Download

1 / 11

110 likes | 388 Views

Annuities. Key Terms:. Annuity: A series of payments or investments made at regular intervals. These payments are referred to as ‘ R ’. Couple of Key Points: In this unit, we’ll be focusing on simple annuities . This means that the payments coincide with the compounding period.

E N D

Key Terms: Annuity: A series of payments or investments made at regular intervals These payments are referred to as ‘R’ • Couple of Key Points: • In this unit, we’ll be focusing on simple annuities. This means that the payments coincide with the compounding period. • We’ll also be focusing on ordinary annuities. This means that the payments are made at the end of each interval.

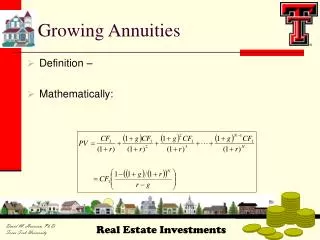

Future Value The future value of an annuity can be represented as a geometric series. Replacing ‘a’ with R(the regular payments), and ‘r’ with (1 + i), we obtain the following formula: The future value of an annuity is the sum of all regular payments and interest earned.

Present Value The present value of an annuity can be represented as a geometric series. The formula is: The present value of an annuity is the value of the annuity at the beginning of the term. It is the sum of all present values of the payments.

Example Zara would like to buy a new Pontiac Solstice that costs $32 000. The dealership offers to finance the car at 2.4% compounded monthly for five year with monthly payments. What will be Zara’s monthly payment if she buys this car? Thus, Zara’s monthly payment would be $566.57.

A Tricky Problem! • Often times the greatest difficulty that students have in solving annuity problems is not the calculations. • It’s deciding whether the problem needs you to use the F.V. or P.V. formula • Here are some hints that might help you!

Future Value Trying to attain an end goal How much will all payments add up to after a specified time. Connected to items you want to buy in the future Usually sound fairly straightforward. Present Value Connected to items that you are buying right now. Calculating payments on items that you have bought via financing Often involve person receiving regular payouts from an investment that he/she has accuulated Problems can sound more confusing Which one am I?

You decide!! Read the following problem • At the end of each year, Mr. Fox deposits $2600 in an RRSP. The interest rate is 7.2%/a compounded annually. He contributes to this RRSP for 20 years, at the end of which time he retires. Upon retiring, Mr. Fox decides to transfer all of this RRSP to an RIF. The interest rate for the RIF is 8.4% compounded quarterly. • Mr. Fox wishes to deplete the fund after 15 years. What will be the quarterly payment from the RIF.

Hmmm….. • Think about what the problem is asking you to do and how you would go about solving this apparent “monster” of a problem • With the person sitting beside you discuss strategies • Share your ideas with the class

Solution? • It is a Future value problem, followed by a present value problem. • The tricky part is that we have to transfer ourselves 20 years into the future to when Mr. Fox starts making his RIF payments and consider that to be our new “Present” • Ugh!!

Your Turn • Complete “What Am I?” Handout • Homework: • Pg 511 5, 7 • Pg 520 3,8