Download

1 / 8

80 likes | 159 Views

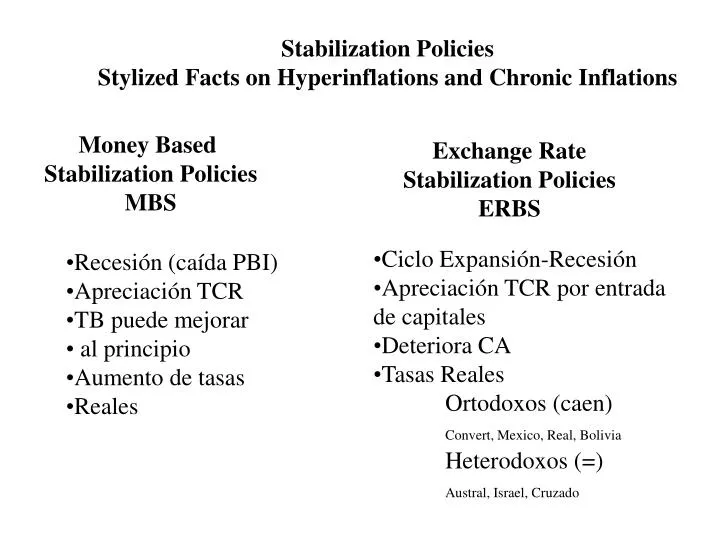

Stabilization Policies Stylized Facts on Hyperinflations and Chronic Inflations. Money Based Stabilization Policies MBS. Exchange Rate Stabilization Policies ERBS. Ciclo Expansión-Recesión Apreciación TCR por entrada de capitales Deteriora CA Tasas Reales

E N D

Stabilization Policies Stylized Facts on Hyperinflations and Chronic Inflations Money Based Stabilization Policies MBS Exchange Rate Stabilization Policies ERBS • Ciclo Expansión-Recesión • Apreciación TCR por entrada de capitales • Deteriora CA • Tasas Reales • Ortodoxos (caen) Convert, Mexico, Real, Bolivia • Heterodoxos (=) Austral, Israel, Cruzado • Recesión (caída PBI) • Apreciación TCR • TB puede mejorar • al principio • Aumento de tasas • Reales

Stopping High Inflation Carlos Vegh 1992 Evidence: Using the exchange rate as the nominal anchor, hyperinflation have been stopped almost over night with relative minor output costs. In contrast, exchange rate based stabilization policies in chronic inflation countries have typically result in a sluggish adjustment of the inflation rate. Both cases sustained real appreciation of the domestic currency, current account deficits and an initial expansion in economic activity followed by a contraction

ERBS The first step assumes that a reduction in the rate of devaluation is fully credible (Policy is permanent). Under this circumstances inflation falls instantaneously without any output costs. Sticky prices don´t prevent the adjustment because price setting behavior is forward looking. This is a way to interpret the end of Hyper. A second exercise assumes that the reduction in the rate of devaluation is not credible (temporary). Public expects the higher rate of devaluation to resume at some point in the future. Temporary fall in interest rate reduce the price of present consumption, current account deficit. The slow convergence of inflation implies a real appreciation which finally reduce the demand of non traded goods and recession is coming. Could be interpreted as a stabilization in Chronic inflation country based on ERBS

Stopping Hyperinflation: Stylized Facts The post World War I Austria Germany Hungary Poland Russia The post World War II Hungary Greece ERBS Fiscal Adjustments Aid from US Taiwan 1945-49 ERBS Fiscal Adjustments Bolivia 1984-1985

Common Facts Inflation is stopped immediately output costs are relative small Stopping Chronic Inflation: Stylized Facts • Latin American heterodox programs of the 1960´ • Argentina-Brazil-Uruguay • Fixed exchange rate • income policies (price and fares control in public utilities and and wages) • all three programs achieved an initial decline in inflation but non sustainable along time.

Southern cone stabilization programs of the late 1970s • Argentina-Chile-Uruguay • Orthodox programs (no price or wage controls) • The exchange rate policy consisted in announcing a devaluation schedule “tablita” with a decreasing rate • The slow convergence of inflation and the corresponding real appreciation of the domestic currency proved fatal.All three programs ended in dramatic fashion with large exchange rate and financial crisis.

Heterodox programs of the mid-1980´s • Argentina-Israel-Brazil-Mexico • price and wage controls, income policies (desagio) • Fixed exchange rate • Inflation converges slowly • There was a sustained real appreciation of the domestic currency • Current account and trade balance deficit • Real activity increases at the beginning of the program and later contracts.

The Model Two goods c is a home good c* is tradable good Identical immortal household Individuals maximize consumption path rate of preference are equal rate of interest e= EP*/P The consumer is required to use money to carry out purchases. The cash in advance constraint is: (c/e+c*)=m The consumer holds an internationally traded bond b Real financial wealth is a= m+b