Download

1 / 4

40 likes | 125 Views

Q1. 2012. MARKET REVIEW AND ECONOMIC OUTLOOK.

E N D

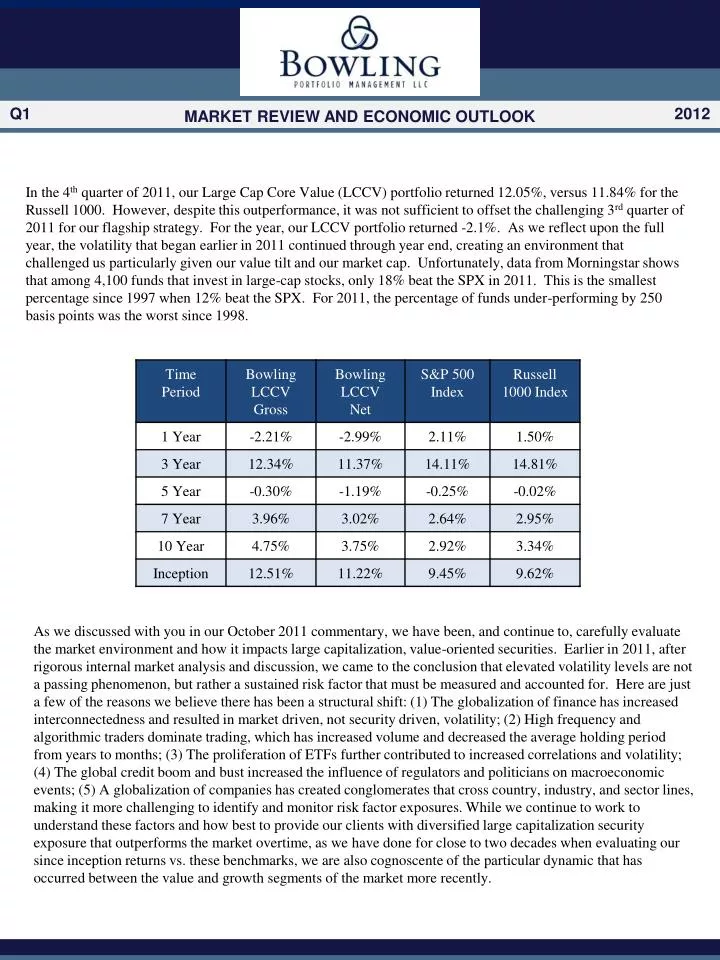

Q1 2012 MARKET REVIEW AND ECONOMIC OUTLOOK In the 4th quarter of 2011, our Large Cap Core Value (LCCV) portfolio returned 12.05%, versus 11.84% for the Russell 1000. However, despite this outperformance, it was not sufficient to offset the challenging 3rd quarter of 2011 for our flagship strategy. For the year, our LCCV portfolio returned -2.1%. As we reflect upon the full year, the volatility that began earlier in 2011 continued through year end, creating an environment that challenged us particularly given our value tilt and our market cap. Unfortunately, data from Morningstar shows that among 4,100 funds that invest in large-cap stocks, only 18% beat the SPX in 2011. This is the smallest percentage since 1997 when 12% beat the SPX. For 2011, the percentage of funds under-performing by 250 basis points was the worst since 1998. As we discussed with you in our October 2011 commentary, we have been, and continue to, carefully evaluate the market environment and how it impacts large capitalization, value-oriented securities. Earlier in 2011, after rigorous internal market analysis and discussion, we came to the conclusion that elevated volatility levels are not a passing phenomenon, but rather a sustained risk factor that must be measured and accounted for. Here are just a few of the reasons we believe there has been a structural shift: (1) The globalization of finance has increased interconnectedness and resulted in market driven, not security driven, volatility; (2) High frequency and algorithmic traders dominate trading, which has increased volume and decreased the average holding period from years to months; (3) The proliferation of ETFs further contributed to increased correlations and volatility; (4) The global credit boom and bust increased the influence of regulators and politicians on macroeconomic events; (5) A globalization of companies has created conglomerates that cross country, industry, and sector lines, making it more challenging to identify and monitor risk factor exposures. While we continue to work to understand these factors and how best to provide our clients with diversified large capitalization security exposure that outperforms the market overtime, as we have done for close to two decades when evaluating our since inception returns vs. these benchmarks, we are also cognoscente of the particular dynamic that has occurred between the value and growth segments of the market more recently.

FIRST QUARTER 2012 MARKET OUTLOOK For the year, the S&P 500 Growth index outperformed the S&P 500 Value index by a whopping 5.13%. Additionally, the outperformance by mega-caps in the major indices is also a notable factor in evaluating relative performance in 2011 as a significant over or underweight to these mega-caps would have driven performance in either direction for the year. The chart on the following page shows the S&P 500 equal weighted return minus the S&P 500 market weighted return since 1992. As can be seen in this chart, the equal-weight S&P 500 returns significantly lagged the market cap weighted returns in the 3rd quarter. In fact, the difference was nearly 400 basis points, a phenomenon seen during only 3 quarters over the last 11 years, including the 3rd quarter of 2011. To date, our portfolios have been constructed using an equally weighted methodology in an effort to reduce risk on behalf of our investors. As a result, in periods of time where mega-cap performance drives alpha as it has done in 2011 we will tend to lag the market. S&P 500 Equal-Weighted Return Minus S&P 500 Market Cap Weighted Return Delta (%) Source: Zephyr

FIRST QUARTER 2012 MARKET OUTLOOK In further review of the impact of the mega-caps on both the S&P 500 and Russell 1000 index returns in 2011, the following chart shows the top ten holdings in the cap-weighted S&P 500. Nine of these holdings are also in the top ten Russell 1000 holdings. Source: Standard and Poors for sector percentages, Thomson for stock returns, Zephyr for sector returns. These top ten mega-cap companies highlighted above make up approximately 20% of the S&P 500 market weight and 18% of the Russell 1000 market weight. An equal weighted portfolio of these ten companies alone would have returned 11.89% in 2011, compared to relatively flat performance for the S&P 500 and Russell 1000 indices. In other words, roughly 70% of the holdings in both the Russell 1000 and S&P 500 underperformed an equally weighted portfolio of the ten holdings above. It should also be noted that the top 10 S&P 500 holdings contained no exposure to the two worst performing sectors in 2011 – Financials and Materials – which were down -18.1% and -9.7% respectively. In 2011 there were generally 3 ways for a long-only large capitalization security manager to outperform: (1) Significantly concentrate the portfolio into the names listed above (or similar mega-caps); (2) Time the market by moving money into and out of cash at just the right windows; (3) Get very, very lucky. Bowling’s process has historically, and by design, not attempted to do 1 or 2, and 3 didn’t happen for us last year. Ironically, the challenge for us in 2011 wasn’t really stock selection, as we actually owned seven of the ten mega caps listed in the table above. The underperformance was driven by our lack of concentration in these names, as we have historically run an equal-weighted portfolio. This structure led us to negative active weightings on stocks that our model was indeed correct about, like Exxon and Apple.

FIRST QUARTER 2012 MARKET OUTLOOK As we have stated before, we want to be adaptive to the constantly changing market environment without tinkering with our proven formula for success. We are firm believers that managers should evolve and lessons should be learned from periods of underperformance. Given the “new normal” environment of increased macroeconomic uncertainties and the likelihood of continued volatility, we have determined that enhancing our risk monitoring procedures will benefit our portfolio construction over time. Several months ago, as you may know, we invested in performance attribution software from Thomson Reuters, which has provided insight into the specific factors and stocks that materially contribute to performance and risk. In addition, we are now actively utilizing risk optimization software from Barra. This tool allows us to disaggregate risk in the portfolio and ensure there are no unintended risk factor tilts in the portfolio. We anticipate that these same tools will assist us in considering an active weight solution within the framework of our commitment to diversified, risk managed exposure. Ultimately, both of these tools will enable us to further enhance our objectivity in the construction of our portfolios, lever our model’s alpha-producing power, control our risk exposures and provide valuable analytic information to investors. Bowling’s long track record demonstrates our ability to work through a wide variety of market environments. Experience has taught us to expect periods of outperformance and underperformance, always striving to deliver consistent portfolio management over full market cycles. We look forward to the dynamic market environment that lay ahead and the opportunity to service our investors. BOWLING PORTFOLIO MANAGEMENT LLC 4030 SMITH ROAD SUITE 140 CINCINNATI, OH 45209 (513) 871-7776 WWW.BOWLINGPM.COM This report is provided for informational purposes only and should not be construed as a recommendation for the purchase or sale of any security nor should it be construed as a recommendation of any investment strategy. There is no guarantee that any opinion, forecast, estimate or objective will be achieved. Certain information has been obtained from sources that we believe to be reliable: however, we do not guarantee the accuracy or completeness of such information. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. 2012 Q1