Download

1 / 34

340 likes | 488 Views

Avoiding Common Mistakes To err Is human But quality review is divine . Dec. 7 2013. Agenda. Purpose of this session Sources for presentation Federal “Challenges” Oregon “Challenges” TaxWise “Challenges” What did we miss?. Purpose.

E N D

AvoidingCommon Mistakes To err Is human But quality review is divine Dec. 7 2013

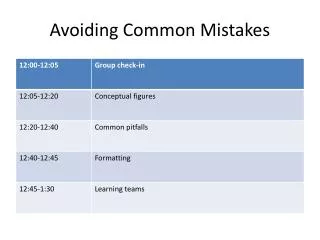

Agenda • Purpose of this session • Sources for presentation • Federal “Challenges” • Oregon “Challenges” • TaxWise “Challenges” • What did we miss?

Purpose • To give Instructors a few points for emphasis in training with the objective of improving our overall quality

Sources for Presentation • DC’s, LC’s, CASH Volunteers • U.S. Treasury Inspector General for Tax Administration (TIGTA) Audit Report • http://www.treasury.gov/tigta/auditreports/2013reports/201340110fr.html • Volunteer Tax Alerts (VTA) and Quality Site Requirement Alerts (QSRA) • http://www.irs.gov/Individuals/Quality-and-Tax--Alerts-for-IRS-Volunteer-Programs (Current Year) • http://www.irs.gov/Individuals/Previous-Year-Quality-and-Tax-Alerts-for-IRS-Volunteer-Programs (Previous Year) • Quality Statistical Sample Review Report Filing Season 2012

Federal Challenges • Interview and Quality Review Procedures 13614-C • Taxpayer Information • Scope • Filing Status • Exemptions • Income • Adjustments • Tax Deductions, Credits • Payments • Amount you Owe

Interview and Quality Review Procedures • Inconsistent Adherence to Quality Procedures leads to Inaccurate tax returns (TIGTA Audit Report) • Not obtaining sufficient information to apply tax law correctly • Not following intake/interview procedures • Not following quality guidelines • Not applying tax law correctly • QSRA 2013-03 • All volunteer return preparers supporting TCE programs must use Form 13614-C, Intake/Interview & Quality Review Sheet for every taxpayer.

Interview and Quality Review Procedures • Verification of the taxpayers’ identity to avoid the potential for identity theft or tax fraud. (QSRA) 2013- 01 • Advising taxpayers of their ultimate responsibility for information on the return. • Explaining the tax return preparation process to the taxpayer and encouraging him or her to ask questions throughout the interview process.

Interview and Quality Review Procedures • Completing Form 13614-C. • Confirming the taxpayer’s responses provided on the Form 13614-C. • Reviewing supporting documentation and confirming with the taxpayer that all income was discussed. • Exercising due diligence, including asking a taxpayer to expand on information that may not appear to be true or accurate.

Quality Review Procedures • In the TIGTA Audit, all 19 tax returns prepared incorrectly did not follow one or more of the quality review requirements. • For 16 (84 percent) incorrect tax returns, quality reviewers did not review the entire Form 13614-C. • For 12 (63 percent) incorrect tax returns, auditor/client was not involved in the quality review process. • For four (21 percent) incorrect tax returns, no quality review was performed.

Brainstorm Ideas – 5 minutes • Form teams of 3 • Each team identify two mistakes that you see frequently

Taxpayer Information • Misspelled names, especially for the Hispanic hyphenated last names • Not checking an ITIN letter for the correct spelling, as defined by the IRS, of the taxpayers name • Incorrect addresses – be sure to verify address from the 13614-C and not just let it default from prior year. Double check apartment numbers/letters. • Incorrect Social Security Numbers (Information worksheet, EIC, Education Credit)– often transposed digits, hard to catch, need to read backwards

Taxpayer Information • Incorrect Date of birth, particularly for dependants • Failure to enter a taxpayer phone number and/or cell phone number (Makes it tough to contact them if there is a problem!!!!!) • Failure to change a W-2 to reflect the SSN being used by an immigrant who is filling using an ITIN. • Watch out for “carry forward” information that is no longer correct such as a dependant.

Scope • Current scope for Program – be sure to emphasize what is and what is not in scope • Volunteer Portal, TaxLaw Training, Training Documents tab, In and Out of Scope Poster C2467 and AARP Tax-Aide Scope Manual TY13 • We are not obligated to prepare all tax returns for all taxpayers. Denying service is not easy, but if you feel the taxpayer is: • providing misleading information; • the return is out of scope; or • you just aren’t comfortable with the return; Don’t do it!!!!!

Filing Status – New Chart • Dependents/HoHversus Single/EIC • Special considerations for child with divorced or separated parents • Custodial parent cannot give HH, CDCC and EIC to non-custodial parent • A child does not have to be a dependent to be claimed as a Qualifying Child for EIC purposes • Difference between Qualifying Child or Qualifying Relative

W2 & 1099 Income • Failure to override the W2 address if it is different from Main Info address • Failure to enter the correct EIN and spelling of business name on W2 or 1099 • If income from a 1099R is for a disability payment, be sure to check the box that will classify payment as wages. • Failure to enter withholding correctly.

Self-Employment Income • Accuracy rate for Schedule C expenses was 69 % in the TIGTA Audit. • Preparers are omitting cash income or are erroneously reporting self-employment income as other income on Form 1040, line 21. (Most common error in QSS Audit) • Exception for Grandparents receiving payments for child care of grandchildren is reported as miscellaneous income (unless they are doing childcare as a business.) Tax court ruling: http://nafcc.org/media/pdf/businessCenter/SteeleCase.pdf

Self-Employment Income • You can't deduct phone expenses for the first phone line. Reference is 2012 Pub 535 page 46. • Self-employed tax payers, using their car within their metropolitan area (aka tax home), who are not claiming business use of home, cannot claim business mileage for the trip from their home to their first business contact nor can they claim business mileage for the trip from their last business contact to their home. Reference is 2012 Pub 17 page184-185.

Refund of State and Local Taxes • If there was a state refund received from last year’s taxes, this may be taxable to the feds if the taxpayer itemized the prior year. • If it's an Oregon refund that is taxable to the feds, this is not taxable to Oregon. • If it's another state refund that is taxable to the feds, this is taxable to Oregon too.

Adjustments • Educator Expenses – Accuracy rate for the Educator Expense deduction was 54% in the TIGTA Audit. • Qualifying Educator for grades K-12. • Educators may subtract up to $250 of qualified expenses. This deduction is available whether or not the taxpayer itemizes deductions. • Volunteers did not include the deduction on the auditors’ tax returns because they did not completely review the Form 13614-C

Adjustments • IRA - the accuracy rate for the IRA adjustment was 46% in the TIGTA Audit. • VTA 2013-02 February 26, 2013 highlighted the IRA • Taxpayers can reduce taxable income by contributing money up to a limit to a traditional IRA. Contributions to IRAs can be made as late as the first due date of a tax return and can be considered retroactive to the previous tax year. • Volunteers did not include this deduction because they did not completely review the Form 13614-C.

Tax, Deductions & Credits • Volunteers incorrectly denied deductions and credits on returns because supporting documentation was not provided. • There are no specific guidelines requiring that taxpayer provide receipts to volunteers to support the deduction or credits claimed. • Be sure to warn taxpayers that if the IRS asks for documentation, they need to be able to document deductions. • If there was a state tax balance due from last year’s return, this can be a deduction on federal Schedule A • Portland Arts Tax is a new deduction….

Education Credits When Scholarships exceed qualified educational expenses on a 1098-T, the difference is taxable to the feds. You may be able to subtract this on Oregon using the "Taxable Scholarships Used for Housing Expenses" Subtraction (subtraction code 333).

Education Credits Here is one example for 2013: Client has a 2013 1098-T that shows $3000 tuition paid and $5000 in scholarships received. They had $500 expenses for text books purchased from Amazon that were not a condition of enrollment but were needed for courses and $1000 for housing. They are fully qualified for an American Opportunity Credit. • Is there a taxable scholarship in 2013? How much? • Yes. $5000-$3000-$500= $1500 on 1040 Worksheet 1 • Is there an education credit in 2013? What are the adjusted qualified Educational Expenses? • No, $0 • Is there any subtraction needed for Oregon purposes in 2013? • Yes, OR Subtractions, Code 333 $1000 for housing to offset taxi

Education Credits In 2014, the 1098-T shows $3000 tuition paid and no Scholarship. There were $500 expenses for text books purchased from Amazon that were not a condition of enrollment but were needed for courses and $1000 for housing expenses. They are qualified for the Lifetime Learning Credit this year. • Is there a taxable scholarship for 2014? • No • Is there any subtraction needed for Oregon purposes in 2014? • No • Is there an education credit for 2014? What are the adjusted qualified Educational Expenses? • Yes . $3000

Credit for Qualified Retirement Savings Contribution • Only 62% of the TIGTA audited returns had the credit correct • Taxpayers may be eligible for this credit if they made deferrals to a 401K or an IRA or other qualified plan and have AGI of less than $28,750 (Single), $43,125 (HOH), $57,500 (MFJ). Use form 8880 • Volunteer Tax Alert 2013-02 February 26, 2013 http://www.irs.gov/pub/irs-utl/VTA_2013-02_Retirement_Savings_Contributions.pdf

Amount You Owe - Penalties • Penalty calculations are out of scope for both Federal and Oregon. • Volunteers sometimes don’t notice that a penalty has been assessed. • If TaxWise is calculating a penalty for federal, go to the 2210 pg 1 form and type a 1 in line 8 in the blank after "2012 tax:" If TaxWise is calculating a penalty for Oregon, go to the OR 10 pg 1 form and type a 1 in line 8 "Enter the tax shown on your 2012 return after nonrefundable and refundable credits - see instructions."

Amount You Owe - Penalties • Always tell clients that there almost assuredly will be penalties and interest for underpayment; it's just that calculating them is out of our scope. Also tell clients to expect a letter from Oregon and/or federal. • Investigate ways to avoid the penalty and interest in the future. Increasing the amount of withholding is an option. Alternatively, discuss and set up Estimated Tax payments in TaxWise.

State Challenges • Federal Pension – tax exemption and box 2 on 1099 checked • Retirement Credit – check box 1 on 1099 (often defaulted) • Itemizing for a taxpayer to limit their Oregon liability even when it doesn’t benefit the federal return • Don’t forget Special Oregon Medical Subtraction if over 62 (taxpayer doesn’t have to reach itemized deduction threshold to benefit) • Forgetting to subtract federally taxable scholarship income that was used on rent • Knowing about Elderly Rental Assistance

ERA Program for Oregon • While few people qualify due to income and asset limitations, this program is for the very neediest seniors • You or your spouse/registered domestic partner(RDP) were age 58 or older on December 31, 2013; and • You and your spouse’s/RDP’s household income was under $10,000; and • You paid more than 20 percent of your household income for rent, fuel, and utilities; and

ERA Program for Oregon (Cont’d) • The total value of you and your spouse’s/RDP’s household assets is $25,000 or less (if you or your spouse/RDP are age 65 or older on December 31,there is no limit on the value of household assets); and • You rented an Oregon residence that was subject to property tax or PILOT; and • You lived in Oregon on December 31; and • You didn’t own your residence on December 31

TAXWISE • Do not override income for social security wages and Medicare wages on W2 when there is a contribution to a retirement account (Box 12, code D-G). Enter box 12 code and they will be calculated correctly. • Put estimated payments in the right place on the form: Line 63 linked to F/S Tax Paid worksheet in TaxWise. • Resolve all “red” entries in the forms tree. • Fill out the Capital Gains Worksheet correctly. • Enter an explanation at the bottom of Main Info (carries forward next year) or the Taxpayer Diary (Date/Time Stamp each entry) for Rejected and Waiting for Info returns • Remember to set return status and efile creation correctly. An example: missing a spouse’s signiture and not setting status to that with an efile ready to go.

Review from Brainstorming What did we miss from initial brainstorming session?