Download

1 / 9

90 likes | 99 Views

2009 ICN Merger Workshop. Session 1. Merger Notification and Initial Review. Maria Coppola Tineo Taipei, Taiwan March 9, 2009. Recommended Practices for Merger Notification and Review Procedures. The Practices address:

E N D

2009 ICN Merger Workshop Session 1. Merger Notification and Initial Review Maria Coppola Tineo Taipei, Taiwan March 9, 2009

Recommended Practices for Merger Notification and Review Procedures The Practices address: (1) nexus between the merger's effects and the reviewing jurisdiction; (2) clear and objective notification thresholds; (3) timing of merger notification; (4) merger review periods; (5) requirements for initial notification; (6) conduct of merger investigations; (7) procedural fairness; (8) transparency; (9) confidentiality; (10) interagency coordination; (11) remedies; (12) competition agency powers; and (13) review of merger control provisions.

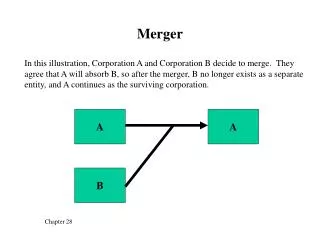

Recommended Practice I Jurisdiction should be asserted only over transactions that have a nexus with the jurisdiction concerned that meets an appropriate standard of materiality, based on activity within that jurisdiction. Example: Company A is buying Company B. Both Company A and B have sales in the reviewing jurisdiction. For threshold calculation, sales of the parent of Company A can be included, but not the sales of the parent of Company B. Company B has material sales in the reviewing jurisdiction. The threshold applies to only the sales of the actual business being acquired (the “target”, here Company B. This does not include the sales of the parent of Company B.) Company A has material sales in the reviewing jurisdiction, Company B does not, and the threshold is triggered by the combined firms’ sales. Company B has a 60% market share in the reviewing jurisdiction.

Recommended Practice II Notification thresholds should be clear and understandable, based on objectively quantifiable criteria (such as sales or assets, rather than market share), and based on information that is readily accessible to the merging parties. Example: Notification is required if the merged parties both either supply or acquire certain goods or services and will, after the merger takes place, supply or acquire 25% or more of those goods and services in the reviewing jurisdiction or in a substantial part of it. There must be an increment to the share of supply. Notification is required if the target company’s sales are more than $50m in the preceding financial year.

What’s the perfect threshold? Factors to consider: • Set clear goals of threshold reform. • Consider different types of thresholds. • Benchmark based on past experience. • Compare thresholds with similarly situated jurisdictions. • Introduce flexibility for future reform.

Recommended Practice III Parties should be permitted to notify proposed mergers upon certification of a good faith intent to consummate the proposed transaction, and suspensive jurisdictions should not have a filing deadline. Example: The concentration shall be notified within one week after the conclusion of the agreement, or the acquisition of a controlling interest. The parties may notify the agency of a draft agreement provided that they declare that their intention is to conclude an agreement that does not significantly differ from the draft notified.

Recommended Practice V Initial notification requirements should be limited to information necessary toinitiate the merger review process. For transactions that do not pose material competitive concerns, notification requirements should avoid unnecessary burdens and consider flexibility in the initial notification (e.g., “short form”). Competition authorities should consider providing an opportunity for pre-notification guidance on the content of notification. Jurisdictions should limit translation requirements (e.g., summaries) and formal authentification burdens for notifications.

Other Resources • Implementation Report http://www.internationalcompetitionnetwork.org/media/archive0611/050505Merger_NP_ImplementationRpt.pdf • Implementation Handbook http://www.internationalcompetitionnetwork.org/media/library/conference_5th_capetown_2006/ImplementationHandbookApril2006.pdf • Defining Merger Transactions for Purposes of Merger Reviewhttp://www.internationalcompetitionnetwork.org/media/library/conference_6th_moscow_2007/23ReportonDefiningMergerTransactionsforPurposesofMergerReview.pdf • Setting Notification Thresholds for Merger Reviewhttp://www.internationalcompetitionnetwork.org/media/library/mergers/Merger_WG_2.pdf • Web Link and Template Projects http://www.internationalcompetitionnetwork.org/index.php/en/publication/293

For further information… N&P Subgroup • mtineo@ftc.gov • clagdameo@ftc.gov Merger Working Group • Paul.E.OBrien@usdoj.gov Advocacy and Implementation Network • icn@jftc.go.jp