Download

1 / 43

430 likes | 577 Views

Loan Portfolio Selection and Risk Measurement. Chapters 10 and 11. The Paradox of Credit. Lending is not a “buy and hold”process. To move to the efficient frontier, maximize return for any given level of risk or equivalently, minimize risk for any given level of return.

E N D

Loan Portfolio Selection and Risk Measurement Chapters 10 and 11

The Paradox of Credit • Lending is not a “buy and hold”process. • To move to the efficient frontier, maximize return for any given level of risk or equivalently, minimize risk for any given level of return. • This may entail the selling of loans from the portfolio. “Paradox of Credit” – Fig. 10.1. Saunders & Allen Chapters 10 & 11

Managing the Loan Portfolio According to the Tenets of Modern Portfolio Theory • Improve the risk-return tradeoff by: • Calculating default correlations across assets. • Trade the loans in the portfolio (as conditions change) rather than hold the loans to maturity. • This requires the existence of a low transaction cost, liquid loan market. • Inputs to MPT model: Expected return, Risk (standard deviation) and correlations Saunders & Allen Chapters 10 & 11

The Optimum Risky Loan Portfolio – Fig. 10.2 • Choose the point on the efficient frontier with the highest Sharpe ratio: • The Sharpe ratio is the excess return to risk ratio calculated as: Saunders & Allen Chapters 10 & 11

Problems in Applying MPT to Untraded Loan Portfolios • Mean-variance world only relevant if security returns are normal or if investors have quadratic utility functions. • Need 3rd moment (skewness) and 4th moment (kurtosis) to represent loan return distributions. • Unobservable returns • No historical price data. • Unobservable correlations Saunders & Allen Chapters 10 & 11

KMV’s Portfolio Manager • Returns for each loan I: • Rit = Spreadi + Feesi – (EDFi x LGDi) – rf • Loan Risks=variability around EL=EGF x LGD = UL • LGD assumed fixed: ULi = • LGD variable, but independent across borrowers: ULi = • VOL is the standard deviation of LGD. VVOL is valuation volatility of loan value under MTM model. • MTM model with variable, indep LGD (mean LGD): ULi = Saunders & Allen Chapters 10 & 11

Valuation Under KMV PM • Depends on the relationship between the loan’s maturity and the credit horizon date: • Figure 11.1: DM if loan’s maturity is less than or equal to the credit horizon date (maturities M1 or M2). • MTM if loan’s maturity is greater than credit horizon date (maturity M3). See Appendix 11.1 for valuation. Saunders & Allen Chapters 10 & 11

Correlations • Figure 11.2 – joint PD is the shaded area. • GF = GF/GF • GF = • Correlations higher (lower) if isocircles are more elliptical (circular). • If JDFGF = EDFGEDFF then correlation=0. Saunders & Allen Chapters 10 & 11

Role of Correlations • Barnhill & Maxwell (2001): diversification can reduce bond portfolio’s standard deviation from $23,433 to $8,102. • KMV diversifies 54% of risk using 5 different BBB rated bonds. • KMV uses asset (de-levered equity) correlations, CreditMetrics uses equity correlations. • Correlation ranges: • KMV: .002 to .15 • Credit Risk Plus: .01 to .05 • CreditMetrics: .0013 to .033 Saunders & Allen Chapters 10 & 11

Calculating Correlations using KMV PM • Construct asset returns using OPM. • Estimate 3-level multifactor model. Estimate coefficients and then evaluated asset variance and correlation coefficients using: • First level decomposition: • Single index model – composite market factor constructed for each firm. • Second level decomposition: • Two factors: country and industry indices. • Third level decomposition: • Three sets of factors: (1) 2 global factors (market-weighted index of returns for all firms and return index weighted by the log of MV); (2) 5 regional factors (Europe, No. America, Japan, SE Asia, Australia/NZ); (3) 7 sector factors (interest sensitive, extraction, consumer durables, consumer nondurables, technology, medical services, other). Saunders & Allen Chapters 10 & 11

CreditMetrics Portfolio VAR • Two approaches: • Assuming normally distributed asset values. • Using actual (fat-tailed and negatively skewed) asset distributions. • For the 2 Loan Case, Calculate: • Joint migration probabilities • Joint payoffs or loan values • To obtain portfolio value distribution. Saunders & Allen Chapters 10 & 11

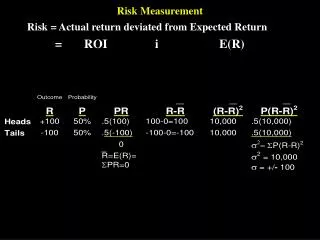

The 2-Loan Case Under the Normal Distribution • Joint Migration Probabilities = the product of each loan’s migration probability only if the correlation coefficient=0. • From Table 10.1, the probability that obligor 1 retains its BBB rating and obligor 2 retains it’s a rating would be 0.8693 x 0.9105 = 79.15% if the loans were uncorrelated. The entry of 79.69% suggests a positive correlation of 0.3. Saunders & Allen Chapters 10 & 11

Mapping Ratings Transitions to Asset Value Distributions • Assume that assets are normally distributed. • Compute historic transition matrix. Figure 11.3 uses the matrix for a BB rated loan. • Suppose that historically, there is a 1.06% probability of transition to default. This corresponds to 2.3 standard deviations below the mean on the standard normal distribution. • Similarly, if there is a 8.84% probability of downgrade from BB to B, this corresponds to 1.23 standard deviations below the mean. Saunders & Allen Chapters 10 & 11

Joint Transition Matrix • Can draw a figure like Fig. 11.3 for the A rated obligor. There is a 0.06% PD, corresponding to 3.24 standard deviations below the mean; a 5.52% probability of downgrade from A to BBB, corresponding to 1.51 std dev below the mean. • The joint probability of both borrowers retaining their BBB and A ratings is: the probability that obligor 1’s assets fluctuate between –1.23 to +1.37 and obligor 2’s assets between –1.51 to +1.98 with a correlation coefficient=0.2. Calculated to equal 73.65%. Saunders & Allen Chapters 10 & 11

Calculating Correlation Coefficients • Estimate systematic risk of each loan – the relationship between equity returns and returns on market/industry indices. • Estimate the correlation between each pair of market/industry indices. • Calculate the correlation coefficient as the weighted average of the systematic risk factors x the index correlations. Saunders & Allen Chapters 10 & 11

Two Loan Example of Correlation Calculation • Estimate the systematic risk of each company by regressing the stock returns for each company on the relevant market/industry indices. • RA = .9RCHEM + UA • RZ = .74RINS + .15RBANK + UZ • A,Z=(.9)(.74)CHEM,INS + (.9)(.15)CHEM,BANK • Estimate the correlation between the indices. • If CHEM,INS =.16 and CHEM,BANK =.08, then AZ=0.1174. Saunders & Allen Chapters 10 & 11

Joint Loan Values • Table 11.1 shows the joint migration probabilities. • Calculate the portfolio’s value under each of the 64 possible credit migration possibilities (using methodology in Chap.6) to obtain the values in Table 11.3. • Can draw the portfolio value distribution using the probabilities in Table 11.1 and the values in Table 11.3. Saunders & Allen Chapters 10 & 11

Credit VAR Measures • Calculate the mean using the values in Table 11.3 and the probabilities in Tab 11.1. • Mean = • Variance = • Mean=$213.63 million • Standard deviation= $3.35 million Saunders & Allen Chapters 10 & 11

Calculating the 99th percentile credit VAR under normal distribution • 2.33 x $3.35 = $7.81 million • Benefits of diversification. The BBB loan’s credit VAR (alone) was $6.97million. Combining 2 loans with correlations=0.3, reduces portfolio risk considerably. Saunders & Allen Chapters 10 & 11

Calculating the Credit VAR Under the Actual Distribution • Adding up the probabilities (from Table 11.1) in the lowest valuation region in Table 11.3, the 99th percentile credit VAR using the actual (not normal) distribution is $204.4 million. • Unexpected Losses=$213.63m - $204.4m = $9.23 million (>$7.81m). • If the current value of the portfolio = $215m, then Expected Losses=$215m - $213.63m = $1.37m. Saunders & Allen Chapters 10 & 11

CreditMetrics with More Than 2 Loans in the Portfolio • Cannot calculate joint transition matrices for more than 2 loans because of computational difficulties: A 5 loan portfolio has over 32,000 joint transitions. • Instead, calculate risk of each pair of loans, as well as standalone risk of each loan. • Use Monte Carlo simulation to obtain 20,000 (or more) possible asset values. Saunders & Allen Chapters 10 & 11

Monte Carlo Simulation • First obtain correlation matrix (for each pair of loans) using the systematic risk component of equity prices. Table 11.5 • Randomly draw a rating for each loan from that loan’s distribution (historic rating migration) using the asset correlations. • Value the portfolio for each draw. • Repeat 20,000 times! New algorithms reduce some of the computational requirements. • The 99th% VAR based on the actual distribution is the 200th worst value out of the 20,000 portfolio values. Saunders & Allen Chapters 10 & 11

MPT Using CreditMetrics • Calculate each loan’s marginal risk contribution = the change in the portfolio’s standard deviation due to the addition of the asset into the portfolio. • Table 11.6 shows the marginal risk contribution of 20 loans – quite different from standalone risk. • Calculate the total risk of a loan using the marginal contribution to risk = Marginal standard deviation x Credit Exposure. Shown in column (5) of Table 11.6. Saunders & Allen Chapters 10 & 11

Figure 11.4 • Plot total risk exposure using marginal risk contributions (column 6 of Table 11.6) against the credit exposure (column 5 of Table 11.4). • Draw total risk isoquants using column 5 of Table 11.6. • Find risk outliers such as asset 15 which have too much portfolio risk ($270,000) for the loan’s size ($3.3 million). • This analysis is not a risk-return tradeoff. No returns. Saunders & Allen Chapters 10 & 11

Default Correlations Using Reduced Form Models • Events induce simultaneous jumps in default intensities. • Duffie & Singleton (1998): Mean reverting correlated Poisson arrivals of randomly sized jumps in default intensities. • Each asset’s conditional PD is a function of 4 parameters: h (intensity of default process); (constant arrival prob.); k (mean reversion rate); (steady state constant default intensity). • The jumps in intensity follow an exponential distribution with mean size of jump=J. • So: probability of survival from time t to s: Saunders & Allen Chapters 10 & 11

Numerical Example • Suppose that =.002, k=.5, =.001, J=5, h(0)=.001 (corresponds to an initial rating of AA). • Correlations across loan default probabilities: • Vc=common factor; V=idiosyncratic factor. As v0, corr0 As v1, corr1. • If v=.02, V=.001, Vc=.05: the probability that loani intensity jumps given that loanj has experienced a jump is = vVc/(Vc+V) = 2%. If v= .05 (instead of .02), then the probability increases to 5%. • Figure 11.5 shows correlated jumps in default intensities. • Figure 11.6 shows the impact of correlations on the portfolio’s risk. Saunders & Allen Chapters 10 & 11

Appendix 11.1: Valuing a Loan that Matures after the Credit Horizon – KMV PM • Maturity=M3 in Figure 11.1. Use MTM to value loans. • Four Step Process: • 1. Valuation of an individual firm’s assets using random sampling of risk factors. • 2. Loan valuation based on the EDFs implied by the firm’s asset valuation. • 3. Aggregation of individual loan values to construct portfolio value. • 4. Calculation of excess returns and losses for portfolio. • Yields a single estimate for expected returns (losses) for each loan in the portfolio. Use Monte Carlo simulation (repeated 50,000 to 200,000 times) to trace out distribution Saunders & Allen Chapters 10 & 11

Step 1: Valuation of Firm Assets at 3 Time Horizons – Fig. 11.7 • A0 , AH , AMvaluations. Stochastic process generating AH, AM: • The random component = systematic portion f + firm-specific portion u. Each simulation draws another risk factor. • Using AH andAMcan calculate EDFH and EDFM Saunders & Allen Chapters 10 & 11

Step 2: Loan Valuation Using Term Structure of EDFs • Convert EDF into QDF by removing risk-adjusted ROR. • Also value loan as of credit horizon date H: Saunders & Allen Chapters 10 & 11

Step 3: Aggregation to Construct Portfolio • Sum the expected values VHfor all loans in the portfolio. Saunders & Allen Chapters 10 & 11

Step 4: Calculation of Excess Returns/Losses • Excess Returns on the Portfolio: • Expected Loss on the Portfolio: • Repeat steps 1 through 4 from 50,000 to 200,000 times. Saunders & Allen Chapters 10 & 11

A Case Study: KMV PM valuation of 5 yr maturity $1 loan paying a fixed rate of 10% p.a. • Using Table 11.8: Saunders & Allen Chapters 10 & 11

Valuing the Loan at the Credit Horizon Date =1 • Using Table 11.9: Saunders & Allen Chapters 10 & 11

KMV’s Private Firm Model • Calculate EBITDA for private firm j in industryj. • Calculate the average equity mulitple for industryi by dividing the industry average MV of equity by the industry average EBITDA. • Obtain an estimate of the MV of equity for firm j by multiplying the industry equity multiple by firm j’s EBITDA. • Firm j’s assets = MV of equity + BV of debt • Then use valuation steps as in public firm model. Saunders & Allen Chapters 10 & 11

Credit Risk Plus Model 2 - Incorporating Systematic Linkages in Mean Default rates • Mean default rate is a function of factor sensitivities to different independent sectors (industries or countries). • Table 11.7 shows as example of 2 loans sensitive to a single factor (parameters reflect US national default rates). As credit quality declines (m gets larger), correlations get larger. Saunders & Allen Chapters 10 & 11