Download

1 / 15

150 likes | 156 Views

Explore the centralized system of public budgets, including the state budget and extrabudgetary state funds, in the Czech Republic. Learn about the budget process, key actors, and the use of funds.

E N D

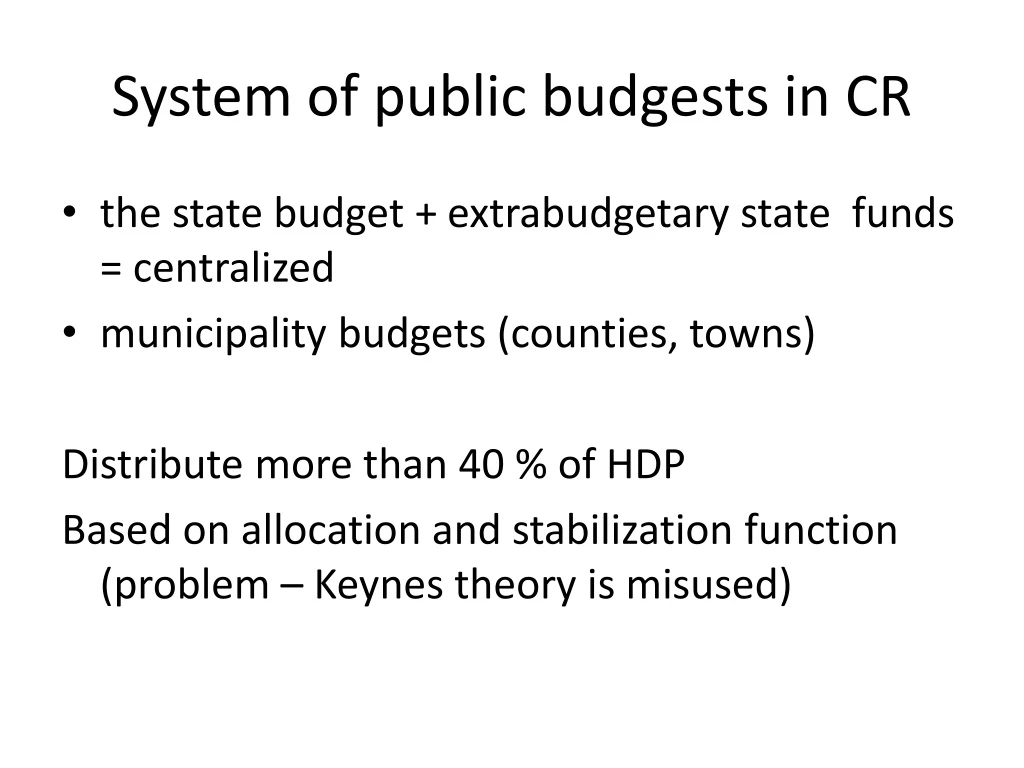

Systemof public budgests in CR • the state budget + extrabudgetary state funds = centralized • municipality budgets (counties, towns) Distribute more than 40 % of HDP Based on allocation and stabilization function (problem – Keynes theory is misused)

The Budget system-Legal Framework The budget processofthecentralgovernment (thestate budget and extra-budgetarystatefunds) is set by theAct on BudgetaryRules in addition to thespecialacts on extra-budgetarystatefunds. Extra-budgetarystatefunds (onlyexamples, together 16 bodies) • StateAgriculturalInterventionFund, • StateCulturalFund, • StateFundforthe Support andDevelopmentoftheCzechCinematography, • StateFundof Transport Infrastructure, • StateEnvironmentalFund, • StateFundforHousingDevelopment, • EstateFundoftheCzechRepublic • Pension andHealthfund, Czech Export bank…

The budgetary process • is a complex of decisions taken by various subjects, which results in resource allocationin the public sector. • As the public budgets in the Czech Republic distribute about 44% of the GDP it is worthstudying who, how and when makes the decisions crucial for the final use of the public money.

Politicalcontext • The Czech Constitution establishes a parliamentaryRepublic. The President (profVaclav Klaus)is Head of State with largelysymbolic powers and WASelected by the Parliament (nexttime – by inhabitants). • The Czech Parliament is composed of • the Chamber ofDeputies (200 seats, proportional, 4years) and • the Senate (81, majority, 6 years).

The budgetary process is composed of two mutually connected cycles: • the multi-annual planning (n+1,2) and • the annualbudgeting (is based on the approved multi-annual expenditure framework). • The Chamber ofDeputies approves in December (t-1) the state budget for the year (t) (if not, thestate budget lawfor t-1 isusedfor t)and the multi-annual expenditureframework for the years (t+1) and (t+2). • The multi-annual expenditure framework contains the total expendituresof the state budget and the extra budgetary funds for the years (t+1) and (t+2).

Process… • Ministry of finance preparesthe agenda forgovernment (January/February (t)) • In April (t) the governmentdiscusses the budget policy for the year (t+1) and sets the limit for the total expenditures, which is equal to theamount approved in the multi-annual expenditure framework after some allowed modifications. • At the same timethe government discusses the multi-annual outlook (framework, but in more detail, + revenues), which is the multi-annual expenditure frameworkelaboratedfor each spending ministry and each extra budgetary fund for the years (t+1) and (t+2). The multi-annual outlookis in contrary to the multi-annual expenditure framework not approved by the Chamber of Deputies and istherefore not binding.

Budgetary process in the Czech Republic is a traditional budgetary process, as characterized by Wildavsky(1997). • It is incremental, line item budgeting which focuses only on inputs. The government declared (8 years ago sic!, 2004) in itspublic budgets reform the will to introduce performance oriented budgeting.

TheSchedule oftheBudget Process – more aboutframeworks • Thescheduleofthe budget processstarts in Februaryandfinishesattheendoftheyearandisobligatoryaccording to theAct on BudgetaryRules. • Thestate budget actand medium-term expenditureframeworksforyears n, n+1,n+2as well as thelimitsofexpendituresandrevenuesforthechapters` (e.g.lineministries ) budgets areapprovedannually. • Thedraft state budget, medium- term expenditureframeworksandlimitsofexpendituresandrevenues (outlook)forthechapters`budgets are drawnup by the Ministry of Finance followed by theapprovalofthegovernmentandthe House ofDeputies.

Medium-term expenditure frameworks • The medium-term expenditure frameworks for years n, n+1, n+2 were included into the Act on Budgetary Rules in connection with the decreasing of the general government deficit and fulfilment of the commitments towards the EU. • The medium-term (only) expenditure frameworks involve state budget expenditures,extra-budgetary state funds. • Public sector revenue forecasts are not reliable for n+2

The Budget Process The budget process has fourmainphases: • Formulationofthe draft statebudget (for n+1) and medium- term expenditureframeworksforyearsn+1, n+2 by the Ministry of Finance • Government`s approval • Parliamentaryscrutiny • Implementation

Two Fiscal Statistical Systems There are twofiscalstatisticalsystems monitoring thegeneralgovernment/ public budgetsfromthedifferentpointsofview: • TheEuropeanSystemofNationalandRegionalAccounts ESA 95(accrual-based) • GovernmentFinance Statistic(GFS - NationalMethodology –FiscalTargeting) (cash-based)

Comparison I • The (GFS)FiscalTargetingincludes just so-calledpublic budgetsinvolvingthecentral, regionalandmunicipalgovernmentsas well asregionalcouncilsofcohesionregions (not funds…). • TheESA 95coverstheentireGovernmentsector, in otherwords, public healthinsurancecompanies,governmentagencies, subsidiaries, funds, stateuniversitiesandother set allowanceorganizations.

Comparison II • In accrual system (ESA 95), recognition occurs with the exchange of liabilities and /or assets, which is usually before the cash flow and closer to actual economic impact of the transaction. • In contrast, the cash basis (Fiscal Targeting ), which is used in most traditional budget systems, records outlays and receipts only when they involve cash transactions.