Download

1 / 18

210 likes | 661 Views

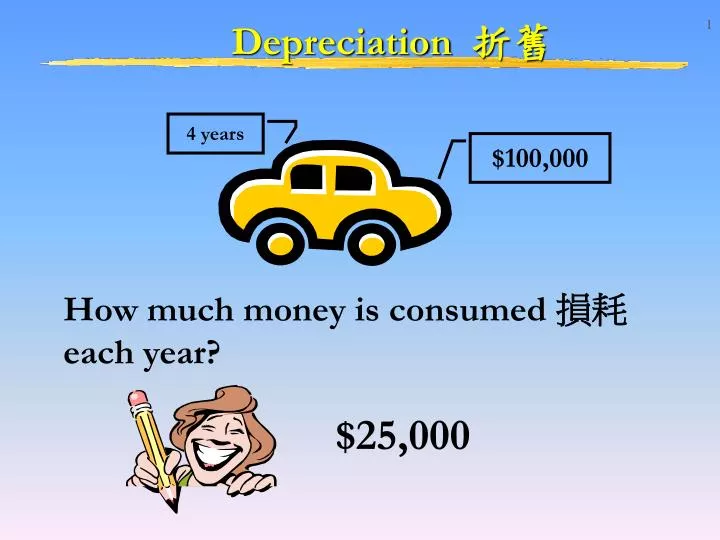

4 years. $100,000. Depreciation 折舊. How much money is consumed 損耗 each year?. $25,000. Depreciation. Definition. Depreciation is the part of the original cost of the fixed asset consumed during its period of use by the firm. .

E N D

4 years $100,000 Depreciation 折舊 How much money is consumed 損耗 each year? $25,000

Depreciation Definition Depreciation is the part of the original cost of the fixed asset consumed during its period of use by the firm. It is an expense for services consumed in the same way as expenses for items such as wages, rent and electricity. Since depreciation is an expense, it will be charged to the profit and loss account.

Depreciation Main causes of depreciation: • Wear and tear (i.e. loss of value arising from use) • Rust, rot and decay • Obsolescence (i.e. new technology) • Inadequacy • Time factor (i.e. lease on premises or a patent) • Depletion (i.e. extraction of raw materials)

Methods of depreciation There are a number of methods by which the actual amount of depreciation for a given period can be calculated: 1. Straight line method Using this method, the same amount of depreciation is deducted each year. 2. Reducing balance method The depreciation charge is calculated by applying a fixed percentage to the net book value of the fixed asset. That means the depreciation charge is less and less each year.

Methods of depreciation 3. Revaluation method This method is used for calculating depreciation of small value fixed assets such as crates, barrels or small tools.

$’s Depreciation charge Straight-line method

Cost less Disposal Value* Number of years of estimated useful life Straight-line method Formula 1 : • Disposal Value • Residual value • Scrap value • Salvage value

COST $10,000 5 years SCRAP VALUE $2,000 $10,000-$2,000 5 Straight-line method of depreciation Annual Depreciation = $1,600

e.g.2 (1) – (12) Answers and e.g.4 (1) – (10) Answers

COST $40,000 Rate=20% Straight-line method Formula 2 : Cost x a fixed % Annual Depreciation = $40,000 x 20% = $8,000

$’s Depreciation charge Depreciation charge Repairs and maintenance Reducing balance method

Reducing balance method Formula: 1st year Costxa fixed % Following years Net Book Valuexa fixed % Net Book Value 賬面淨值 = Cost less Accumulated Depreciation

Year 1 $ Cost price 8,000 Less Depreciation ($8,000 x 20%) 1,600 Net book value Year 1 = 6,400 Year 2 Less Depreciation ($6,400 x 20%) 1,280 Net book value Year 2 = 5,120 Year 3 Less Depreciation ($5,120 x 20%) 1,024 Net book value Year 3 = 4,096 Reducing balance method e.g.An equipment costs $8,000 and it was agreed to depreciate the machine at 20% per annum using the Reducing Balance Method. and so on… Note: You can never completely write off an asset using this method.

Revaluation method Formula : Value of Fixed Assets at start add Purchases of Fixed Assets during the year less Value of Fixed Assets at end

At Start $3,000 At End $2,300 Revaluation method

Revaluation method Use of Loose Tools (Depreciation) = $3,000 - $2,300 = $700

At Start $5,000 Purchases $1,000 At End $4,800 Revaluation method

Revaluation method Use of Loose Tools (Depreciation) = $5,000 + $1,000 - $4,800 = $1,200