Download

1 / 34

360 likes | 496 Views

Audit Requirements. Objectives. Purpose & applicability Responsibilities of auditee & DOL Components of a single audit WIA considerations Testing for compliance Exercise & review questions. Purpose of OMB Circular A-133 Single Audit Act (SAA).

E N D

Objectives • Purpose & applicability • Responsibilities of auditee & DOL • Components of a single audit • WIA considerations • Testing for compliance • Exercise & review questions

Purpose of OMB Circular A-133Single Audit Act (SAA) • To set standards for obtaining consistency and uniformity among Federal agencies for the audit of non-Federal entities expending Federal awards • Provides a snapshot into an organization’s financial operations • Is NOT intended to provide detailed financial coverage or in-depth review of individual programs/awards – too cost prohibitive

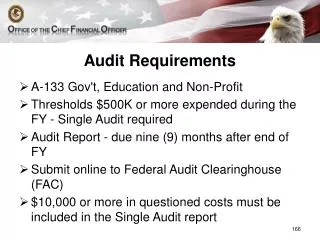

Requirements • Required when any entity expends $500,000 or more in Federal awards in it’s fiscal year • Agencies spending less than $500,000 are exempt • Must make records available for audit or review by the federal agency or pass-through agency • Alternatives: program specific, limited scope or agreed-upon procedures

ApplicabilityWho is required to have a Single Audit? • State and local governments, colleges and universities, hospitals, and non-profit organizations that are direct grant recipients & sub recipients of Federal funds • See the Single Audit Act Amendments of 1996

Commercial Organizations Is the SAA applicable to For-Profit entities? • Direct grant recipients • DOL (Secretary) has the responsibility for audits of grantees that are commercial organizations • Sub-recipient of WIA Title I funds • Commercial organizations that expend $500,000 or more and are a sub recipient under WIA Title I must adhere to OMB Circular A-133 Audit Requirements • WIA Regulations at 20 CFR 667.200

Frequency of Audits • All audits required by OMB A-133 shall be performed annually (exceptions) • Submission to Federal audit clearinghouse • Within one month of completion • No later than 9 months after auditee’s fiscal year

Federal Audit Clearinghouse • Send Single Audit Report Package & Data Collection Form (SF-SAC) to: • Federal Audit Clearinghouse - FACBureau of the Census1201 East 10th Street Jeffersonville, IN 47132 • Phone Numbers: • FAC (Census Bureau) 1-800-253-0696 • Processing Center (Jeffersonville) 1-888-222-9907 • Email: govs.fac@census.gov • FAC’s website allows users to query its audit database • http://harvester.census.gov/sac

Auditee Responsibilities • Identify all Federal awards received and expended by program • Maintain internal control over Federal programs • Comply with laws, regulations, and provisions of contracts or grant agreements • Prepare appropriate financial statements • Ensure audits are properly performed and submitted when due • Prepare schedule of prior audit findings and corrective action plan

Auditee Responsibilities • Always purchase audit services through a competitive procurement process • Periodically review contract terms • Suggest limiting contract extensions to 1-2 years • Guidance: “How to Avoid a Substandard Audit: Suggestions for Procuring an Audit” http://www.gao.gov/govaud/niaf.pdf

Auditee Responsibilities • Entities that pass through federal funds to subrecipients are responsible for: • Ensuring that the requirements of A-133 and the grant are met • Preparing management decisions on subrecipient audit findings

Federal Awarding Agency Responsibilities • Ensure audits and reports are complete and received in timely manner • Make decisions on audit findings in a timely manner • Ensure recipients take timely and appropriate corrective action

DOL’s Responsibilities • From the Federal Audit Clearinghouse, reports are sent to OIG. • OIG reviews & distributes the reports to the appropriate agency for resolution • For DOL-ETA funded programs/grants • Resolution is completed through DOL-ETA’s Grant Officer’s Determination Process • Initial Determination • Includes an informal resolution process • Final Determination • Debt Collection • ALJ Hearing

Components of a Single Audit Report • Schedule of expenditures • Management letter on internal controls, financial statements, compliance to major programs • Provides auditor’s opinion • Schedule of findings & questioned costs • Corrective action plan • Summary of prior year findings • Data collection form (SF-SAC) • Major & non-major programs identified • Risk assessment – high or low risk

Components of a Single Audit ReportAuditor’s Opinions • UNQUALIFIED OPINION states that the financial statements are presented fairly in conformity with GAAP. • Auditor’s Clean Bill of Health • QUALIFIED OPINION is issued when the financial statements present the entity's financial position, results of operations, and cash flows in conformity with GAAP except for the matter of the qualification. Qualified opinions are issued, in some cases, when: (1) a scope limitation, or (2) a departure from GAAP exists. • ADVERSE OPINION is issued when the auditor concludes that the financial statements do not present the entity's financial position, results of operations, and cash flows in conformity with GAAP. This type of opinion is only issued when the financial statements contain very material departures from GAAP. • DISCLAIMER OF OPINION is issued when the auditor is unable to form an opinion on an entity's financial statements. A disclaimer may be issued in cases when: (1) the auditor is not independent with respect to the entity under audit, (2) a material scope limitation exists, or (3) a significant uncertainty exists.

Components of a Single Audit ReportOpinions on Internal Controls • Material Weakness • A material weakness is a significant deficiency in internal control, or combination of deficiencies that results in more than a remote likelihood that a material misstatement of the financial statements will not be prevented or detected. (GAGAS 5.13) • Reportable Condition • For audit periods prior to December 15, 2006 • AICPA standards define reportable conditions as significant deficiencies in the design or operation of internal control that could adversely affect the entity's ability to record, process, summarize, and report financial data consistent with the assertions of management in the financial statements.

Recent ChangesFederal Register 6/26/2007Effective for audit periods after December 15, 2006 • Significant Deficiency – replaces Reportable Condition • Is a control deficiency, or combination of control deficiencies … such that there is more than a remote likelihood that a misstatement of the entity’s financial statements that is more than inconsequential will not be prevented or detected. • Control Deficiency - exists when the design or operation of a control does not allow management or employees, in the course of performing their assigned functions, to prevent or detect misstatements on a timely basis. • Material Weakness – definition has changed • Is a significant deficiency, or combination of significant deficiencies, that results in more than a remote likelihood that a material misstatement of the financial statements will not be prevented or detected.

Components of a Single Audit ReportRisk Assessment • Criteria for HIGH RISK or LOW RISK • Current and prior audit experience • Federal agency and pass-through entity oversight. • Inherent risk of Federal program

Low-Risk Auditee Criteria • Single audits performed annually • Opinion on financial statements are unqualified • Opinion on schedule of expenditures of Federal awards is unqualified • No deficiencies in internal control • No Federal program had audit findings

Audit Working Papers • Retention • Minimum 3 years after issuance of auditor’s report • Access • Available upon request • Copies may be made as necessary and reasonable

WIA Considerations • Non-Federal Resolution • Governor is responsible for resolving the audit findings related to LWIAs and other subrecipients • Must use same resolution process, debt collection, and appeals procedures for WIA as used for other grant programs • ETA Resolution Process • 29 CFR Part 96

Additional WIA Considerations • Waiver of Liability • Through DOL’s Grant Officer, a Grantee may request a waiver of liability from disallowed costs • 20 CFR 667.720(c)(1-5) • Criteria for Waiver • Occurred at the subrecipient level • Not gross negligence, willful disregard or failure to follow standards • If fraud, aggressive action pursued by grantee • Debt established • Formal request with supporting documents is submitted

Additional WIA Considerations • Advance Approval • Contemplated corrective actions • Including debt collection • Grantee request of Grant Officer • Criteria listed in 20 CFR 667.730(b) • Nearly the same as Waiver of Liability

Stand-In Costs Chapter 12, OneStop Financial Management TAG Comptroller General Decision B-208871.2, dated February 9, 1989

What is Stand-In Costs? • Non-Federal costs that may be substituted for disallowed grant costs when certain conditions are met. • Must be for an allowable activity • Within administrative and cost limitations • Recognized in the financial system • Occurred during the same appropriation year • Incurred by the same entity proposing the substitution

Conditions • Must be allowable ETA costs that were actually incurred by the ETA-funded program and paid by a non-ETA fund source. • Must have been included within the scope of the audit (not necessarily tested but potentially subject to testing). • Must have been accounted for in the auditee’s financial system. • Must be adequately documented in the same manner as all other ETA-funded program costs.

Stand-In Costs are NOT • Uncompensated overtime • Unbilled premises costs associated with fully depreciated publicly owned buildings • Allocated costs derived from an improper allocation methodology • Discounts, refunds, rebates • Any State share of the cost of State or community college tuition

Testing for Compliance • How do you ensure compliance with Federal audit requirements at the grantee and sub recipient level? • Interview staff • Review single audit reports

Testing for Compliance • Ask to see their audit files or log for their sub recipients. The file/log should provide at a minimum the following items of information: • Most recent audit report reviewed • Fiscal year • Number of findings • Amount of questioned costs • Current status of corrective action • Missing audit reports • Current status or sanction for non-compliance See Handout for a Sample Audit Resolution Tracking Checklist

Sanctions for Non-Compliance • Percentage of Federal awards withheld until audit completion • Withholding/disallowing overhead costs • Suspend Federal awards • Terminating Federal award

Regulatory References • OMB Circular A-133 • Including the Compliance Supplement • 29 CFR Part 96 • 29 CFR Part 99 • Government Auditing Standards – Yellow Book

Web Resources • http://www.gao.gov/ - Government Auditing Standards (Yellow Book) • http://www.oig.dol.gov/public/reports/oa/documents/singleauditcfoBrochure.pdf - DOL’s Office of Inspector General (OIG) summarizes the audit requirements on their website • http://harvester.census.gov/sac - FAC and Single Audit Database • http://www.access.gpo.gov/nara/cfr/waisidx - Provides links to specific regulations, CFRs, Federal Register notices, public laws, and Privacy Act issuances • http://www.whitehouse.gov/OMB/ -Provides links to all OMB circulars, compliance supplements, and OMB policy • http://www.cfda.gov - Catalog of Federal Domestic Assistance (CFDA) website – Provides CFDA # and description of major federally funded programs

More Web Resources • http://www.doleta.gov/grants/ -One-Stop Financial Management TAG, Grant Closeout System, Workforce Tools of the Trade • http://epls.arnet.gov/- Debarment & Suspension Listing • http://www.dnb.com - Duns & Bradstreet website – D&B number is needed to complete a SF-424 Grant Application • http://thomas.loc.gov/ - Library of Congress THOMAS System that includes the status of federal appropriations, Congressional resources, and legislative Bills