Download

1 / 0

0 likes | 119 Views

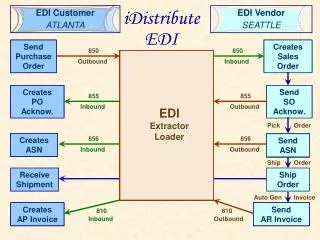

Auditing Electronic Data Interchange. Electronic Data Interchange. It is the intercompany exchange of computer processible business information in standard format.

E N D