Download

1 / 21

210 likes | 321 Views

Reform Options. Federal Subsidies Debt or Taxes Doesn’t address fundamentals Part of most PRA plans Payroll tax increases 12.4% - 19% (2075) to close gap Benefit Reduction Equal application?. Expanding Tax Base Earned Income Cap (10% - 15%) State & local employees

E N D

Reform Options • Federal Subsidies • Debt or Taxes • Doesn’t address fundamentals • Part of most PRA plans • Payroll tax increases • 12.4% - 19% (2075) to close gap • Benefit Reduction • Equal application?

Expanding Tax Base • Earned Income Cap (10% - 15%) • State & local employees • Long run liability of additional workers • Savings Options • Centralized (Trust Fund investment) • Decentralized (Personal Retirement Accounts) • Blended • Adjustments to the SS Forcast • GDP growth rate (1%) • Inflation (3.3%) • Could add 10 years to insolvancy date

Methods of Benefit Reduction • Retirement age adjustment • Increasing FBA • Longevity trends since 1950 • Men +3.6 years, Women +4.2 years • Equal application • Increasing EEA • Changes in retirement behavior (RHR) • Would hurt those who must retire early

Indexation (COLA) • Most opaque (politicaly feasable) • Would hurt oldest recipients the most • Direct reduction • AIME to PIA (benefit) calculation • Replacement Rate (42% - 38%) • Income testing • Appropriate for “insurance” payout • Would not affect those most in need • SS income already taxed at lower rate

Privatization Cooper Caillier Warren Whippo

What is Privatization? • Privatization - the partial or full replacement of the current pay-as-you-go system with voluntary or mandatory personal accounts • Investments – wide array of government and private securities, including equities

How it would work… • Treasury issues new debt to pay the benefits of existing retirees. • Next generation of workers (todays children) saves for retirement in personal accounts • Next generation of retirees (todays workers) consumes their accumulated personal account balances • Treasury services a larger stock of national debt

Typical Privatization Argument… • Historically, a portfolio of 50% stocks, 30% corporate bonds, and 20% gov’t bonds has produced real returns of about 5% per year1 • Social Security’s real return equal to about 1% per year2 [1] According to Ibbotson’s Cost of Capital Center [1] This estimate is taken from Steven Caldwell, Melissa Favreault, Alla Gantman, Jagadeesh Gokhale, Thomas Johnson, and Laurence J. Kotlikoff, “Social Security’s Treatment of Postwar Americans,” NBER Working Paper 6603. Other studies find somewhat higher returns, but most estimates are below 2%.

Privatization Cont/d… • At face value, this switch to privatization seems lucrative • From an individual perspective, it would boost expected returns • From a macro perspective, it would help make the Social Security system more solvent over the long run b/c it reduces the contributions required to enjoy adequate living standards during retirement

Too good to be true… • Privatization is no free lunch from individual or macro perspective • A macro level, privatization can only increase national income if it raises national savings, which would boost size of capital stock. Or if it improved capital allocation, which would boost the productivity of the capital stock.

No free lunch cont/d… • In practice, this is unlikely b/c the Treasury would have to issue one dollar of additional debt for each dollar that is diverted from payroll taxes into personal accounts • Improved capital allocation is unlikely b/c there is little reason to expect new investors to make systematically better investment decisions than existing investors • If national income really is unchanged than privatization merely reallocates risk and expected returns b/w different parts of the population

Confusion about risk-adjusted returns… • The comparison b/w the historical returns on equities and bonds is misleading • Economic theory tells us that risk adjusted returns of different financial assets should be equal; otherwise there is an arbitrage opportunity which will eliminate the gap

What does this mean for an investor of average risk aversion? • The advantage from higher expected returns offered by the riskier assets is exactly offset by the disadvantage of more risk • So, the higher expected returns that are available from investing in risky assets will not necessarily make personal accountholders better off

The real question… • Is it desirable for low and middle-income workers to share in the risk and returns of equities to a greater degree ? • Are we comfortable with a system that redistributes resources toward lower-income households if the markets and the economy to reasonably well in coming decades, but redistributes resources away from lower-income households if the markets and the economy do very poorly?

Analyzing S.S. low ‘rate of return’… • We could switch to a system of personal accounts, finance the transition by borrowing, and thereby swap the unfunded liability for a larger stock of explicit Treasury debt. This would improve expected returns from the perspective of the individual worker.

But… • But it would also require higher taxes to service the now larger stock of national debt. In other words, it would replace one drag on living standards (the unfunded liability) with another (the additional Treasury debt), leaving us neither better nor worse off.

Conclusion… • The difference between the historical rate of return on equities and bonds and the rate of return on Social Security contributions does not necessarily imply that individuals would be better off in a privatized system.

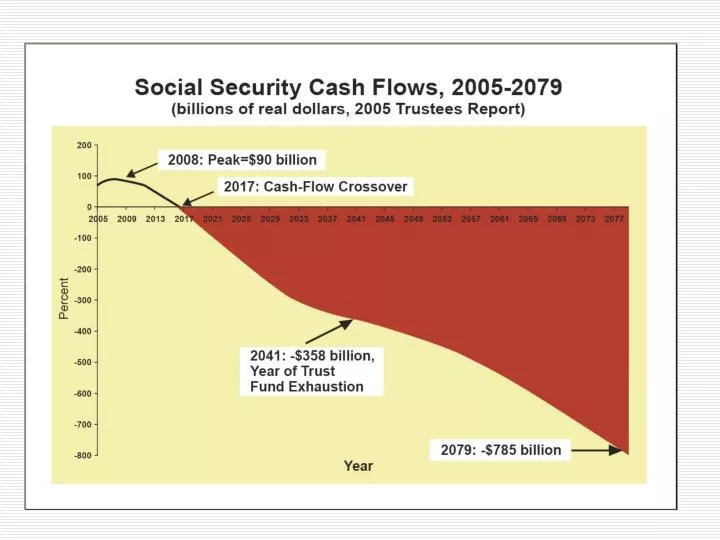

Possibility of Increasing Income to Social Security • The ratio of the number of workers paying FICA taxes to the number of retirees entitled to Social Security benefits is decreasing. • Increases in income to the social security system must come as a result of increased tax revenues.

It is projected that an increase in the payroll tax of 1.9% would solve the social security financing problem for the next 75 years. • It is projected that a 3.5% increase in the payroll tax would solve the social security problem forever! • This is likely to garner opposition by younger workers who have doubts that the system will provide for them into their retirements and are skeptical about having to pay increased taxes, losing money that they could independently invest in privatized markets.

The eventual failure of the social security system could be delayed by increasing the ceiling on earnings that are subject to the payroll tax . The current ceiling is $87,900. This would likely be met by opposition by these earners who would argue the taxes they would be paying would be incommensurate with the benefits they would receive. They would argue that Social Security was established as a social insurance program, not a welfare program. • According to The American Academy of Actuaries, eliminating the wage cap on Social Security taxes and paying benefits on the additional taxed earnings would clear up 77% of the Social Security financing problem.