 3) Repos: is a contract in which the seller of securities, such as T-bills, agrees to buy them back at a specified time and price. It also called “Repurchase agreement”. 4) Municipal bond : is a bond issued by state, or local government 5) Eurodollars : are American dollars deposited at foreign financial institutions outside U.S.A. they are usually used to pay off or for the merchandise bought from overseas company in the country. 6) Commercial paper is short-term, unsecured debt issued by businesses, short-term notes issued by big companies that are very good credit records with maturities ranging from a few weeks to 270 days. However, they may yield a higher return than CDs because it is riskier Since there is no active secondary market for commercial paper, marketability is low. Default risk varies with the issuer's strength. 7) Certificates of deposit (CDs) are time deposits in banks. a form of savings deposit that cannot be withdrawn before maturity without a high penalty. They are short- or medium-term with interest bearing under FDIC-insured debt instrument offered by banks. There is an active market for 3-month, 6-month, 9-month and 12-month CDs. negotiable CDs are sold or transferred to another party under the regulation of the Federal Reserve System. As a result, they are also traded at a secondary market. 8) Treasury billsare direct obligations of the U.S. government. They are issued with maturities of 90, 180, 270 and 360 days, via auction.

INVENTORY MANAGEMENT Inventory management Inventory accounts include raw materials, work-in-process, and finished goods. Smaller businesses often use a revolving line of credit to finance their merchandise inventory. Work-in-process inventory has a lower marketability than other types of inventory and may therefore be more difficult to finance. Centralizing and coordinating inventory purchasing activities may lower inventory levels and related cost of carrying the inventory. Inventory management attempts to minimize total ordering, carrying(holding) costs, and stock-out costs. I.e., The firm must also minimize the sum of the costs of stock-out and safety cost. Safety cost is the quantity held for sale during the lead time. Lead time is the period between when an order is placed and when it is received. Carrying costs include storage costs for inventory items plus Opportunity costs (I.e., the cost incurred by investing in inventory rather than making an income-earning Investment.) Examples are insurance, spoilage, interest on invested capital, Obsolescence and warehousing costs. Ordering costs Are costs incurred when placing and receiving orders. Ordering cost include purchasing Costs, shipping costs, setup costs for a production run, and quantity discounts lost. ( Cost of holding Inventory ) Cost in dollar Of holding Inventory Total costs of holding Inventory Carrying costs Shortage costs Q (order quantity) Q* The optimal size Of Inventories

Carrying costs include costs of storing and insuring inventory as well as losses due to • obsolescence and theft, and the opportunity cost of funds invested. • Shortage costs are incurred when the firm must continually restock, or when sales are • lost due to inability to fill orders. Carrying costs는 보통 재고자산 수준에 정비례한다고 본다. Starting Inventory Q = 3,600 Q/2 = 1,800 Average Inventory Ending cash Week 0 1 2 3 4 5 6 7 8 Q를 매번 주문하는 재고자산의 양(3,600개) 평균재고자산은 Q/2 또는 1,800개 연간 단위당 보유비용을 CC라고 하면 총재고 보유비용 = 평균재고자산 × 단위당 보유비용 = ( Q/2 ) × CC Shortage costs 재고보충비용에만 초점을 맞춰 Safety stock과 관련된 비용은 중요하지 않도록 하기위해 기업은 재고자산이 부족하지 않고, 재고보충비용(Shortage costs)은 통상 고정되어있다고 가정한다. 기업의 연간 총 매출량, T, 기업이 매번 Q개의 주문한다면 총 T/Q 회의 주문을 해야 할 필요가 있다. 46,800 / 3,600 = 13회 주문 각 주문당 고정비용을 F라 하면 Shortage cost = 주문당 고정비용 × 주문횟수 = F × ( T/Q )

The Economic Order Quantity (EOQ) Model The EOQ model is a cost-minimization approach to inventory management. Let total costs be equal to carrying costs + shortage costs; i.e., Total inventory cost costs = (Avg. inventory Carrying costs per unit) + (Fixed cost per order Number of orders) = [(Q/2) CC] + [F (T/Q)]. 정확하게 비용을 최소화하는 양을 찾기 위해 (Q*/2) × CC = F × (T/Q*) (Q*)2 = 2T×F/CC Q* = [(2T F)/CC]1/2 - - - - EOQ (economic order quantity) EOQ(economic order quantity) The amount of orders that minimizes total variable costs required to Carry cost and order costs. Ex-1) Aldine uses 100 units per year. The unit order cost is $4 and the carrying cost $2. Calculate the EOQ. Answer) ({$4x100x2}÷$2) = 400 = 20 units Ex-2) Aldine uses 10,400 units annually and has an order quantity of 2,000 units. Its safety stock level is 1,300 units, and there is an order-delivery lead time of 4 weeks. What is the re-order point? Answer) Average usage per week: 10,400 units ÷ 52weeks(52x7=364 days/365 days) = 200 units Average usage per lead time: 200 units x 4 weeks = 800 units Per re-order point: 800 units + 1,300 units = 2,100 units.

Ex-3) Aldine’s planning managers, CMA and CFM, want to quantify the annual carrying cost of its safety stocks of 50 units. The inventory investment per unit is $20 and the carrying cost approximately 25% of the investment. Inventory is ordered 10 times a year. The probability of a stock-out is 15% and the related cost is $5 per unit. What is the total cost of 50 units of safety stock? Answer) Safety stock cost= carrying cost + expected stock-out cost Carrying cost: 50 units x $20 investment per unit x 25% carrying cost = $250 Expected stock-out cost: 15% probability x 50 units x $5 stock-out cost per unit x 10 orders per year = $ 375 Total cost of 50 units of safety stock: $250 + $ 375 = $625 The EOQ model can be extended to include such factors as the holding of safety stocks, as well as the determination of optimal reorder points. Q 최소재고자산수준 Safety Stock Time 0 Safety Stock이란 기업에 수중에 유지하는 재고자산의 최소수준 Q Re-order point Time 0 Delivery time Re-order point는 기업이 실제로 재고자산을 주문하는 시점이다. 재고자산이 0에 도달하는 것으로 예측되기 며칠(또는 몇 주,몇 달)전에 발생한다.

Q Time 0 Delivery time Safety stock과 Re-order point를 결합함으로써 기업은 예상치 못한 사건에 대한 완충장치를 유지한다. Managing Derived-Demand Inventories Inventory levels based on "derived-demand" inventory management techniques such as "materials requirement planning" (MRP) systems are determined by anticipated finished goods requirements. Once a finished goods forecast is in hand, we estimate the level of work-in-progress and then raw materials necessary to meet the firm's needs. Just-in-Time (JIT) is another derived-demand technique in which the firm orders inventory only to meet immediate production needs. As a result, inventory holdings are minimized.

SHORT-TERM BORROWING SHORT-TERM BORROWING : Short-term credit is debt scheduled to be repaid within 1 year. 1)Unsecured Loans Short-term borrowing used to cover a temporary cash deficit often takes the form of an unsecured short-term bank loan. Such loans are usually arranged as either a non-committed or a committed line of credit. The former is an informal agreement allowing the firm to borrow without submitting the usual paperwork. The latter is a formal agreement specifying that the bank will lend up to a specified amount to the firm in return for a fee based on the committed funds. 2)Secured Loans Secured short-term loans require either accounts receivable or inventories as security for the loan. With accounts receivable financing, accounts are either 'assigned' or 'factored.' If factored, they are sold to a lender who assumes the risk of customer default. Under assignment, the lender has a lien on receivables, and the borrower is responsible for bad accounts. - Factoring: is the selling of a company’s accounts receivable at a discount price to a factor, who usually assumes all credit risk and receives cash when the debtor clears his account. This financing source is very high cost required….usually about two or three or more above the prime rate plus a fee for collection. Pay attention!) The general factoring transaction procedures are as follows: In factoring agreement of 2% fee, 18% interest and 90% advance with the company of having $100,000 monthly credit sales at credit terms of net 60 days, the factor will advance 90% of the receivables submitted by the firm after deducting the 2% fee and then the interest 18% for the remaining while keeping 10% as reserve till net due is over as follows: $90,000($100,000-$10,000)-$2,000($100,000 x 2% fee)= $88,000 $88,000-$2,640($88,000 x 18%)= $85,360 in advance, and $10,000 only after credit due date (60 days) unless sales return and allowances occur.

- Pledging receivables: bank loan may be secured by pledging receivables, which is an offered receivable to a lender as collateral for the loan. Usually the bank lend up to 80% of the asset’ value. - Chattel mortgages: are loans secured by a movable property, which includes all properties, except properties related to real estate, such as equipment, office furniture…etc. - Float lien: is a general lien against a set of assets, such as inventory, accounts receivable..etc., in which the assets aren’t specifically identified. 3) Inventory loans are secured by inventory. - A blanket lien is a lien against all inventory. Trust receipt arrangements identify specific inventory items as collateral. Field warehousing arrangements segregate inventory for use as security and place it under the control of an independent third party. - Warehouse financing: uses inventory as security (=collateral) for the loan. A third party, a public warehouse, usually holds the collateral and serves as the creditor’s agent, and the creditor receives the warehouse receipts evidencing its rights on the collateral. 4)Other Sources Commercial paper consists of short-term notes issued by large, highly-rated firms; maturities are short, generally less than 270 days. Another source of financing is trade credit, which is equivalent to borrowing from suppliers, spontaneous financing because it arises automatically as part of the purchase transaction. COST OF BANK LOAN 1) Regular interest formula Interest / Borrowed amount 2) Discounted interest Interest /〔 Borrowed amount – Interest 〕 3) Installment loan Interest / Avg. borrowed amount

Another source of financing is trade credit, which is equivalent to borrowing from suppliers, spontaneous financing because it arises automatically as part of the purchase transaction. Accrued expenses are another source of spontaneous financing. Accruals such as salaries, wages, interest, dividends and taxes also represent an interest-free method of financing because no interest accumulates until the due date, for example, payday for workers or the quarterly time set for payment of federal income taxes. Accruals have the additional advantage of fluctuating directly with operating activity. CASH DISCOUNT 판매조건의 하나로써 Cash discount를 제공하는 이유는 매출채권의 회수를 가속화하기 위한 것이다. 이는 제공되는 신용금액을 줄이는 효과가 있을 것이고, 기업은 이를 할인비용과 견주어 결정해야 할 것이다. 현금할인의 또 다른 이유는 현금할인이 신용을 받는 고객들에게 더 높은 가격을 부과하기위한 수단이라는 것이다. 이런 의미에서 현금할인은 고객들에게 신용을 부담하게 하는 편리한 방법이다. < 2/10, net 30 > 조기지불로 구매자들은 2%의 할인을 받는다. 이것이 조기지불에 대한 충분한 유인이 되는가? 내재된 이자율이 매우 높으므로 충분한 유인이 된다. 1,000달러를 주문했다고 하자. 구매자는 10일째에 980달러를 지불하거나 20일을 더 기다려 1,000달러를 지불할 수 있다. 구매자는 사실상 20일 동안 980달러를 빌린 “대출”에 대해 이자로 20달러를 지불하는 것이다. 이자율은 얼마인가? $20 / 980 = 2.0408 % 이다. 비교적 낮지만 20일 동안의 이자율임을 기억하자. 1년에 그런 기간은 365 / 20 = 18.25회가 있으므로 할인을 받지않음으로써 구매자는 사실상 다음과 같은 실효이자율을 지불한다.

Ex) 2/10, net 30 means that the total payment period is 30 days, the discount period is 10 days, and the discount rate is 2%. - A Straight-effect method used to calculate the cost of not taking a discount: (360{bank’s year}÷not discount period) x (discount rate÷{100%-discount rate}) (360 days÷20 days) x (2%÷98%)=18 x 0.02= approx. 36% annualized interest cost of not taking discount. - A Compound-effect method used to calculated the cost of not taking a discount: [ 1.0+(discount rate÷{100%-discount rate})]ª– 1.0 [1.0+{2%÷98%}]18-1.0= approx. 44% annualized I.C. of not taking discount.