Download

1 / 14

150 likes | 670 Views

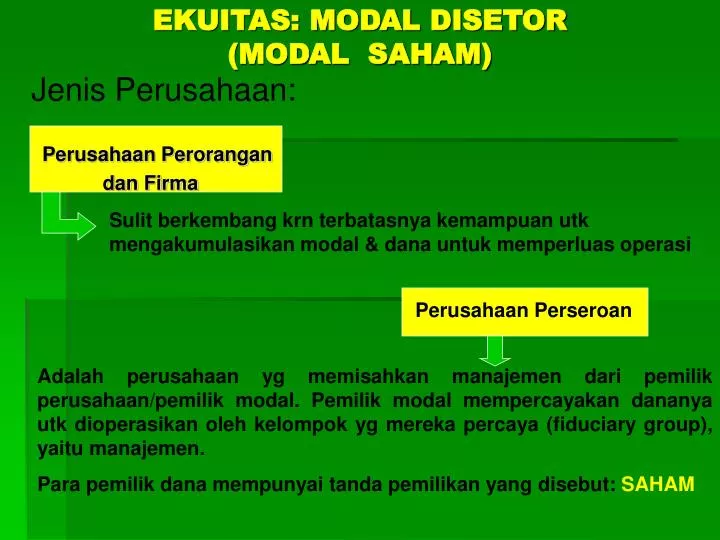

EKUITAS: MODAL DISETOR (MODAL SAHAM). Sulit berkembang krn terbatasnya kemampuan utk mengakumulasikan modal & dana untuk memperluas operasi. Perusahaan Perseroan. Jenis Perusahaan: Perusahaan Perorangan dan Firma.

E N D

EKUITAS: MODAL DISETOR(MODAL SAHAM) Sulit berkembang krn terbatasnya kemampuan utk mengakumulasikan modal & dana untuk memperluas operasi Perusahaan Perseroan Jenis Perusahaan: Perusahaan Perorangan dan Firma Adalah perusahaan yg memisahkan manajemen dari pemilik perusahaan/pemilik modal. Pemilik modal mempercayakan dananya utk dioperasikan oleh kelompok yg mereka percaya (fiduciary group), yaitu manajemen. Para pemilik dana mempunyai tanda pemilikan yang disebut: SAHAM

Keunggulan perusahaan perseroan: • Memungkinkan untuk dapat mengakumulasikan atau menghimpun sumberdaya modal yang lebih besar • Lebih menjamin perusahaan untuk bisa beroperasi pada tingkat atau skala kegiatan yang ekonomis • Lebih berpeluang untuk bisa go public atau akses ke pasar modal dimana sumber dana lebih mudah didapat oleh perusahaan yang bisa beroperasi secara efisien dan efektif Kekurangan: • Pajak berganda (double taxation); Pajak Penghasilan Badan dan individu pemegang saham sebagai pemodal dikenakan Pajak Penghasilan Perseorangan atas penghasilan berupa dividen yang dibagikan oleh perusahaan.

The president is the The controller’s chief executive officer responsibilities include (CEO) with direct 1 maintaining the responsibility for accounting records managing the business. 2 maintaining adequate The chief accounting internal control system officer is the controller. 3 preparing financial statements, tax returns and internal report Stockholders Board of Directors President Corporate Secretary Vice-President Marketing Vice-President Finance Vice-President Production Vice-President Personnel Treasurer Controller SAMPLE CORPORATION ORGANIZATION CHART

Komponen Modal Saham: Komponen modal saham dapat dilihat dalam pencantuman modal saham di Laporan keuangan. Contoh kasus: PT ‘Park Ji Sung’ pada saat pendirian mengotorisasi pengeluaran saham sebanyak 10.000.000 lembar dengan nilai nominal Rp. 1000 per lembar. Jumlah yang disetujui untuk diedarkan adalah 4.000.000 lembar dan dijual dengan harga Rp. 3000 per lembar. 60% dari jumlah tersebut sudah dibayar oleh pembeli

Jenis Saham • Saham Biasa (Common Stock) - Dgn nilai nominal - Tanpa nilai nominal, ttp tercatat pada saat dikeluarkan - Tanpa nilai nominal dan tdk tercatat pada saat dikeluarkan • Saham Prioritas/Preferen (Preferred Stock): Jenis: - Callable; Saham dapat ditebus kembali atas opsi perusahaan penerbit - Convertible; Pemodal dapat menukarkan porto folio investasinyayang saham prioritas ke bentuk saham biasa - Redeemable; Harus dilunasi atau dibayar kembali pada tanggal tertentu sesuai dg kontraknya

Jenis Saham Klausul: - Saham Prioritas Komulatif, Partisipatif - Saham Prioritas Komulatif, tidak Partisipatif - Saham Prioritas tidak Komulatif, Partisipatif - Saham Prioritas tidak komulatif dan tidak Partisipatif Komulatif: berhak memperoleh dividen pada setiap tahun bukunya. Apbl dalam suatu tahun buku dividen belum dibayarkan (disebut dividen menunggak), dividen tersebut tetap harus dibayarkan terlebih dahulu Partisipatif: Bisa memperoleh tambahan dividen setelah dividen dlm jumlah tertentu sudah dibayarkan kepada para pemegang saham biasa

Hak Pemegang Saham • Ikut serta dalam pengelolaan perusahaan atau memilih anggota direksi dan menentukan kebijakan strategis perusahaan • Mendapatkan pembagian laba dalam bentuk dividen yang dibagikan oleh perusahaan • Mendapatkan aktiva bersih, apabila perusahaan dilikuidasi • Mempertahankan jumlah relatif saham yang dimiliki, melalui pembelian saham baru yang diterbitkan perusahaan (preemptive right) Note: Pemegang saham prioritas mendapatkan hak point 2 & 3 didahulukan drpd pemegang saham biasa

Beberapa istilah: • Saham yang diotorisasi (Authorized) • Saham yang beredar (Issued) • Outstanding stock • Nilai nominal/nilai pari/par value • Nilai/harga pasar/Kurs • Nilai buku/Book value

Penjualan Saham: 1. Secara Tunai ACCOUNTING FOR COMMON STOCK ISSUES at PAR VALUE Hydro-Slide, Inc. issues 1,000 shares of $1 par value common stock at par for cash. The entry to record this transaction is: 1000 1000

ACCOUNTING FOR COMMONSTOCK ISSUES at GREATERTHAN PAR VALUE 5,000 1,000 4,000 Hydro-Slide, Inc. issues an additional 1,000 shares of the $1 par value common stock for cash at $5 per share. The entry to record this transaction is:

ACCOUNTING FOR COMMON STOCK ISSUESwithSTATED VALUES Paid-in Capital in Excess of Stated Value is reported as part of paid-in capital in the stockholders’ equity section. When no-par stock does not have a stated value, the entire proceeds from the issue become legal capital and are credited to Common Stock. If Hydro-Slide does not assign a stated value to its no-par stock, the issuance of the 5,000 shares at $8 per share for cash is recorded as follows: 40,000 40,000

ACCOUNTING FOR COMMON STOCK ISSUESat GREATER THANSTATED VALUES When no-par common stock has a stated value, the entries are similar to those for par value stock. The stated value represents legal capital and therefore is credited to Common Stock. When the selling price of no-par stock exceeds stated value, the excess is credited to Paid-in Capital in Excess of Stated Value. Hydro-Slide, Inc. issues 5,000 shares of $5 stated value no-par stock at $8 per share for cash. The entry is: 40,000 25,000 15,000

ACCOUNTING FOR COMMONSTOCK ISSUESforASSETSOTHER THAN CASH 80,000 50,000 30,000 Athletic Research Inc. is a publicly held corporation whose $5 par value stock is actively traded at $8 per share. The company issues 10,000 shares of stock to acquire land recently advertised for sale at $90,000. On the basis of these facts the market price of the consideration given is the most clearly evident value. The par or stated value of the stock is never a factor in determining the cost of the assets received. The entry is: