Download

1 / 20

200 likes | 466 Views

IMPACT OF ECONOMIC SLOWDOWN ON INDIAN POWER SECTOR. C O N T E N T S. ECONOMIC SLOWDOWN. CORPORATE INDIA ON THE SLIDE. IMPACT ON T & D SECTOR. POWER SECTOR SCENARIO. EFFECT ON ELECTRICAL INDUSTRY. RECOMMENDATIONS TO ENHANCE T&D SECTOR. CREDIT AND EQUITY MARKET CRISIS.

E N D

IMPACT OF ECONOMIC SLOWDOWN ON INDIAN POWER SECTOR

C O N T E N T S ECONOMIC SLOWDOWN CORPORATE INDIA ON THE SLIDE IMPACT ON T & D SECTOR POWER SECTOR SCENARIO EFFECT ON ELECTRICAL INDUSTRY RECOMMENDATIONS TO ENHANCE T&D SECTOR CREDIT AND EQUITY MARKET CRISIS CHALLENGES FOR SURVIVAL SILVER LININGS WAY FORWARD

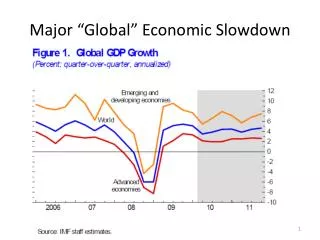

ECONOMIC SLOWDOWN • 2008 – UPHEAVALS IN GLOBAL ECONOMY, Failures of financial institutions, credit crunch, Government interventions. • Has affected virtually all markets and sectors across the globe. • Indian economy cannot be completely insulated from global slowdown. • India Inc. posted of its worst performances in Q3 2008-09

CORPORATE INDIA : ON THE SLIDE Source: India Infoline

POWER SECTOR SCENARIO • Power sector is one of the few industries unfazed by the ongoing economic meltdown. • Both top and bottom lines have shown significant improvements. • NTPC, Power Transmission Corporation and Torrent Power showed strong profits and sales growth during Q3. • NTPC registered 26.5 % increase in net profit to Rs 2,251 crore, with sales increasing by 20.8 % to Rs 11,277 crore.

POWER SECTOR SCENARIO • Project cost escalations are likely to come down with the decline in commodity prices and interest rates • Tightness in equipment supply is no longer a major concern. • Tightness in the availability of manpower, both skilled and un skilled, has eased over a past few months. • Most banks and institutions believe that the power sector has one thing going for it-demand is not an issue and hence, financial closure will not be an issue for good projects.

IMPACT ON T & D SECTOR • Order book position remains robust: All the major companies in transmission section currently holds a robust order book size of Rs. 123 bn. • New order inflow to come, mainly driven by PGCIL: In Indian market alone, Rs 57.9 bn worth of active tenders are open in transmission sector. The Major portions of Rs 30.2 bn are from transmission tower- Rs 21.16 bn from Substation and rest are from the rural electrification segments. • REC and PFC funded private line projects worth Rs 60 bn are due for bidding. Also Rs. 80 bn NHPCL orders are still pending. We don’t see any slowdown or order inflow from domestic market in near term future.

IMPACT ON T & D SECTOR • SEBs and Private Transmission Companies: No clear picture: The order flows from SEBs are also likely to be impacted due to the election and funding issues. Due to the market meltdown and liquidity crunch in the overall economy, we believe the project capex are likely to be deferred and hence we do not see any near term order inflow from the private sector in India. • PGCIL Investment Plan: Only positive booster – According to Industry boosters there is no indication of slowdown seen in order flowing from PGCIL. PGCIL is going to spend Rs 85 bn in FY09E and Rs 100 bn in FY10E. • International Markets: Slowdown expected: African and Middle East markets with the cooling down of crude oil prices and bid dependence of these economies on commodities, the order inflow is likely to get impacted in near future.

IMPACT ON T & D SECTOR • Borrowing cost and liquidity issues to impact margins: Transmission tower sector is a working capital intensive industry. Due to the current liquidity crunch, the companies may find it difficult to meet its working capital requirements. • Easing of commodity prices to benefit fixed contracts.: With the easing of inflation, the key raw material prices like steel (-80% of total raw material cost) have corrected considerably from the highs of April 2008. This will help the EPC players in improving their margins as well as their working capital position. But the significant benefit will be derived by the players which has more exposure to the fixed price contracts. • Foreign currency fluctuation: Depreciating rupee to improve margins: The foreign currency having appreciated significantly in recent period has led to significant translation loss booked by the companies on the advance from customers and external borrowings. companies which are net exporters depreciated rupee will actually help the companies in improving the margins.

EFFECT ON ELECTRICAL INDUSTRY Though there is no slowdown or deferment in power and T&D Segment and the only slowdown seen in the industrial segment. Overall cumulative growth of electrical industry shows negative trends. • Q3 of FY 08-09 shows 1.76% decline from 7% growth registered in previous quarter. • Growth index of major electrical equipments

EFFECT ON ELECTRICAL INDUSTRY • Positive growth – HT motors, power transformers, HT circuit breakers, power cables, conductors. • Negative growth – LT motors, LV switchgear, LT capacitors, Energy meters. • Though Govt’s thrust is on capacity addition, main factors affecting power equipment industry are: a. Difficulty in credit availability. b. Decline in export orders. c. Growing imports.

EFFECT ON ELECTRICAL INDUSTRY • Hit by –ve growth of 6.6% in the current fiscal, the electrical and Electronic Industries has urged Govt. to provide financial and policy initiatives to achieve targets. • In a pre-budget memorandum to the Finance Minister, IEEMA has appealed that, Govt. should treat Power sector as a full fledged infrastructure sector and extend all policy and fiscal support to it. • Benefits under sections 80 I – A of IT act should be extended in full to new Power Plants. • Tax exemptions are available to other infrastructure activities in rural areas such as water supply and sanitation or rural area development scheme, but such breaks have not been granted to RGGVY. This would bring down cost of scheme to 25 % thereby enabling electrification of more villages.

RECOMMENDATIONS TO ENHANCE T&D SECTOR • Clarity on funding arrangements at utility level (e.g: current MSETCL’s strategic alliance project) • Pre-qualification requirements need to be relooked by SEBs/utilities. • Vendor development programmes to be undertaken by utilities to develop contracting agencies. • Establishing a project monitoring cell at utilities to focus on project job. • Standardisation of commercial terms and conditions. • Standardisation of Design and Engg. across the boards.

CREDIT AND EQUITY MARKET CRISIS • In the current year, the fundamental factor which will impact the power sector would be the global ( and now Indian )impacting the Power sector will be the Indian credit and equity market crisis. • The first casualty of this crisis will be the large number of Pvt. Sector Power projects. • Current credit crisis will sharply reduce access to credit for Pvt. Sector projects. • In 2009 very little progress will be achieved on Pvt. Sector BOT projects.

CREDIT AND EQUITY MARKET CRISIS • Govt. will have to think of innovations like pre arranging debt and equity support package to ensure take off of Projects. • The Govt. would also need to consider increasing its focus on Govt. funded projects being set up by PSUs such as NTPC. • The authorities could use 2009 to address some of the existing problems plaguing the sector like tie-up for fuel and taking concrete steps to alleviate funding constraint. A transparent and objective bid process for allocation of coal linkages and coal blocks to be put into place. • Investment in APDRP scheme will provide business opportunities for equipment suppliers and contractors.

CREDIT AND EQUITY MARKET CRISIS To sum-up: • 2009 will pose several challenges for private Investment in India and hence Govt. will be required to take concrete steps to alleviate funding constraints for private sector projects. • Govt. will also be required to renew its focus on Govt. investment in Generation, Transmission and Distribution sectors.

CHALLENGES FOR SURVIVAL Though Govt’s. thrust is on capacity addition, main factors affecting speedy growth are: • Dearth of boiler, turbine, generator manufacturers. (India would require minimum 3 more power plant equipment manufacturers having capabilities and credentials similar to BHEL) • Quality of Chinese power equipment manufacturers • Unavailability of finance & credit facilities. • Limited coal and gas reserves in India • Poor infrastructure- ports, roads, railways (making evacuation of imported coal from ports to users difficult) • Availability of skilled manpower. • Delay in commissioning of Generation projects.

WAY FORWARD • State Govts, Railway ministry, Coal ministry to work hand-in-hand. • GoI to grant stimulus packages to grids • Ensure timely financial closures by a. Fund raising by IIFC through issue of tax-free bonds. b. Reduce interest rates of Banks. c. Remove cap on lending by Banks to Power sector. • Solar and hydel energy ventures to be tapped. • Provide funds from Foreign exchange reserves, tapping PF and pension accounts fund, long term funds available with insurance companies. • PFC, REC, IDFC etc. to open up their funding for private sector projects.

SILVER LININGS • 15 states have corporatized their SEBs. • A recent change made by CERC to increase ROE from 14 % to 15.5 % is a positive step that will allow central sector utilities to add more capacity in 12th plan period or beyond. • PFC to explore lending opportunities in setting up/expansion if equipment manufacturing ventures. • No indication of slowdown seen in orders flowing from PGCIL. • Active tenders worth Rs 57.9 bn are open in transmission sector. a. Transmission tower : Rs 30.20 bn b. Sub-station : Rs 21.16 bn c. Rural Electrification : Rs 6.54 bn • For Exporters, depreciating rupee will improve margins. • Easing of commodity prices will benefit fixed price contracts. • Decline in commodity prices and interest rates. • RBI has increased liquidity in last 3 months.