Download

1 / 10

100 likes | 203 Views

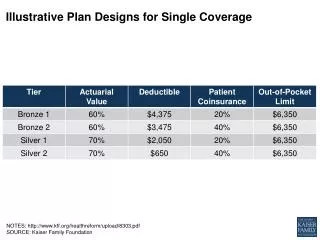

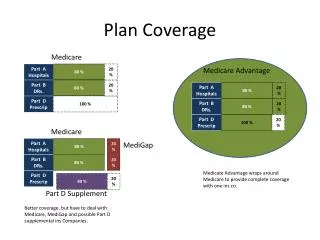

Plan Coverage. Medicare. Part A Hospitals. 80 %. 2 0 %. Medicare Advantage. Part B DRs. 80 %. 2 0 %. Part A Hospitals. 80 %. 2 0 %. Part D Prescrip. 100 %. Part B DRs. 80 %. 2 0 %. Part D Prescrip. 100 %. 2 0 %. Medicare. Part A Hospitals. 80 %. 2 0 %.

E N D

Plan Coverage Medicare Part A Hospitals 80 % 20 % Medicare Advantage Part B DRs. 80 % 20 % Part A Hospitals 80 % 20 % Part D Prescrip 100 % Part B DRs. 80 % 20 % Part D Prescrip 100 % 20 % Medicare Part A Hospitals 80 % 20 % MediGap Part B DRs. 80 % 20 % Medicate Advantage wraps around Medicare to provide complete coverage with one ins co. Part D Prescrip 80 % 20 % Part D Supplement Better coverage, but have to deal with Medicare, MediGap and possible Part D supplemental ins Companies.

Plan Comparisons Need Policy Need Policy

These contractors, called “health plan sponsors” or Medicare Advantage Organizations (MAOs), offer Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Private-Fee-for-Service (PFFS) plans, and more, to Medicare beneficiaries. These private plans must cover the same services and benefits that are available through the Original Medicare program. Benefit Period —The way that Original Medicare measures your use of hospital and skilled nursing facility (SNF) services. A benefit period begins the day you are admitted as an inpatient in a hospital or skilled nursing facility. The benefit period ends when you haven’t received any inpatient hospital care (or skilled care in a SNF) for 60 days in a row. If you go into a hospital or a skilled nursing facility after one benefit period has ended, a new benefit period begins. You must pay the inpatient hospital deductible for each benefit period. There is no limit to the number of benefit periods.

HMO vs PPO How HMOs and PPOs Differ The following outline compares some of the features of HMOs and PPOs. These are general rules and you should speak with your human resources office at work or directly with your health plan. If you are in the process of deciding between enrolling in a HMO or PPO, you often can compare the plans by going online to the plans' websites to learn about the available benefits and costs. Which health care providers must I choose? HMO: You must choose doctors, hospitals, and other providers in the HMO network. PPO: You can choose doctors, hospitals, and other providers from the PPO network or from out-of-network. If you choose an out-of-network provider, you most likely will pay more. Do I need to have a primary care physician (PCP)? HMO: Yes, your HMO will not provide coverage if you do not have a PCP. PPO: No, you can receive care from any doctor you choose. But remember, you will pay more if the doctors you choose are not "preferred" providers. How do I see a specialist? HMO: You will need a referral from your PCP to see a specialist (such as a cardiologist or surgeon) except in emergency situations. Your PCP also must refer you to a specialist who is in the HMO network. PPO: You do not need a referral to see a specialist. However, some specialists will only see patients who are referred to them by a primary care doctor. And, some PPOs require that you get a prior approval for certain expensive services, such as MRIs. Do I have to file any insurance claims? HMO: All of the providers in the HMO network are required to file a claim to get paid. You do not have to file a claim, and your provider may not charge you directly or send you a bill. PPO: If you get your healthcare from a network provider you usually do not need to file a claim. However, if you go out of network for services you may have to pay the provider in full and then file a claim with the PPO to get reimbursed. The money you receive from the PPO will most likely be only part of the bill. You are responsible for any part of the doctor's fee that the PPO does not pay. How do I pay for services in the network? HMO: The only charges you should incur for in-network services are copayments for doctor's visits and other services such as procedures and prescriptions. PPO: In most PPO networks you will only be responsible for the copayment. Some PPOs do have an annual deductable for any services, in network or out of network. How do I pay for services out of the network? HMO: Except for certain types of care that may not be available from a network provider, you are not covered for any out-of-network services. PPO: If you choose to go outside the PPO network for your care, you will need to pay the provider and then get reimbursed by the PPO. Most likely, you will have to pay an annual deductable and coinsurance. For example, if the out-of-network doctor charged you $200 for a visit, you are responsible for the full amount if you have not met your deductable. If you have met the deductable, the PPO may pay 60%, or $120 and you will pay 40%, or $80.

Doughnut Hole What IS the Doughnut Hole? The “doughnut hole” refers to a gap in prescription drug coverage under Medicare Part D. In 2011, once you reach $2,840 in prescription drug costs (which include both your share of covered drugs and the amount paid by your insurance,) you will be in the coverage gap. During this gap in coverage, if you are not receiving Extra Help (the low-income subsidy), you pay the full costs for prescription drugs. When your total out-of-pocket costs reach $4,550, you qualify for catastrophic coverage.” At that point, you are responsible for only 5% of your prescription drug costs for the rest of the year. Starting in 2011, you will get a 50% discount on brand-name drugs and a 7% discount on generic prescription drugs while you are in the coverage gap. Because of the Affordable Health Care Act of 2010, the coverage gap/ “Doughnut Hole” will gradually narrow until it disappears in 2020. If you want to see whether you are eligible for the Medicare Extra Help Program, check out Benefits Quicklink. To share your experiences with the doughnut hole calculator and ask questions, visit the Medicare Part D online community group. Find out more about how the new health care law helps people who fall into the doughnut hole this year by checking out this fact sheet. Learn more about the doughnut hole at this AARP Bulletin guide on Medicare Prescription Drug Coverage.

MediGap Medigap insurance, which is sold by private companies, helps pay for costs that Medicare doesn’t cover, such as copayments and deductibles. Medigap coverage is available only to people who have Original Medicare Parts A and B. If you opted for a Medicare Advantage health plan (aka Part C), you cannot also buy a Medigap policy. Although you do have out-of-pocket expenses with Medicare Advantage, they are typically not as great as with Original Medicare. As a general rule, if you are younger than 65 and on Medicare due to disability, you are not eligible to enroll in a Medigap plan. Exceptions exist, however. Contact your state insurance department for more information. Eleven standard Medigap policies are available in most states. Each lettered plan — A through G and K through N — offers a different set of benefits, filling different gaps in Medicare Parts A and B coverage. All Medigap plans with the same letter provide the same benefits. Only the premiums and the sponsors of the plans vary. By law, you can choose only one of these plans. Insurers are not allowed to sell more than one Medigap plan to you. If your spouse is covered by Medicare and also wants Medigap coverage, he or she will need to buy a separate policy. Generally, standard Medigap policies cover some or all of the cost of:• Your Part A deductible and coinsurance (i.e. the 20 percent Medicare doesn't cover) for hospital stays • Your portion of your doctor’s bills for Part B services• The first three pints of blood annually, if needed• Hospice care coinsuranceMedigap plans do not cover:• Long-term care to help you bathe, dress, eat or use the bathroom• Vision care, eyeglasses, hearing aids or dental care • Private-duty nursing • Prescription drugs, or any out-of-pocket costs for Part D plansBefore Buying a Medigap PolicyWhen deciding what to do, review what other health insurance you have in addition to Medicare, if any. If you already have a comprehensive retiree health plan to supplement Original Medicare, you may not need a Medigap plan. If your retiree policy provides more-generous benefits, or benefits not covered by Medicare or Medigap policies, you should think carefully before dropping your retiree health plan for a less expensive choice. (You might not be able to get that employer plan back once you drop it.) Check with your union or your former employer’s benefits manager or health plan to make sure you understand all the stipulations.Can you accept some restrictions on your care? If so, Medicare Select is a Medigap policy that limits the providers you can see. Costs can be lower than with standard Medigap policies because Medicare Select policies cover services only at certain hospitals and through specific doctors. Your state insurance department can tell you if there are Medicare Select plans in your state and give you more information about them. • MediGap Qs: • Doctors – HMO/PPO? • Cost – premium, copay, out of pocket max • Medigapvs Advantage? When does medigap make sense? • Prescriptions?