Download

1 / 6

60 likes | 161 Views

Why a good credit score matters. Lower interest rates Credit cards, car loans, mortgage Lower auto insurance premiums Rent an apartment Avoid larger security deposit or paying additional months’ rent up front Better cell phone and cable rates

E N D

Why a good credit score matters • Lower interest rates • Credit cards, car loans, mortgage • Lower auto insurance premiums • Rent an apartment • Avoid larger security deposit or paying additional months’ rent up front • Better cell phone and cable rates • Employers may also be interested in your credit score • Shows you are dependable

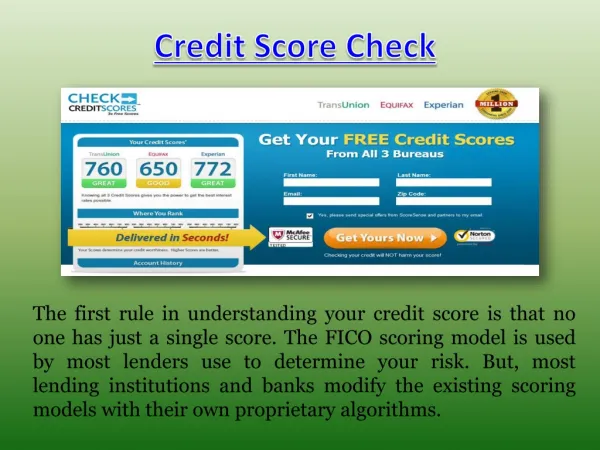

“Establishing a credit score, however, can be a bit of a Catch-22. You build a credit history primarily by taking out loans, but you can't take out loans without a credit history. So how do you establish credit for the first time?” -Rob Berger

Ways to build Credit • Credit card • Student Credit Card • Secured Credit Card • Put security deposit down ($200-$500) and after some time, approx 1 year, get security deposit back, raise credit limit, and can get a regular credit card • Apply for additional cards through department stores or for something specific like gas and pay in full each month • Car loans • Paying utilities in your name—if don’t pay on time major hit to credit score

What makes up your FICO Score? • 35% payment history. • 30% amounts owed. • 15% length of credit history. • 10% new credit. • 10% types of credit used.

Advice • Start building credit as soon as you can and feel ready to • Build responsibility by using a debit card first although debit cards do not do much to build credit • If you carry a balance on your card keep it at or below 30% of your credit limit • Leave accounts open in good standing even if you do not use the card anymore • Adds to length of credit history • Don’t apply for too much credit b/c this lowers your score • Keep track of your credit score

Sourceshttp://money.msn.com/credit-rating/article.aspx?post=45196da9-83b9-4229-8435-14415c64fe16http://www.cbsnews.com/news/5-ways-to-build-a-good-credit-score-from-scratch/Sourceshttp://money.msn.com/credit-rating/article.aspx?post=45196da9-83b9-4229-8435-14415c64fe16http://www.cbsnews.com/news/5-ways-to-build-a-good-credit-score-from-scratch/