Download

1 / 20

220 likes | 509 Views

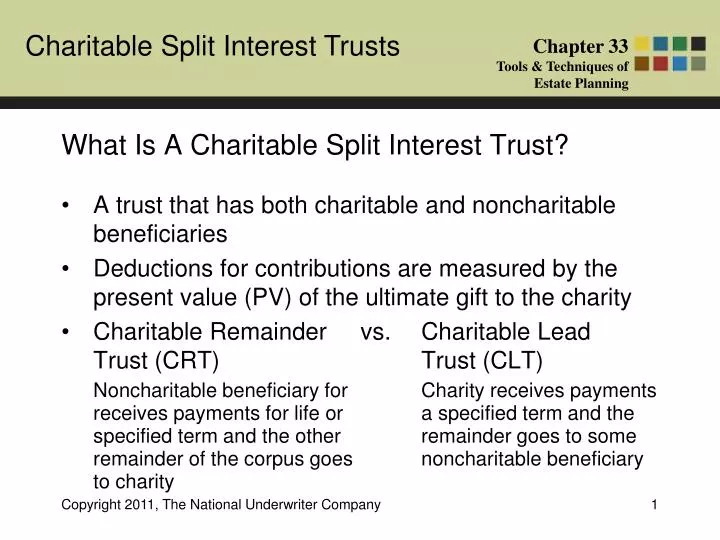

What Is A Charitable Split Interest Trust?. A trust that has both charitable and noncharitable beneficiaries Deductions for contributions are measured by the present value (PV) of the ultimate gift to the charity Charitable Remainder vs. Charitable Lead Trust (CRT) Trust (CLT)

E N D

What Is A Charitable Split Interest Trust? • A trust that has both charitable and noncharitable beneficiaries • Deductions for contributions are measured by the present value (PV) of the ultimate gift to the charity • Charitable Remainder vs. Charitable Lead Trust (CRT) Trust (CLT) Noncharitable beneficiary for Charity receives payments receives payments for life or a specified term and the specified term and the other remainder goes to some remainder of the corpus goes noncharitable beneficiary to charity

1) Gift of Highly Appreciated Property 1) Gift of Property Grantor(s) / Donor(s) Grantor(s) / Donor(s) Charitable Trust (CRT) Charitable Trust (CLT) 2) Payment for life or fixed term Income Tax Deduction Growth of asset out of donor(s) estate 2) Income interest for set term 3) Remainder 3) Remainder Noncharitable Beneficiaries Charity Charity CRT vs. CLT

What Is A Charitable Split Interest Trust? • Gifts of a remainder interest are generally only deductible if made to a fixed annuity trust, unitrust, or pooled income fund • Annuity Trust $ vs. Unitrust %Fixed Dollar Payout Amount Fixed Percentage Payout Amount - CRAT or CLAT - CRUT or CLUT • Pooled Income Fund • Property contributed by a number of donors is commingled with property transferred by other donors and each beneficiary of an income interest will receive income determined by the rate of return earned by the trust for such year

Charitable Pooled Income Fund $2,000,000 earned $100,000 income Donated $1,000,000 Receives $37,500 Income Receives $50,000 Income Donated $750,000 Receives $12,500 Income Donated $250,000 Donor 1 Donor 3 Donor 2 Pooled Income Fund (PIF)

When Is The Use Of A Charitable Split Interest Trust Appropriate? When a donor wishes to provide a present (remainder) or future (lead) economic benefit to himself or other members of his family, or both, along with a present or future interest to charity which qualifies for income, estate, and gift tax charitable deductions

What Are The Requirements of a CRAT? • Pay a fixed amount annually to a noncharitable beneficiary with remainder going to charity • If trust income is insufficient to meet the required annual payment, the difference is paid from capital gains or principal • If income is greater than the required payment amount, the excess is reinvested in the trust • The value of the remainder interest is determined by a combination of • The term of the trust or the beneficiary’s age, • The amount payable to the beneficiary, and • The appropriate monthly IRC Section 7520 rate

What Are The Requirements of a CRAT? • The income tax deduction is computed in the year funds are irrevocably placed in the trust • The deduction is measured by the PV of the charity’s right to receive trust assets upon the death of the annuitant beneficiary or end of the trust term • Tests for a CRAT to qualify for income, estate, and gift tax deductions • A fixed amount determined by a fixed percentage of the initial value of the trust must be payable to the noncharitable beneficiary

What Are The Requirements of a CRAT? • Tests for a CRAT to qualify for income, estate, and gift tax deductions (cont’d) • Annuity percentage must not be less than 5% nor more than 50% of the initial FMV of all property transferred in trust • The specified amount must be paid at least annually to the noncharitable beneficiary out of income and/or principal • Trust must be irrevocable and not subject to a power by either the donor, trustee, or beneficiary to invade, alter, or amend the trust • Trust must be for the benefit of one or more living persons at the time of the transfer in trust, whose interests must consist of a life estate or term of years not exceeding 20

What Are The Requirements of a CRAT? • Tests for a CRAT to qualify for income, estate, and gift tax deductions (cont’d) • Entire remainder of trust must go to charity • Value of the remainder must equal at least 10% of the initial FMV of all assets transferred to the trust

What Are The Requirements of a CRUT? • Tests for a CRUT to qualify for income, estate, and gift tax deductions • A fixed percentage of the net FMV of the principal, revalued annually, must be payable to a noncharitable beneficiary • Percentage payable to noncharitable beneficiary must not be less than 5% nor more than 50% of the annual value • Unitrust may provide that noncharitable beneficiary can receive the lesser of: • The specified fixed percentage, or • Trust income for the year plus any excess trust income to the extent of any deficiency in prior years

What Are The Requirements of a CRUT? • Tests for a CRUT to qualify for income, estate, and gift tax deductions (cont’d) • Trust must be for the benefit of one or more living persons at the time of the transfer in trust, whose interests must consist of a life estate or term of years not exceeding 20 • Entire remainder of trust must go to charity • Value of the remainder must equal at least 10% of the initial FMV of all assets transferred to the trust

What Are The Requirements of a CRUT? • The income tax deduction is computed in the year funds are irrevocably placed in the trust • The deduction is measured by the PV at the date of the gift of the charity’s right to receive trust assets, subject to percentage limitations • The portion of the deduction disallowed may generally be carried forward for five years

What Is A NIMCRUT? • A NIMCRUT is a net income makeup trust where • The beneficiary is limited to the lower of the set percentage or the actual income of the trust • Investments are in assets that produce little to no income in the early years (while the donor’s income is high) and then are converted to high income investments after the donor retires

What Are The Requirements of a Pooled Income Fund (PIF)? • Generally created and maintained by a public charity • Donor contributes an irrevocable, vested remainder interest to the charity that maintains the fund • Property transferred by the donor is commingled with property transferred by other donors • Fund cannot invest in tax-exempt securities

What Are The Requirements of a Pooled Income Fund (PIF)? • No donor or income beneficiary can be a trustee • Donor must retain for himself (or a named beneficiary) a life income interest • Each income beneficiary must be entitled to and receive a pro rata share of income, annually, based on the rate of return earned by the fund

Wealth Replacement Trust • An ILIT which is used in conjunction with a CRT to replace assets that the donor’s heirs will be losing because the remainder will pass to charity at the donor’s death

Wealth Replacement Trust Example • Donor in 48% combined federal and state estate tax bracket • Donor transfers $1,000,000 worth of highly appreciated stock to 6% CRAT • Remainder at death passes to charity of donor’s choice • Donor’s heirs have been disinherited • Heirs would have inherited $1,000,000 - $480,000 (48% tax) = $520,000 had there be no CRAT • The donor establishes an ILIT and the ILIT purchases a policy worth $520,000 on the donor to replace the monies that the heirs would have inherited

Gift $1,000,000 Appreciated Stock 6% CRAT Receives $60,000 Annual Income Donor Receives Income Tax Deduction Gifts Annual Premiums Wealth Replacement Trust ILIT Owns policy worth $520,000 IRS Estate Tax Receives Remainder at Donor’s Death ILIT Proceeds Pass Income and Estate Tax Free to Heirs Charity Donor’s Heirs Wealth Replacement Trust