Download

1 / 26

280 likes | 511 Views

At this exchange rate, you purchase a dollar-denominated asset worth $1,000 which is worth 1,000 pesos ... Expected total rate of return on dollar-denominated assets rises ...

E N D

Flexible Exchange Rates CHAPTER 14

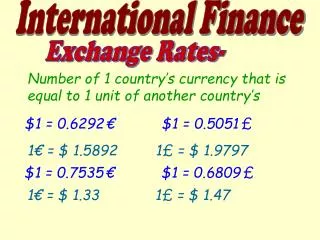

Introduction • Forces of supply and demand in currency markets determine exchange rate • An example of a flexible or floating exchange rate regime • Canadian dollar began the 1990s at 1.651 per US dollar • By 1998, it was trading at 2.155 per US dollar • A fall from 61 US cents to 46 US cents • What makes a flexible exchange rate move one way or another? • This chapter develops a model of how the nominal exchange rate is determined in currency markets • Will consider a trade-based model • Nominal exchange rate is determined by currency transactions arising from imports and exports • Will extend model to account for exchange of assets

A Trade-Based Model • Part of fundamental accounting equations • Foreign Savings = Trade Deficit • Rewrite this relationship using symbols • SF (foreign savings) = Z (imports) - E (exports) or SF = (Z - E) • Use Mexico as home country and United States as foreign country • SF is foreign savings • Savings supplied by US residents who buy Mexican assets • SF is a demand for pesos (supply of dollars) by US • Demand is invariant with respect to value of peso • Gives us the perfectly inelastic demand for pesos curve

A Trade-Based Model • Z - E is the trade deficit • Net demand for US goods by Mexico • A supply of pesos (demand for dollars) by Mexico • Z has a positive relationship to value of peso • E has a negative relationship to value of peso • Thus Z-E has a positive relationship to value of peso

A Trade-Based Model • We are considering the case of a flexible exchange rate regime • e can vary in response to excess supply of or excess demand for pesos • Increase in e or a fall in value of peso • Depreciation of peso • Decrease in e or a rise in value of peso • Appreciation of peso

A Trade-Based Model • Consider three alternative values of the peso • 1 ÷ e1—supply of pesos exceeds demand for pesos • Reduces value of peso • Trade deficit falls—brings the supply and demand of pesos into equality • 1 ÷ e2—demand for pesos exceeds the supply of pesos • Increases value of peso • As peso appreciates, trade deficit rises—brings supply and demand of pesos into equality • 1 ÷ e0—demand for and supply of pesos are exactly the same • Represents equilibrium value of peso, and e0 is the equilibrium nominal exchange rate • Model is trade-based in the sense that only trade flows respond to a change in value of peso

An Assets-Based Model • Views foreign currency transactions as arising from the buying and selling of foreign-currency-denominated assets, rather than from trade flows • Focuses on foreign savings rather than on trade deficit in the SF = Z - E relationship • Pretend you are a Mexican investor, deciding upon the allocation of your wealth portfolio between two assets • A peso-denominated asset • A dollar-denominated asset • For simplicity, assume both assets to be open-ended mutual funds with fixed domestic-currency prices • You will allocate your portfolio with an eye to rates of return of alternative assets

An Assets-Based Model • In the case of peso-denominated assets, return you obtain is the interest rate, or rM • Total expected return on the peso-denominated asset is • Since you are a Mexican investor, dollar-denominated assets are a bit more complicated—you must consider • Interest payment on the dollar-denominated assets, or rUS • Exchange rate • Suppose initial exchange rate is e0 = 1 • At this exchange rate, you purchase a dollar-denominated asset worth $1,000 which is worth 1,000 pesos • Suppose peso depreciates and the new exchange rate is e1 = 1.1 • $1,000 asset has increased in value to 1,100 pesos

An Assets-Based Model • At any point in time, current exchange rate is at a value e • Also, at any point in time, you have your expectation of what exchange rate will be in the future, or ee • Your expected rate of depreciation of the peso is • Your expected total rate of return on dollar-denominated assets is the sum of the interest rate and the expected rate of depreciation of the peso

An Assets-Based Model—Portfolio Allocation • How will you allocate your portfolio between these two asset types? Possibilities include • If expected total rate of return on peso-denominated assets exceeds expected total rate of return on dollar-denominated assets • Since peso-denominated assets offer a higher expected rate of return, reallocate your portfolio towards these assets, selling dollars and buying pesos • If expected total rate of return on dollar-denominated assets exceeds expected total rate of return on peso-denominated assets • Reallocate your portfolio towards dollar-denominated assets, buying dollars and selling pesos • If expected total rate of return on dollar-denominated assets equals expected total rate of return on peso-denominated assets • No reason or incentive to reallocate your portfolio

Interest Rate Parity • Reallocations cause buying of one currency and selling of another • Equilibrium in foreign exchange market requires that • Known as interest rate parity condition • Equilibrium in foreign exchange market requires that interest rate on peso deposits equals interest rate on dollar deposits plus expected rate of peso depreciation

Interest Rate Parity increases in value • Role of the value of the peso in the interest rate parity condition • Suppose initially equilibrium exists • Next suppose value of peso increases or e falls • For a given expected future exchange rate the total expected rate of return on the dollar-denominated asset increases because as e falls • You (along with other investors from all other countries) would sell peso-denominated assets and buy dollar-denominated assets • SF (asset-based demand for pesos) declines

Interest Rate Parity • To understand adjustment process, consider three alternative values of the peso • At 1/e1 supply of pesos exceeds demand for pesos resulting in a fall in value of peso • Trade deficit falls as Z decreases and E increases—decreases supply of pesos • Foreign saving rises • Expected total rate of return on dollar-denominated assets falls • Investors move into peso-denominated assets—increases demand for pesos • Both of these changes bring the peso market towards equilibrium

Interest Rate Parity • At 1/e2 demand for pesos exceeds supply of pesos leading to a rise in value of peso • Trade deficit rises as Z increases and E decreases—increases supply of pesos • Foreign savings falls • Expected total rate of return on dollar-denominated assets rises • Investors move out of peso-denominated assets into dollar-denominated assets—decreases demand for pesos • At e0 demand for and supply of pesos are equal—peso market is in equilibrium

Interest Rates, Expectations, and Exchange Rates • Interest rate parity condition • An increase in rM increases total expected rate of return on peso-denominated assets • Results in an increase in demand for pesos • Shifts demand curve to right and raises value of peso to 1/e1 • An increase in Mexican (home-country) interest rate causes an appreciation of the Mexican (home-country) currency in a flexible exchange rate regime

Interest Rates, Expectations, and Exchange Rates • An increase in rUS increases total expected rate of return on dollar-denominated assets • Results in a decrease in demand for pesos, which shifts the demand curve to left and lowers value of peso to 1/e2 • An increase in US (foreign-country) interest rate causes a depreciation of the Mexican (home-country) currency in a flexible exchange rate regime

Interest Rates, Expectations, and Exchange Rates • Interest rate parity condition involves expectations about future exchange rates • Expectations are formed in the minds of investors and are subjective • Suppose, for example, expected future exchange rate, ee, were to increase in the minds of investors • Would increase total expected rate of return on dollar-denominated assets • Results in a decreased demand for pesos • Shifts demand curve to left which lowers value of peso to 1/e2 • An increase in expected future exchange rate for Mexico’s (home-country’s) currency causes a depreciation of Mexico’s (home-country’s) currency in a flexible exchange rate regime