Download

1 / 29

290 likes | 473 Views

Net Present Value Made Easy. The ability to perform net present value calculations is a great skill to have. The applications are limitless and net present value is very flexible. Research indicates that it

E N D

Net Present Value Made Easy The ability to perform net present value calculations is a great skill to have. The applications are limitless and net present value is very flexible. Research indicates that it is one of the best financial decision tools available. Fortunately, once you see how it works it is a very simple tool to use. Use your “Arrow Keys” to navigate the slides.

Net Present Value Made Easy Two Keys to Success There are two keys to success when doing net present value: cash flows and interest rate When doing NPV problems, the two keys to success are guesses (estimates). They are important guesses because they affect the outcome of the NPV analysis and your decision.

Net Present Value Made Easy Cash Flows Usually, a business project or business investment will have cash flows. That is, sometimes an entity doing a project will be spending money and sometimes the business entity will be receiving money. Money going out of the entity is called a negative cash flow and money received by the entity is called a positive cash flow. The focus of a NPV analysis is cash flows. A primary job of a person doing a NPV analysis is determining the amount and the timing of cash flows. As mentioned before, cash flows are usually an estimate.

Net Present Value Made Easy Interest Rate In order to do a NPV analysis, you need to have an interest rate. Interest rates vary depending on what you want to do. Credit cards offer various interest rates, and mortgages, savings accounts, etc will offer even different interest rates. In addition, interest rates change frequently. As with cash flows, the interest rate used in a NPV analysis is a guess. Although just an estimate, the interest rate used in the analysis will have a huge impact on the outcome of the analysis and therefore the business decision. So what interest rate should be used?

Net Present Value Made Easy What Interest Rate Should be Used? Since the interest rate used in a NPV analysis is a guess, there are many different ways to choose an interest rate. The interest rate should be chosen carefully because the interest rate will affect the decision in a very big way. In fact, unprofitable projects can be made to look profitable, simply by the the interest rate used in the analysis. Of course, the opposite can occur also. Here is one common way to choose an interest rate: Usually a business will have a rate of return on investments and projects that the organization strives to achieve. That rate might be 15%, 20%, 25%, etc. It depends on the business and the policy of the management. Start with the desired rate of return and add a percentage point or two if the project is not too risky. If the project is very risky, add several percentage points to the desired rate of return.

Net Present Value Made Easy The Timing of Cash Flows As said before, the amounts and timing of cash flows need to be estimated. Since NPV is a method of analyzing future alternatives, and the future is usually quite uncertain, there is a limit as to how precise the timing of cash flows can be determined. For example, a person could try to forecast future cash flows to the day and hour, but that would be too impractical and the person would probably be wrong anyway. Most people believe the trade-off between accuracy and practicality is a year. That is, when people do NPV, they only attempt to estimate cash flows to the nearest year. For example, any cash flows taking place in a given year are assumed to take place on the last day of that given year. A very rough estimate, but it works in most cases and it simplifies the NPV analysis.

Net Present Value Made Easy Recognizing Some Cash Flow Patterns There are only two types of cash flow patterns used in NPV analysis. Lump Sum and Annuity A lump sum is just what the name implies. A lump sum of money, received or paid, on a certain date. For example: a person receives (or pays out) $1,000,000 at the end of year 2018. An annuity is a series of equal payments over equal periods of time. For example: a person receives (or pays out) $10,000 at the end of each year for the next 20 years.

Net Present Value Made Easy Solving NPV Problems The key to solving NPV problems is the time line. A time line looks as follows: 1 2 3 4 5 6 7 The numbers indicate the years (sometimes called periods). Always draw a time line when doing complex NPV problems.

Net Present Value Made Easy Entering the Cash Flows You place the estimated cash flows onto the time line in order to gain a clear understanding of the cash flow patterns. The following is an example: 1 2 3 4 5 6 7 $1,000 The cash flow shown represents a positive cash flow (cash received) of $1,000 at the end of year 4. It also represents a lump sum as opposed to an annuity.

Net Present Value Made Easy Entering the Cash Flows Here is another example: 1 2 3 4 5 6 7 - $1,000 - $1,000 - $1,000 - $1,000 - $1,000 The cash flow shown represents a negative cash flow (cash paid out) of $1,000 at the end of each year, years 1 – 5. This is a good example of an annuity.

Net Present Value Made Easy Everything Needed to Solve the NPV Problem The last thing to enter is the interest rate being used in the analysis. This problem is going to use 15% 15% 1 2 3 4 5 6 7 - $1,000 - $1,000 - $1,000 - $1,000 - $1,000 I usually place the interest rate used in a prominent place above the time line.

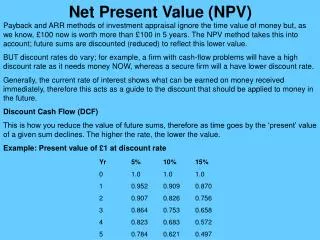

Net Present Value Made Easy Everything Needed to Solve the NPV Problem (really) Last slide I said that we had everything we needed to solve the problem. I forgot one important thing: either a calculator that can do cash flows or present value tables. 15% 1 2 3 4 5 6 7 - $1,000 - $1,000 - $1,000 - $1,000 - $1,000 Since every calculator is different to operate, I will solve all of the problems using the present value tables. You can find present value tables in the back of any accounting or finance book.

Net Present Value Made Easy Problem #1: Solving an Annuity Problem By looking at the time line below, it is easy to see that the cash flows represent an annuity (equal payments & equal periods of time). You need to look at the “Present Value of an Annuity Table” to get the “factor.” 15% 1 2 3 4 5 6 7 - $1,000 - $1,000 - $1,000 - $1,000 - $1,000 Looking at the Present Value of an Annuity Table you see Interest Rates along the top of the table and “Periods” down the left side of the table. In problem #1, the interest rate is 15% and the number of periods is 5. The payments happen each and every year, starting at the end of year 1 and terminating at the end of year 5. The appropriate factor from the table should be 3.35216 or something close to it.

Net Present Value Made Easy Problem #1: Solving an Annuity Problem On the last slide we found the factor to be 3.35216 15% 1 2 3 4 5 6 7 - $1,000 - $1,000 - $1,000 - $1,000 - $1,000 PV = -$3,252.20 All you do to find the answer is multiply the factor times one of the payments. Present Value = 3.25216 x -$1,000 Present Value = -$3,252.20 (negative number) That is all you do to find the PV of an annuity.

Net Present Value Made Easy Problem #2: Solving a Lump Sum Problem Here is a lump sum problem. Lump sum problems are pretty easy. Again, you need to look up a factor. Be sure to look up the factor on a “Present Value of a Lump Sum” table. Sometimes those tables are called “Present Value of $1.” 15% 1 2 3 4 5 6 7 $5,000 PV = $3,287.60 Hopefully the factor you found is .65752 Here is all you do to find the present value: Present Value = .65752 x $5,000 Present Value = $3,287.60 (positive cash flow)

Net Present Value Made Easy Problem #3: Mixing An Annuity and a Lump Sum Check out the following cash flows. If you look carefully, you will see that there is an annuity for years 1-6 and a lump sum at the end of the 7th year. The interest rate has been changed to 12%. 12% 1 2 3 4 5 6 7 $3,000 $3,000 $3,000 $3,000 $3,000 $3,000 10,000 PV = $12,786.58 Solution: Find the present value of the annuity (12% & 6 periods) Present Value = 4.11141 x $3,000 = $12,334.23 Next: find the present value of the lump sum ($12% & 7th period) Present Value = .45235 x $10,000 = $452.35 Finally: simply add the two present values together for the final answer. $12,334.23 + $452.35 = $12,786.58

Net Present Value Made Easy Problem #4: A “Late Bloomer” Annuity Although it looks different, this problem is similar to the problem we just did. Below we have an annuity (equal payments & equal periods of time), but the annuity begins at the end of year 3 and extends to the end of year 7. If you count the number of payments, you would see that there are 5 payments of $5,000 each. The first step is to find the present value of the annuity. 12% 1 2 3 4 5 6 7 $5,000 $5,000 $5,000 $5,000$5,000 $18,023.90 Solution: Find the present value of the annuity (12% & 5 periods, not 7 periods) Present Value = 3.60478 x $5,000 = $18,023.90 We are left with a lump sum of $18,023.90. Notice that it is placed at the end of year 2. Now, just find the present value of a lump sum $18,023.90, 12%, period 2 1 2 3 4 5 6 7 $18,023.90 The present value and final answer = .79719 x $18,023.90 = $14,368.47

Net Present Value Made Easy Problem #5: Scattered Odd Amounts Sometimes there will be cash flows that occur in different amounts and at different times. The key is to treat them as separate lump sums and then add each present value together. 12% 1 2 3 4 5 6 7 $2,500 $4,000 $3,500 PV = $6,826.11 Solution: Present Value of $2,500, end of year 2, 12% = .79719 x $2,500 = $1,992.98 Present Value of $4,000, end of year 3, 12% = .71178 x $4,000 = $2,847.12 Present Value of $3,500, end of year 5, 12% = .56743 x $3,500 = $1,986.01 Grand total and final answer = $6,826.11

Net Present Value Made Easy Problem #6: Mixing Positive and Negative Cash Flows Often times when analyzing business opportunities, there are a combination of positive and negative cash flows. For example, perhaps a business must invest $3,000 for the first three years in order to receive $10,000 at the end of the 4th and 5th years. Again, all cash flows are assumed to take place at the end of each year. 12% 1 2 3 4 5 6 7 -$3,000 -$3,000 -$3,000 $10,000 $10,000 Solution: PV of -$3,000 Annuity, 3 years, 12% = 2.40183 x -$3,000 = -$7,205.49 PV of $10,000, end of year 4, 12% = .63552 x $10,000 = $6,355.20 PV of $10,000, end of year 5, 12% = .56743 x $10,000 = $5,674.30 Grand total and final answer = $4,824.01

Net Present Value Made Easy Putting it All Together So what does this all mean? How do you use it to solve business problems? Here are the steps: #1. Determine the cash flows in regard to the business opportunity you are analyzing and place the cash flows on a time line. #2. Determine a rate of interest. A good place to start is the rate of return you would like to earn. Add percentage points if the opportunity is very risky. #3. Find the present value of all cash flows. Do not forget to distinguish positive and negative cash flows. #4. If the final result of your present value calculations is greater than zero, the project might be worth doing. If the final result of your present value calculations is less than zero, the business opportunity fails the NPV test and the project might not be worth further consideration. Following this slide are some practice problems and solutions.

Net Present Value Made Easy Practice Problem #1: Converting to a Company Wide Software System During years one and two, a company is spending $5,000 each year on a new computer software system. The company expects to save (positive cash flow) $8,000 each year for years 3, 4, 5, & 6. Is the project worthy of consideration if the company expects a 15% return on its investments?

Net Present Value Made Easy Practice Problem #1: Solution The following are the cash flows: 15% 1 2 3 4 5 6 7 -$5,000 -$5,000 $8,000 $8,000 $8,000 $8,000 PV = Solution: PV of -$5,000 Annuity, 2 years, 15% = 1.62571 x -$5,000 = -$8,450.25 PV of $8,000 Annuity, 4 years, 15% = 2.85498 x $8,000 = $22,839.84 (The $22,839.84 is lands at the end of year 2 and must be treated as a lump sum) PV of $22,839.84, end of year 2, 15% = .75614 x $22,839.84 = $17,270.12 Add up the results inside the boxes for the final total = $8,819.87 Since the end result is positive (greater than zero) the project passes the NPV test and might be worthy of further consideration.

Net Present Value Made Easy Practice Problem #2: Adding a New Technology Department A company has decided to add a new technology department. During year one the cost will be $10,000. During years 2 – 7 the cost of operating the department is expected to be $5,000 each year. During year 5, the department will be up-graded. The upgrade will cost $4,000. This $4,000 up-grade is an additional cost over and above the normal operating cost of $5,000 during year 5. The company expects to save (positive cash flow) $9,000 each and every year for years 1 – 7. The company expects to earn a 10% rate of return on this investment. Does the project pass the NPV test?

Net Present Value Made Easy Practice Problem #2: Solution The following are the cash flows: 10% 1 2 3 4 5 6 7 -$10,000 -$5,000-$5,000 -$5,000 -$5,000 -$5,000 -$5,000 -$4,000 $9,000 $9,000 $9,000 $9,000 $9,000 $9,000 $9,000 Here is a technique that sometimes makes the problem easier. Before you begin calculating the present values of the various cash flows, sometimes you can simplify the problem by combining the cash flows for each year. Here is what the cash flows would look like after combining cash flows. 1 2 3 4 5 6 7 -$1,000 $4,000 $4,000 $4,000 $0 $4,000 $4,000

Net Present Value Made Easy Practice Problem #2: Solution As indicated on the previous slide, here are the revised cash flows: 10% 1 2 3 4 5 6 7 -$1,000 $4,000 $4,000 $4,000 $0 $4,000 $4,000 There are a few different ways to go about this, but here is a straight forward approach: PV of -$1,000, lump sum, year 1, 10% = .90909 x -$1,000 = -$909.09 PV of $4,000Annuity, years 2 - 4 (3 years), 10% = 2.48685 x $4,000 = $9,947.40 (the PV of the annuity lands at the end of year 1 and must be treated as a lump sum) PV of $9,947.40, year 1, 10% = ,90909 x $9,947.40 = $9,043.08 PV of $4,000 Annuity, years 6 – 7 (2 years), 10% = 1.73554 x $4,000 = $6,942.16 (the PV of the annuity lands at the end of year 5 and must be treated as a lump sum) PV of $6,942.16, lump sum, year 5, 10% = .62092 x $6,942.16 = $4,310.53

Net Present Value Made Easy Practice Problem #2: Solution Here are the results from the previous slide: PV of -$1,000, lump sum, year 1, 10% = .90909 x -$1,000 = -$909.09 PV of $4,000Annuity, years 2 - 4 (3 years), 10% = 2.48685 x $4,000 = $9,947.40 (the PV of the annuity lands at the end of year 1 and must be treated as a lump sum) PV of $9,947.40, year 1, 10% = ,90909 x $9,947.40 = $9,043.08 PV of $4,000 Annuity, years 6 – 7 (2 years), 10% = 1.73554 x $4,000 = $6,942.16 (the PV of the annuity lands at the end of year 5 and must be treated as a lump sum) PV of $6,942.16, lump sum, year 5, 10% = .62092 x $6,942.16 = $4,310.53 Combining the numbers in the boxes equals $12,444.52 $12,444.52 is greater than zero and so the project passes the NPV test and should be considered further.

Net Present Value Made Easy One Last Bit on How to Do NPV Analysis Look at the following cash flow. See if you can see something that is different from the previous problems. 10% 1 2 3 4 5 6 7 $1,000 $1,000 $1,000 $1,000 $1,000 $1,000 $1,000 The real difference between this problem and the others is that the cash flows begin at the present time. In other words, the first $1,000 cash flow happens immediately. What this means is that the very first cash flow is already at the present value. The moral of the story is that when a cash flow is listed at the beginning of the time line, the amount is already at the present value and no additional calculation are required for that first $1,000. See the next slide for more info

Net Present Value Made Easy A Payment at Time Zero. How to Solve It. Here is the same problem from the previous page. 10% 1 2 3 4 5 6 7 $1,000 $1,000 $1,000 $1,000 $1,000 $1,000 $1,000 The remaining payments form an annuity. Equal payments over equal periods of time. Of the remaining payments we have, 6 payments of $1,000, @10%. PV = $1,000 x 4.35526 = $4,355.26 The first payment is already at its present value because the payment takes place at the very start (time zero) and so for now we can leave it alone. The final answer: The first payment + the PV of the annuity = final answer $1,000 + $4,355.26 = $5,355.26

Net Present Value Made Easy That is the end of Net Present Value Made Easy. If you click the “Back” button on the top left hand corner of the screen once or twice, you will exit this slide show.