Download

1 / 57

610 likes | 960 Views

Consolidated Financial Statements and Accounting for Investments in Subsidiaries. Background Regulatory Framework The Financial Statement prepared for a group of companies is govern by the Companies Act No 17 of 1982 and

E N D

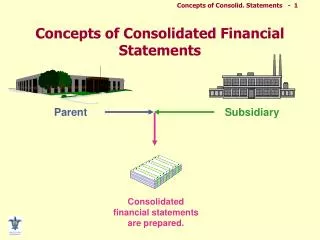

Consolidated Financial Statements and Accounting for Investments in Subsidiaries Background Regulatory Framework The Financial Statement prepared for a group of companies is govern by the Companies Act No 17 of 1982 and Sri Lanka Accounting Standard No 26 “ Consolidated Financial Statements and Accounting for Investment in Subsidiaries” Consolidated financial statements are prepared in accordance with Sri Lanka Accounting Standards.

Control : (for the purpose of this Standard) is the power to govern the financial and operating policies of an enterprise so as to obtain benefits from its activities. A subsidiary :is an enterprise that is controlled by another enterprise (known as the parent). A parent :is an enterprise that has one or more subsidiaries. A group : is a parent and all its subsidiaries. Consolidated financial statementsare the financial statements of a group presented as those of a single enterprise. The minority interest: is that part of the net results of operations and of net assets of a subsidiary attributable to interests which are not owned, directly or indirectly through subsidiaries, by the parent.

Control • Control has been defined as the power to govern the financial and operating policies of an enterprise. Generally these decisions are taken by the board of directors and are appointed by the share holders of the enterprise. There fore the control is presumed to exist in the following circumstances • when the parent owns, directly or indirectly through subsidiaries, more than one half of the voting power of an enterprise

Control also exists even when the parent owns one half or less of the voting power of an enterprise when there is • When it has power over more than one half of the voting rights by virtue of an agreement with other investors • Power to govern the financial and operating policies of the enterprise under a statute or an agreement • Power to appoint or remove the majority of the members of the board of directors or equivalent governing body • power to cast the majority of votes at meetings of the board of directors or equivalent governing body

Why Consolidated Financial Statement The capital contributed by the shareholders of the parent company are normally invested in the subsidiary . Therefore such shareholders of the parent company would like to know not only the results and net assets of the parent company but also the aspects of the subsidiary. They would more prefer to know in respect of funds they have contributed the total return rather the return only on the parent company. A parent company should present consolidated financial statements to its share holders. A parent which issues consolidated financial statements should consolidate all subsidiaries( Foreign and domestic)

A subsidiary should be excluded from consolidation when • Control is intended to be temporary because the subsidiary is acquired and held exclusively with a view to its subsequent disposal in the near future • It operates under severe long-term restrictions which significantly impair its ability to transfer funds to the parent

A parent that is wholly owned subsidiary of another parent company need not to present consolidated financial statements provided the latter parent present consolidated financial statements. A Owns 100% B Owns 60% C Thought B is a parent, B need not to prepare the consolidated financial Statements as it is wholly owned subsidiary of A

Consolidation Procedures • Consolidated Balance Sheet • In preparing consolidated balance sheet, the balance sheets of parent and the subsidiaries are combined on a line-by-line basis by adding together like items of assets, liabilities, equity. • In order that the consolidated financial statements present financial information about the group as that of a single enterprise, the following steps are then taken: • The carrying amount of the parent's investment in each subsidiary and the parent's portion of equity of each subsidiary are eliminated • Inter company trading should be eliminated.

Balance sheet of the parent company and the subsidiary as at 31st March 2006 are as follows. Parent Company Balance Sheet Assets Parent Subsidiary Non Current Assets Property, Plant & Equipments 1,500,000 550,000 50,000 Rs 10 each shares in Subsidiary at cost 5,00,000 2,000,000 Current Assets Stock 160,000 130,000 Debtors in Subsidiary 50,000 Other Trade Receivable 110,000 160,000 70,000 Cash at Bank 100,00060,000 520,000 260,000 Current Liabilities Creditors in Parent (50,000) Creditors (120,000) 400,000 (60,000) 150,0002,400,000700,000 Capital & Reserves 200,000 Rs 10 each Ordinary shares 2,000,000 50,000 of Rs 10 each ordinary shares 500,000 Reserves 400,000200,000 7,900,000700,000

Some item may appear in the balance sheet of the parent company and its subsidiary but not at the same amount • The parent company may acquire the subsidiary at a consideration greater or lesser than their nominal value. The assets will appear in the parent company balance sheet at cost, while liability will appear in the subsidiary balance sheet at nominal value. This difference raises the issue of Good Will. • Some time parent company may not acquire all the shares of the subsidiary. This raises the issue of Minority interest. • The inter company balances may out of step because of the goods or cash in transits. • Parent company may have acquired proportion of the loan stock of the subsidiary balance sheet.

The balance sheet of H ltd and its subsidiary S ltd as at 31st March 2006 are given below. H Ltd has acquired the all the ordinary shares and 60% of the loan stock of its subsidiary. The different of the current account arises because of goods in transits. Prepare the consolidated balance sheet of H Ltd.

Minority Interest The minority interest is that part of the net results of operations and of net assets of a subsidiary attributable to interests which are not owned, directly or indirectly through subsidiaries, by the parent. So a proportion of the net assets of such subsidiaries in fact belongs to investors from outside the group. In the consolidated balance sheet it is necessary to distinguish this proportion from those assets attributable to the group and financed by share holders fund. The consolidated procedure for dealing with partly owned subsidiaries is to calculate the proportion of ordinary shares, preference shares and reserves attributable to minority interests.

Balance sheet of the H Ltd and its subsidiary S Ltd are given below as at 31st March 2006.

Adjustment for the dividend When the subsidiary company pays a dividend during the accounting period, no adjustment is required when consolidation. But adjustment is required when the subsidiary company proposed dividend but not yet paid. In this case the first step is to ensure that accounts of both subsidiary and parent company are reflecting the proposed dividend. If they have not accrued first the proposed dividend should be accrued in both companies’ accounts. Then on consolidation, The dividend payable in subsidiary’s accounts will cancel with the dividend receivable in the parent’s accounts. If the subsidiary is a wholly owned one, there will be complete cancellation, If it is only partly owned there will be only part cancellation. The un cancelled portion will be the amount belongs to minority share holders and this will appear in the consolidated balance sheet as a current liability.

Balance sheets of the H Ltd and its subsidiary S Ltd are given below as at 31st March 2006.

Additional information • Neither company has yet provided for any dividend, you are required to provide for • - The preference dividend of S Ltd • - A proposed ordinary dividend of 10% By S Ltd • A proposed ordinary dividend of 15% By H Ltd • You are required to prepare the consolidation balance sheet

Good Will Arising On Consolidation The amount paid over and above the value of the tangible assets acquired of a subsidiary is called good will arising on consolidation. Any excess of the cost of the acquisition over the acquirer's interest in the fair value of the identifiable assets and liabilities acquired as at the date of the exchange transaction should be described as goodwill and recognised as an asset. Goodwill acquired in a business combination represents a payment made by the acquirer in anticipation of future economic benefits from assets that are not capable of being individually identified and separately recognised. Goodwill acquired in a business combination shall not be mortised. Instead, the acquirer shall test it for impairment annually or more frequently if events or changes in circumstances indicate that it might be impaired. in accordance with SLAS 41, Impairment of Assets.

Negative Good Will • If the acquirer's interest in the net fair value of the identifiable assets, liabilities and contingent liabilities recognised exceeds the cost of the business combination, the acquirer shall: • Reassess the identification and measurement of the acquiree's identifiable assets, liabilities and contingent liabilities and the measurement of the cost of the combination; and • (b) Recognise immediately in profit or loss any excess remaining after that reassessment.

Reserves The net asset or the share holder’s interest of a subsidiary consists of ordinary share capital and the reserves. At the point of acquisition of a company (Subsidiary), it is very important to make a distinction between pre acquisition reserves and Post acquisition reserves. Pre acquisition reserves are those reserves of the subsidiary exist at the date of acquisition by the parent Post Acquisition Reserves are those reserves of the subsidiary which arose after the acquisition.

When consolidating the financial statements of the parent and subsidiaries, pre acquisition reserves of subsidiary companies are not aggregated with the parent company’s reserves instead they charged to the cost of control account. But the post acquisition reserves of the subsidiaries aggregated with the parent company’s reserves when consolidating the financial statements.

H Ltd acquired the ordinary ordinary shares of the S Ltd on 31st March 2006 when draft balance sheet of each company as follows H Ltd acquired its investment in S Ltd on 01/04/2004 when the revenue reserves of S Ltd stood at Rs 10,000. There has been no change in the share capital and capital reserves of S Ltd since that date. At 31st March 2006 S Ltd had invoiced H Ltd for goods to the value of Rs 2,000 which had not been received by H Ltd.

Inter Company Trading We have come across where one company in a group in trading with another group company. Any debtor, creditor balances outstanding between companies are cancelled on consolidation. So there will not be any problem if all such inter group transactions are undertaken at cost. However each company in a group is a separate entity and may wish to teat other group companies in the same way as any other customer. In this case, a company (A Ltd) buy goods at one price and sell them at a higher price to another group company( B Ltd). The accounts of A ltd will quite properly include profit earned on sales to B. Similarly B Ltd balance sheet will include stock at their cost to B Ltd at the amount at which they were purchased from A.

H Ltd acquire all the shares in S Ltd when the reserves of S Ltd stood at Rs 15,000 Draft balance sheet for each company are as follows.

During the year S Ltd sold goods to H Ltd Rs 75,000 The profit from to S Ltd being 20% of selling price at the balance sheet date Rs 22,500 of these goods remain unsold in the stocks of H Ltd. At the same time H Ltd owed S Ltd Rs 18,000 for goods bought and this debt is included in the creditors of H Ltd and the debtors of S Ltd.

Acquisition of a subsidiary during its Accounting Period When a holding company acquires a subsidiary during its accounting period the only accounting entry will be those recording the cost of the acquisition in the holding company’s books at the and of the accounting year it will be necessary to prepare consolidated Financial Statements. The subsidiary company accounts to be consolidated will show the subsidiary profit or loss for the whole year. For consolidation, profit need to distinguish between profit earn before the acquisition and profit earned after the acquisition.

H Ltd acquires 80% of the ordinary shares of S Ltd on 31st December 2005. On 31st March 2005 S Ltd accounts showed a share premium account of Rs 6,000 and revenue reserves of Rs 22,500. The balance sheet of two companies as at 31st March 2006 are set out below. Neither company has paid or propose any dividend during the year. You are required to prepare the consolidated balance sheet of H Ltd as at 31st March 2006.

Dividend out of requisition profits The holding company as a member of the subsidiary company is entitled to its share of dividends. When a subsidiary company pays out a dividend soon after the question it is important to decide, those dividends are paid out of pre acquisition profit or post acquisition profits. If the dividends comes from pre acquisition profit there is no problem, the holding company simply credit the relevant amount to its profit & loss account as with any other dividend income. However if the dividend is paid from pre acquisition profits, the double entry is as follows Cash Account Dr Investment in Subsidiary Account Cr

Then the holding company’s balance sheet disclose the investment as in subsidiary at cost less amount written down (Group proportion of the dividend paid out of pre acquisition profit by the subsidiary) We need next to consider how it is decided whether a dividend is paid from pre acquisition profits. If the holding company acquires shares in subsidiary at the beginning of the accounting period and the dividend was in respect of the previous accounting period clearly the dividend was paid from profit earned in the period before acquisition. If the shares are acquired during the accounting period of the subsidiary the example will illustrate the fact that the dividend is paid out of the pre acquisition profit or not.

Example. H ltd acquired 16,000 of the 20,000 ordinary shares of S Ltd on 1st April 2005 for Rs 500,000. S ltd balance sheet as at 31st March 2005 showed a proposed ordinary dividend of Rs 80,000 and retained reserves of Rs 240,000. The balance sheet of the two companies at 31st March 2006 are given below.

Revaluation of a subsidiary company’s assets on acquisition SLAS 25 Defined the Goodwill as the difference between the purchase consideration paid by the holding company and the fair value of the assets acquired from the subsidiary. The balance sheet of the subsidiary company at the date of its acquisition may not guiding to the fair value of its assets. Until now we have calculated the goodwill as the difference between the cost of the investment and the book value of the net assets acquired by the group. If this calculation is to comply with the definition in SLAS 25, we must ensure the book value of the subsidiary’s net assets is the same as their fair value.

There are two possible ways of achieving this • The subsidiary company might incorporate any necessary revaluation in its own books of accounts. • The revaluation may made as a consolidation adjustment without being in corporate in the subsidiary’s books. In this case we must make the necessary adjustments to the subsidiary company’s balance sheet as a working . • It is very important to note that when depreciable assets are devalued there may be a corresponding alteration in the amount of depreciation charged during year and accumulated depreciation.

Example H Ltd acquired 75% of the subsidiary shares of S Ltd on 1st April 2005, at the date fair value of S Ltd’s Property, Plant & Equipment was Rs 460,000 greater than their net book value, and the balance of retained profits was Rs 420,000. This balance sheet of both companies as at 31st March 2006 are given below. S Ltd has not incorporated any revaluation in this books of account. H Ltd has devalued its Property. Plant & Equipment on 1st April 2005, addition of Rs 60,000 would have been needed depreciation charged in the profit & Loss account for 2005/06 Prepare the H Ltd consolidated balance sheet as at 31st March 2006

Piecemeal Acquisitions A holding company may acquire a controlling interest in the share of subsidiary as a result of successive share purchases, rather than by purchasing the all shares on the same day. For the purpose of consolidation, it is necessary to decide what reserves of the subsidiary are pre acquisition profits, but since the acquisition has occurred in several stage, it is not immediately clear how to decide what they are.

If a controlling interest is achieved by means of a build up of share acquisition over a period of time. So that the present reserves include elements which are pre acquisition as regards some block of shares hold but post acquisition as regards other blocks shares the problem faced in deciding how much of the present reserves belongs to the good will calculation is really one of interpretation. The general rule is that the pre and the post acquisition reserves and profits should be established at each purchase of shares if it can be assumed that each purchase is substantial and there is an objective of gaining ultimate control when these assumptions are present the pre and post acquisition profit should only be established when control has been gained.

Ignore share purchases which keep the buying company shares of equity below 20% make no step by step method calculations before the bought company becomes an associated company. This is on the rough and ready assumptions that on insertions as to obtain control does not exits until associated company status in reached for the partly bought company. When the purchase of shares first take a company’s holding above 20% (up to 50%) treat all the share purchases up to this date as a single block of purchase for the purpose of calculating pre acquisition profits. For future purchases up to the time when control is eventually acquired, the step by step method should be applied.

H Ltd acquires shares in S Ltd , which has issued ad fully paid share capital of 200,000 Rs 10 ordinary shares, on these separate dates. You are required to calculate the pre acquisition profits of the H group in S Ltd eventually become a subsidiary on 31 /12/ 2005

Reserves as at 31st March 2006 is Rs 1,500,000 Share capital 200,000 of Rs 10 each. Prepare Cost of Control Account, Minority Interest and Consolidated reserve Account as at 31st March 2006.

Consolidated Profit & Loss Account When leaning consolidated profit and loss account it is very important to consider the aspects of Inter company trading, Inter company dividends, pre acquisition profit and Disclosure requirements.

H Ltd acquire 75% of the subsidiary S Ltd on the company incorporation in 2004. The summarised Profit & Loss Account of the companies for the year ending 31st March 2006 are set out below.

Inter company Dividend S Ltd Capital consist of 20,000 6% Rs 10 Preference shares and 20,000 Rs 10 ordinary shares on 1st April 2002, the date of S Ltd Incorporated, H Ltd Acquired 6,000 of the preference shares and 15,000 of the ordinary shares in S Ltd. The profit & Loss Account of these two companies for the year ended 31st March 2006 are set out below.

Pre Acquisition Profits • The figure for retained profits at the bottom of the consolidated profit and loss account must be the same as the figure for retained profits in the consolidated balance sheet. • The retained profit of the consolidated balance sheet comprises • The whole of the holding company’s retained profit and • A proportion of the subsidiary company’s retained profit. That is the group share of post acquisition retained profit in the subsidiary from the total retained profit of the subsidiary.

We must there fore exclude both the minority share of the total retained profits and the group share of pre acquisition retained profits. A similar procedure is necessary in the consolidated profit and loss account. There fore the figure for profits brought forward should only include the group share of the post acquisition retained profit.

If the subsidiary is acquired during the accounting period it is there fore necessary to apportion its profit for the year between pre acquisition and post acquisition element. There are two approaches which may be used for this in the consolidated Profit and loss Account. • The whole year method • Part year method

With the whole year method, the whole of the subsidiary’s turnover cost of sales so on are included in the consolidated P & L. A deduction is then made lower down the schedule to exclude the profit accruing prior acquisition. With the part year method entire P & L Account of the subsidiary split between pre and post acquisition proportion. Only the post acquisition proportion is included in the consolidated P & L.

H Ltd acquire 60% of the equity of S Ltd on 1st July 2005. The profit and loss account of the two companies for the year ended 31st March 2006 are set out below. Prepare the consolidated profit & Loss account using two methods

Summarised profit and loss account for the year needed 31st March 2006 of H Ltd and its subsidiary S Ltd are set out below.

Additional Information • H Ltd acquired 80% ordinary shares of S Ltd on 1st April 2005. • Balance of the profit and loss account of S Ltd as at • 01.04.2005 was Rs 50,000 • S Ltd has not utilised pre acquisition profit to propose the dividends • H Ltd has not accounted dividend proposed by S Ltd on accrual basis. • You are required to prepare the consolidated Profit and Loss account as at 31st March 2006.