Download

1 / 22

400 likes | 870 Views

Chapter Two. Financial System. Chapter Outline. Financial System and Functions Basic Puzzles about Financial Structure Asymmetric Information Problem Why different interest rates on bond? The term Structure of Interest rate Market Indexes for stocks Inflation and Real rate of return.

E N D

Chapter Two Financial System

Chapter Outline • Financial System and Functions • Basic Puzzles about Financial Structure • Asymmetric Information Problem • Why different interest rates on bond? • The term Structure of Interest rate • Market Indexes for stocks • Inflation and Real rate of return

I- The Financial System • Includes: • Financial Markets: • Derivatives • Capital : - Debt (Money & Bonds) - Stocks • Exchange Rate • Financial Intermediaries: • Commercial Banks • Investment banks : mergers acquisition • Insurance companies • Pensions, Retirement and Mutual funds • Venture Capital Firms • Information Services : Moody’s &(S&P 500)

The Financial System • Financial infrastructure • Regulation • Government and Quasi Governmental Organization

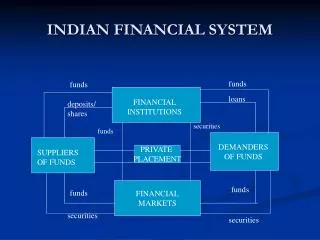

The Main Functions of Financial System 1-Transferring Resources Across Time and Space Stock & Bond Direct financing Markets Individual Firms Government Individual Firms Government Banks buys stocks Banks issue stocks Surplus Units Deficit Units National & International National & International Intermediaries Indirect financing The Flow of Funds Diagram

The Functions of Financial System • Managing Risk • Clearing and settling Payments efficiently • Subdividing Shares (financing firms ) • Providing Information: • Dealing with asymmetric information • Definition: One party has no sufficient information about the other party • Two types : • Adverse selection (before signing the contract). Lemon prevail • Moral hazard (after signing the contract) • The principal - agent problem • Herd instinct, snowball effect, financial crises

II-Basic Puzzles about Financial Structure Financing Business in USA • Stocks and debt are not the most important source of external financing for business. • Indirect finance ( Banks) are the most important • Why companies relay mainly on indirect financing?

Explanation of the puzzles • Problems facing the direct financing • 1- Transaction costs • 2- Asymmetric Information: • Adverse selection: • Potential bad credit risks are the ones who most active seeking funds. The lender may refuse to lend. • Moral hazard • You may playing with someone else’s money • Indirect financing provide solutions

How Adverse selection influence Financial Structure • Example 1 Cars: The Lemons Problem • Used cars market. Volvo S60 (2010). • Two Qualities Good Bad (Lemon) Buyers willing • Price 150 000 50 000 100 000 • Only the sellers know the quality • The seller of bad has incentive to make his care look like a good one. • The buyers will discover that • Likely that used care market will not work • Solutions: • The buyers should know as much about the quality of used cars as the seller: • Subscribe in consumer report • Mechanic to evaluate the particular car • Buy from a dealer so asymmetric information is eliminated.

How Adverse selection influence Financial Structure? • Example 2 : Stocks. • Example 3: Bonds • Solutions • Private production and sales of information • S & P, Moody’s • Doesn’t eliminate asymmetricbecause of the Free-Rider. • Government Regulation: • Politically difficult to refer to bad firms. • Regulation instead • Still bad firms have incentives to look like good firms • Doesn’t eliminate asymmetric information • 3- Financial Intermediaries • Financial intermediaries function as a car dealer:

How Moral Hazard influence Financial Structure? • A- Moral Hazard in Equity Contracts • Example : You build a factory with Mr. X who is the manager. • The Principal-Agent problem • The separation involve moral hazard (manager act in their own interest) • Tools to solve the Principal-Agent problem: • 1- Monitoring: • but expensive in time and money • 2- Government regulation: lows for standard accounting • 3- Financial intermediation : Venture capital firms:

How Moral Hazard influence Financial Structure? • B- Moral Hazard in Debt Contracts • The borrower can undertake riskier projectand the lender may lose all his money. • Because of the moral hazard the lender may not make the loan • Tools to Reduce moral hazard in debt contracts • 1- Net worth) : • 2- Monitoring • 3- Enforcement of restrictive covenants (skriftligtavtal) • 4- Financial Intermediation:

III- Financial Markets Rates • Why different interest rates on bonds? • Because different: • Unit of account • Maturity • Default risk • Taxes • Liquidity • Effect of Unit of account • What is risk free in one currency is not in another. • ExampleiSEK= 3%, i$ = 9% E=10 SEK/$. You have 10000 SEK to invest for one year. • Two investment strategies: • Invest in SEK:10000kr (1.03)=10300 =300kr (3%) • Invest in $: 1000$(1.09) = 1090$ (10900kr) = 900 kr(9%) • But, if $ depreciate to 8 SEK/$ • R$= $1090 x 8 = 8720 Rate of return = -12.8%

Managing Exchange Rate exposures • Covered Interest Parity (CIP) • A risk averse investor is indifferent between placing an extra 1kr into home or foreign treasury bill when returns on them are equal: • or • Given any 3 variables, we can solve for the fourth:

Financial Markets Rates • Effect of maturity • Yield Curve . • The slope could be negative, positive or constant • Three theories? • 1- Expectation theory (Förväntningshypotesen ): • The long interest rate is the average of short and future short interest rates. • Perfect substitute therefore the curve should be constant . • Ex. The one-year interest rate over the next five years is expected to be: 5%, 6%, 7%,8% and 9%. What are the interest rates on : a two-year bond, a three-year bond, a four-year bond and a five-year bond? What is happening to the yield curve. • it= Year 1 interest rate = 5%, - iet+1= Year 2 interest rate = 6%, • iet+2 = Year 3 interest rate = 7%, - iet+3 = Year 4 interest rate = 8%, iet+4 = Year 5 interest rate = 9%, int= The long term interest rate

Financial Markets Rates • The interest on the two-year bond: • The interest on the three-year bond: • The interest on the four-year bond: • The interest on the five-year bond : • Yield curve should be constant . • If in reality • Positive the short would rise. • Negative the short will fall. • The theory cannot explain: why the yield curve is positive often.

Financial Markets Rates • 2-Segmented market theory (marknadssegmenteringsteorin) • No substitutions • Positive, negative, or constant • 3- Liquidity preference theory (Likviditetspreferensteorin) • There is substitute but it is not perfect • Most investors would prefer short, therefore they should be offered higher rate of return for long term.

Exempel- Liquidity preference theory • Ex: The one-year interest rate over the next five years is expected to be: 5%, 6%, 7%, 8% and 9%. Investors’ preferences for holding short-term bonds have the liquidity premium for one-year to five-year bonds as 0%, 0.25%, 0.5%, 0.75%, and 1%, respectively. What are the interest rates on : a two-year bond, a three-year bond, a four-year bond and a five-year bond? What is happening to the yield curve. • The interest on the two-year bond : • The interest on the three-year bond : • The interest on the four-year bond:

Market Indexes For Stocks • Two major indexes: • Dow Jones Index (major 30 stocks in US) • Ex: With only 2 stocks • S & P 500 = 0.8 * 0.5 + 0.2 * 2.2 = 84 • Weight : • IBM = 20Bil/25bil • DEC: 5bil/25bil

Inflation and Real rate of return • Calculating the real rate of return: • 1- Fisher equation: • i= r + nominal return • or r = i - Approximationof real return • 2- : 1+ r= (1+ i) / (1+) or r = (I - )/(1+ ) exact • Ex1: Amount = 100, i = 8% and = 5%, calculate real rate of return for 1year. • Approximately 100(0.08-.05) = 3kr or 3%. • Exact : 1+ r = (1.08)/(1.05) = 1,02857. Then r = 1,02857 -1= 0.02857 or 2.857% • Note that what is risk free in nominal is not in real.

Example of Real and Nominal Return • Calculation of Real Return: • 1- Approximation: • Fisher equation • 2- Exact • 1+ r = (1+ i) / (1+)= = 1.10/1.05 =1,0476 • 3- or