Download

1 / 26

280 likes | 432 Views

Kuali Chart of Accounts. Claire Tyson, San Joaquin Delta College Bill Overman, Indiana University. Kuali (KFS) Chart. Simple Account Identification Number Transaction Object Code Sub Accounts/Sub Object Codes as Needed Numerous Attributes Linked to the Account Identification Number

E N D

Kuali Chart of Accounts Claire Tyson, San Joaquin Delta College Bill Overman, Indiana University

Kuali (KFS) Chart • Simple Account Identification Number • Transaction Object Code • Sub Accounts/Sub Object Codes as Needed • Numerous Attributes Linked to the Account Identification Number • Multiple Charts if Needed

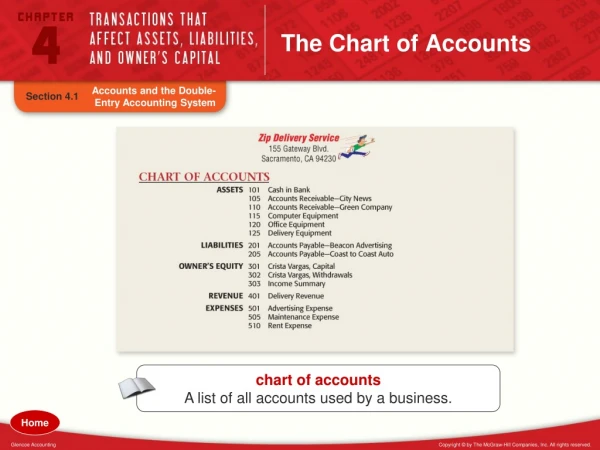

Purpose of a Chart of Accounts • What is the primary purpose of a chart of accounts? • To support and validate entries into a general ledger • Support internal controls • What other functions does the Kuali chart of accounts serve? • Document routing and approvals • Framework for budget construction • Reporting, both internal and external

KFS Chart Features • Chart • Ability to have multiple charts • Charts are hierarchical • Organization • Hierarchical • Facilitates reporting, workflow, controls • Account/Sub-Account • Report up through organizations • Allows for further division of an account for internal reporting purposes

KFS Chart Features • Object code and sub-object codes • Track expenditure types of categories • Allows for further division of an object for internal reporting purposes • Object level codes and object consolidation codes • Provides ability to combine and consolidate by object groups for reporting • Extended attributes

KFS Chart Features • Extended Attributes • Can be used throughout Chart (e.g. Orgs, Accounts, Object Codes, etc.) • What is it? • Additional field to “tag” chart objects with a unique identifier • How to use • Use to “link” chart objects that are not naturally linked for reporting purposes – i.e. tool for pre-existing reporting requirements that don't fit neatly into hierarchical structure • Example • Interdepartmental activities, link unrelated organizational units (cross functional teams, etc.), inter-disciplinary activities

Benefits of Multiple Charts • Ability to handle complex reporting structures • Campus charts are not required to contain object codes unrelated to their activities (i.e. Cost of Goods Sold, Inventory, etc.) • Auxiliary Charts are not required to contain object codes unrelated to their activities (i.e. Tuition, State Appropriations) • Easy access to campus level or Auxiliary reporting • Increased information and knowledge at the campus level

Organizations • Organization • Example: FMOP (Financial Management Operations) • Collection of accounts and/or other organizations • Some organization features: • Chart of Accounts, Campus, Department, Responsibility Center, Subunit • Can include all fund groups • Up to four alphanumeric characters (eg. FMOP) • Extension HRMS table (customizable)

Organization Hierarchy at SU UNIV WA VPBus FM FMSY FMOP

Accounts • Account Number • Specific identifier for a pool of funds assigned to a specific organization for a specific function. • Example: 1912610 (Financial Management Administration) Reports to org FMOP • All accounts can be self-balancing or can post claim on cash offsets to a control account

Org Hierarchy with Accounts UNIV WA VPBus FM FMSY FMOP 1912631 1912610

Sub-Accounts • Sub-accounts achieve further division of an account for internal reporting purposes. • Example: finpr (FM Financial Processing) Reports to 1912610 • Characteristics of a sub-account: • Account specific • Assumes all features of the account it reports to

Org Heir with Accounts/Sub Accounts UNIV WA VPBus FM FMSY FMOP 1912631 1912610 reprt finpr

Object Codes • Object Codes are detailed identifiers for Income, Expense, Asset, Liability and Fund Balances. • Chart specific • Four numeric digits • Example 1: West-2000 “Academic Salaries” East-2000 “Academic Salaries” • Example 2: West-1504 “Animal Care Income” East-1504 “Card Services Income”

Sub-Object Codes • Sub-object codes achieve further division of an object code for internal reporting purposes • Features of a sub-object include the following: • Specific to an account and object code • Assumes all features of the object code it reports to • Example: In State Travel Object Code 6000 • Faculty Instate Travel, Fac • Staff Instate Travel, Sta • Student Instate Travel, Stu

Levels and Consolidations • All object codes report to a higher Level code and each Level code reports to a higher Consolidation code • Approximately 80 Levels (although no limit) • Approximately 20 Consolidations (no limit) • Example: Object Code 4100 “Office Supplies” Level S&E “Supplies and Expense” Consolidation GENX “General Expenses”

Extended Attributes • Extended Attributes are extensions of an Account that enable: • Search by attribute • Lookup by attribute • Balance inquiry retrieval by attribute • Reporting by attribute • Extended Attributes can be alpha / numeric. • They are optional.

Management Control and COA • How can I use the chart for organizational management? • Flexibility in Reporting • Flexibility in making Routing decisions • Hierarchy for Responsibility Management • Facilitates internal controls by assigning fiscal officers, account managers, supervisors • Transparency of data to measure performance of departments and subunits

Management Control and COA • What tools are provided to achieve reporting objectives? • With the Approval of the Chart Manager • Organizations • Accounts • Object codes • Sub-accounts (budgeting / spending) • Sub-object codes (budgeting / spending) • On line balance inquiries and formal reports through use of data warehouse

Creating your own Chart General questions to consider: • Just because it can be changed, should it? • What currently works, what doesn’t? • Implications for historical comparisons • What are the reporting requirements? • Institutional financial reporting (external) • Summarized management reporting • Departmental detail • Ad hoc reporting

Creating your own Chart Chart questions to consider: • Does the institution need multiple charts? • For separate campuses • For auxiliary operations • For high level institutional financial reporting • Will interfaced systems be able to accommodate multiple charts? • Will it add confusion for users?

Creating your own Chart Organization questions to consider: • What should be the basis for the organizational hierarchy? • Lines of authority • Lines of business (disciplines, auxiliaries, etc.) • Financial reporting requirements • How should the org structure relate to other administrative systems (e.g. HR)? • Do orgs need to be grouped in a way other than hierarchical? • How narrowly should org attributes (e.g. type) be defined?

Creating your own Chart Account questions to consider: • Should existing account structure be preserved or should entirely new structure be created? • If new structure is used, can a map from old to new be created? • Should fund/sub-fund attribute perpetuate fund accounting or represent a different way of grouping accounts? • Should accounts be self-balancing, or should the institution use the “flexible claim on cash” option? • How should sub-accounts be used?

CoA Next Steps • Kuali Demo Labs Tuesday 1 pm • Kualitestdrive.org