Download

1 / 8

80 likes | 187 Views

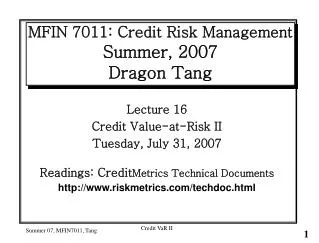

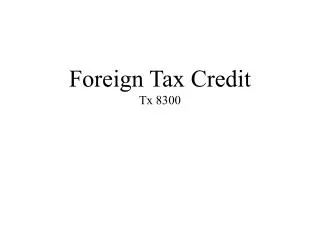

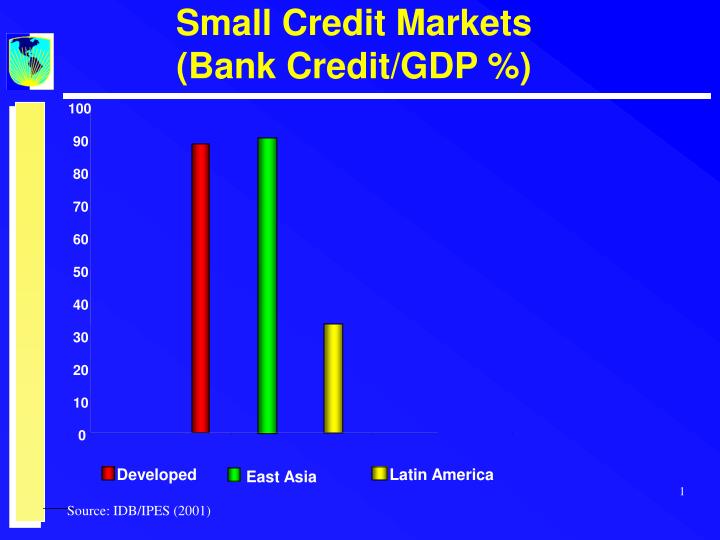

Small Credit Markets (Bank Credit/GDP %). 100. 90. 80. 70. 60. 50. 40. 30. 20. 10. 0. Developed. Latin America. East Asia. Source: IDB/IPES (2001). Effective Creditor Rights. AVERAGE SOUTH-EAST ASIA. AVERAGE OECD. AVERAGE LAC. 0. 0.1. 0.2. 0.3. 0.4. 0.5. 0.6.

E N D

Small Credit Markets (Bank Credit/GDP %) 100 90 80 70 60 50 40 30 20 10 0 Developed Latin America East Asia Source: IDB/IPES (2001)

Effective Creditor Rights AVERAGE SOUTH-EAST ASIA AVERAGE OECD AVERAGE LAC 0 0.1 0.2 0.3 0.4 0.5 0.6 Source: Galindo and Micco(2001); Security Interests= Rule of Law * Creditor Rights

The Legal-Institutional Framework for Property Rights • 1. The cadastre • 2. The property registry office • 3. Cadastral and registry law • 4. The banking system • 5. Enforcement law and procedures

Sequence Matters • The chain is only as strong as its weakest link

What Happens When You Get it Right? • Home ownership expands • Access to credit at lower rates of interest • Safer and sounder banking system • Deeper financial system, longer lending terms

A Word about Competitiveness • It is difficult to compete if property markets don’t work • Companies are afraid to invest if they are not sure who owns what • Individuals are afraid to buy property if they can’t be sure if the seller owns it • The cost of capital is structurally higher