Download

1 / 22

E N D

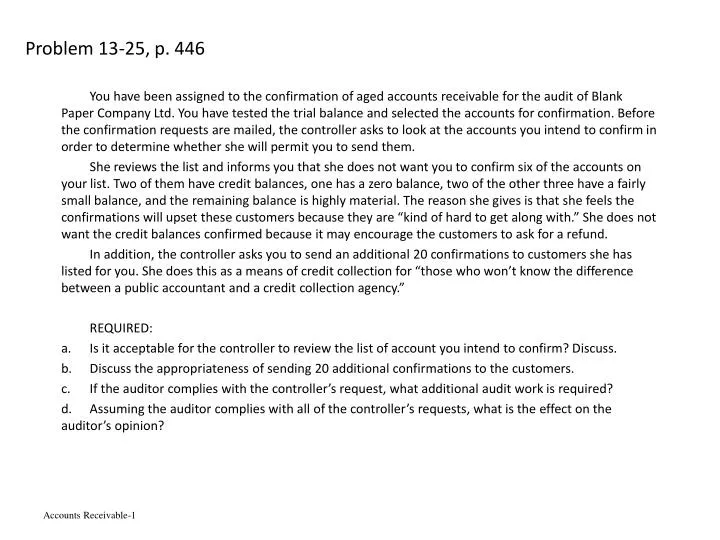

Problem 13-25, p. 446 You have been assigned to the confirmation of aged accounts receivable for the audit of Blank Paper Company Ltd. You have tested the trial balance and selected the accounts for confirmation. Before the confirmation requests are mailed, the controller asks to look at the accounts you intend to confirm in order to determine whether she will permit you to send them. She reviews the list and informs you that she does not want you to confirm six of the accounts on your list. Two of them have credit balances, one has a zero balance, two of the other three have a fairly small balance, and the remaining balance is highly material. The reason she gives is that she feels the confirmations will upset these customers because they are “kind of hard to get along with.” She does not want the credit balances confirmed because it may encourage the customers to ask for a refund. In addition, the controller asks you to send an additional 20 confirmations to customers she has listed for you. She does this as a means of credit collection for “those who won’t know the difference between a public accountant and a credit collection agency.” REQUIRED: • Is it acceptable for the controller to review the list of account you intend to confirm? Discuss. • Discuss the appropriateness of sending 20 additional confirmations to the customers. • If the auditor complies with the controller’s request, what additional audit work is required? • Assuming the auditor complies with all of the controller’s requests, what is the effect on the auditor’s opinion?

13-25 Solution Yes, it is acceptable for the controller to review the list of accounts the auditor intends to confirm. The confirmations will be sent to the company’s customers, and the auditor must be sensitive to the client’s concern with the treatment of their customers. At the same time, if the client refuses permission to confirm receivables, the auditor must consider the reasonableness of the request. The auditor should be willing to perform special procedures that the client requests if the client is in agreement that these procedures may not necessarily be considered within the scope of the auditor’s engagement. In the case of the 20 additional confirmations that the controller requested that the auditor send, the auditor should be willing to send the confirmations; however, these confirmations should not be considered in the evaluation of the results of the accounts receivable confirmation sent by the auditor. It would also be reasonable for the auditor to track the time spent on these confirmations and bill them separately. If the auditor complies with the controller’s request to eliminate six of the accounts from the confirmation, the auditor must perform alternative procedures on the six accounts and decide whether or not this omission is significant to the scope of her examination. If the auditor believes that the impact of omitting these accounts is significant, she must qualify the auditor’s report to indicate the restriction of scope imposed by the client. With respect to the additional 20 confirmations, since these are outside the scope of the audit, the auditor could discuss the extent of the alternative procedures conducted with the client. There may not be any additional procedures conducted, but simply mail the confirmations (unless there are significant disputes or other matters that come to light. Then the auditor must consider their impact upon the accounts receivable balance). If the restriction with respect to not sending the confirmations is material, a qualified or denial of opinion may be needed, if the alternative procedures do not provide satisfactory evidence.

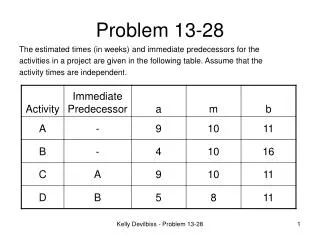

Problem 13-28, p. 447 You intend to use MUS as a part of the audit of several accounts for Roynpower Manufacturing Inc. You have done the audit for the past several years, and there has rarely been an adjusting entry of any kind. Your audit tests of all tests of controls for the transaction cycles were completed at an interim date, and control risk has been assessed as low. You therefore decide to use an ARIA of 10 percent for all tests of details of balances. You intend to use MUS in the audit of three of the most material asset balances: accounts receivable, inventory, and marketable securities. You feel justified in using the same ARIA for each audit area because of the low assessed control risk. The recorded balances and related information for the three accounts are as follows: Net earnings before taxes for Roynpower are $2,000,000. You decide that materiality will be $100,000 for the client

The audit approach will be to determine the total sample size needed for all three accounts. A sample will be selected from all $10 million, and the appropriate testing for a sample item will depend on whether the item is a receivable, inventory, or marketable security. The audit conclusions will pertain to the entire $10 million, and no conclusion will be made about the three individual accounts unless significant misstatements are found in the sample. REQUIRED • Evaluate the audit approach of testing all three account balances in one sample. • Calculate the required sample size for each of the three accounts assuming you decide that the tolerable misstatement in each account is $100,000. (Recall that tolerable misstatement equals preliminary judgement about materiality for MUS.) • How would you identify which sample item in the population to the audit for the number 4,627,817? What audit procedures would you perform? • Assume you select a sample of 100 sample items for testing and you find one misstatement in inventory. The recorded value is $987.12, and the audit value is $887.12. Calculate the misstatement bounds for the three combined accounts, and reach the appropriate audit conclusions. What are the factors to be used in this problem? Estimated Population Exception Rate (EPER) = 0.00 ( as there has rarely been an adjusting entry of any kind.) The acceptable risk of incorrect acceptance (ARIA) is equivalent to ARACR = 10% Tolerable Misstatement for A/R = 100,000/3,600,000 = 0.028, or close to 3% Tolerable Misstatement for Inv. = 100,000/4,800,000 = 0.021, or close to 2% Tolerable Misstatement for M.S. = 100,000/1,600,000 = 0,063 or close to 6%

Some Key Terms for Testing Balances Estimated Population Error Expected Population Error Rate • A judgmental estimate based on knowledge of client. • Used to determine appropriate sample size. • Low Error => low sample size • As Expected Error approaches Tolerable misstatement, more precision is needed and larger sample size is needed. Acceptable Risk of Incorrect Acceptance • ARIA • The risk that the auditor is willing to take of accepting a balance as correct when the true misstatement is greater than the tolerable misstatement. • In other words it could be materially misstated • ARIA is equivalent to ARACR • ARACR is the risk the auditor is willing to take of accepting a control as effective (or monetary amount as tolerable) when the true population exception rate is greater than TER. • Again, materially misstated • ARIA is inversely related to sample size Tolerable Misstatement • TER on the tables • The misstatement that the auditor will permit in the population before concluding that the balance is materially misstated. • Result of auditor judgment.

TER INV A/R MS

Solution 13-28 • The audit approach of testing all three account balances is acceptable. This approach is also desirable when the following conditions are present: • The auditor can obtain valid, reliable information to perform the required tests in all of the areas. • Internal control for each of the three areas is comparable. • Misstatements are expected to occur evenly over the entire population. For instance, the auditor does not expect a large number of misstatements in accounts receivable and very few, if any, in inventory. • The required sample sizes if each account is tested separately are: • The population would be arranged so that all accounts receivable would be first, followed by inventory and marketable securities. The items would be identified by the cumulative totals. In the example, the number 4,627,871 would relate to an inventory item since it is between the cumulative totals of $3,600,000 and $8,400,000. Accordingly, for this number the inventory audit procedures would be performed. • The misstatement data are as follows: Now need to extend the misstatement to the population. Do this by calculating the Upper and Lower bounds, not a point estimate. If the both the lower and upper misstatement bound fall below the overstatement and understatement tolerable misstatement amounts, accept the conclusion that the book value is not misstated by a material amount. Otherwise conclude that the book value may be misstated by a material amount.

Generalizing Misstatements to the Population • The auditor wants to determine the maximum amount of overstatements and understatements • While still providing a sample with no misstatements • In other words, the auditor did not miss any misstatements in the sample • These are the upper misstatement bound and the lower misstatement bound • Use the Upper & Lower Misstatement Limits tables for 5% or 10% ARIA and the number of misstatements • In this example there is one misstatement and the sample size is 114 • From the table at an ARIA of 10% • The percentage is between 3.8% (Note for future 2.3 + 1.4 = 3.8) and 3.2% (1.9 + 1.3) • See next slide for the calculation. Calculated percentage = 3.38% • This percentage represents both upper and lower bounds as a percentage • Based on this: • At a 10% sampling risk, there are no more than 3.38% of the dollar units in the population that are misstated. • The auditor must make anassumption about the average percent of misstatement for population dollars that contain a misstatement, but which the auditor has not examined. • i.e. what is the average misstatement rate for those items that contain a misstatement • This called the Percent of Misstatement Assumption, see Slide 46 • In our example the misstatement rate for one misstatement in 10.1% - see previous page. • The auditor is trying to estimate it for those misstatements not found. • This estimate significantly affects the misstatement bounds

Generalizing from the Sample to the Population • Calculating Misstatement Percentage • Sample size for inventory was 114 • Actual number of deviations was 1 • ARACR is 10% • From table Misstatement Percentage = between 3.8 an 3.2 • Sample size of 100 = % of 3.8 • Sample size of 120 = % of 3.2 • Thus a sample size of 114: • 100 = 3.8 • 114 = x • 120 = 3.2 • Thus (114 – 100)/(120 – 100) = (x – 3.8)/3.2 – 3.8 • x = 3.38 • This percentage can be used in calculating the upper and lower bounds (i.e. $ balances) • But note in our example, Part d, we are using a sample size of 100. Thus we will use 3.8%

Appropriate Percent of Misstatement Assumption • This is an auditor decision • Based on judgment • Most auditors assume that it is desirable to assume 100% for both overstatements and understatements • Highly conservative • N.B. using MUS, upper and lower misstatement bounds are used rather than maximum likely misstatement attached to a confidence level. • In other words, the misstatement is likely somewhere in between the max and the min • The following example uses 50% instead of 100% • What this means is that for those items the auditor has not examined and have a misstatement, it is assumed that they are misstated 50% • The single overstatement percentage amount for this problem is 10.1% as calculated below. Thus 50% is conservative.

Note that there may be both overstatements and understatements in the population. Thus the following tables look at the Precision Limits for both over and understatements. Also remember that there was only one misstatement found, and this was an overstatement. Also remember in this example the auditor makes the assumption that the average percent of misstatement for population dollars that contain a misstatement is a 50% misstatement unit error. These will be items that the auditor has not examined.

There must be adjustments made to the over and understatement bounds because an understatement offsets and over statement, and vice-versa Thus the likely misstatement is between $105,000 and $130,050. Since materiality is $100,000, more work needs to be done

Another example • Assume that there are the following misstatements:

Note in the following table, the conservative approach is to associate the lowest misstatement limit (2) portion with the highest misstatement unit error (4) .The amount of error is thus maximized Overstatements * * These amounts come from the previous slide. Only overstatements.

Offsetting Adjustments Thus the likely misstatement is between $116,900 and 117,570. Since materiality is $100,000, more work needs to be performed.

Problem 13-19, p. 443 During his interim audit visit, Charles Ai determined that one of the subsidiary companies of Mega Big Limited had experienced some very serious problems with respect to the credit management and collection of trade accounts receivable. During the first six months of the year, the accounts receivable of this subsidiary had almost doubled, the number of days’ sales in accounts receivable had increased from 39 to 64 days, and bad-debt expense had risen sharply. REQUIRED Prepare an outline of the steps that should be taken to investigate the nature and causes of the credit and collection problems. (Do not consider the possibility of fraud.)

Investigation of credit and collection problems • Obtain: • aged accounts receivable trial balances (current date) • analysis of bad-debt expenses • analysis of doubtful accounts • Ascertain policies in force. • Obtain explanations from credit manager for unfavourable results. • Consider the following factors: • economic situation • effect of competition • sales policies • Identify variances in policies and procedures between subsidiary and parent company. • Method of granting credit: Is there an acceptable credit granting system? • outside sources (such as trade credit agencies) • internal sourcespayment history • credit limits established • Follow-up on collections: Is there an adequate system for follow-up? • invoices and statements mailed promptly • aged list of accounts reviewed and old accounts contacted by reminders, advices, correspondence, etc. • Are records up-to-date? • Check compliance with procedures. • Have there been changes? • Review status of overdue accounts per aged list of accounts and ascertain whether proper action has been taken. • follow-up by credit manager • approval of credit on specific sales • credit limit exceededshould be cut off • explanation of delays in payment • perform similar analysis of accounts written off as to causes, by checking original credit approval and follow-up. • Determine that current allowance is adequate by reviewing collectibility of overdue accounts.