Download

1 / 62

640 likes | 1.26k Views

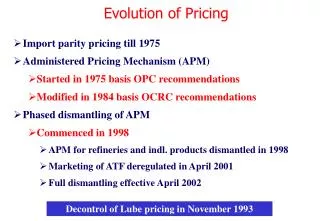

ADMINISTERED PRICING MECHANISM FOR PETROLEUM PRODUCTS. OBJECTIVES. Understand the evolution and fundamentals of Administered Pricing Mechanism. Familiarise with the current pricing structures for products. PRICING FUNDAMENTALS HISTORY AND BACKGROUND. Pricing fundamentals .

E N D

ADMINISTERED PRICING MECHANISM FOR PETROLEUM PRODUCTS

OBJECTIVES • Understand the evolution and fundamentals of Administered Pricing Mechanism. • Familiarise with the current pricing structures for products

PRICING FUNDAMENTALS • HISTORY AND BACKGROUND

Pricing fundamentals • History: Till Mid 50s • Products imported by Shell, Stanvac & Caltex • From Principals • No control • Prices based on US/Gulf port prices plus transportation, insurance etc.

Pricing fundamentals • History Mid 50s - Mid 60s • Refineries - Shell, Esso & Caltex • Refineries compensated on import parity • Import parity based on landed cost, transportation & local taxes ex-MI to up country depots • Distribution favoured Metros, Coastal areas

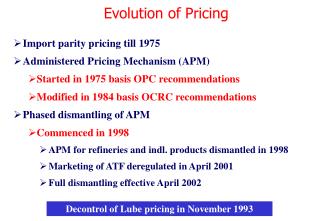

Pricing fundamentals • History: OPEC (Damle) Report w.e.f Oct 1st,1961 • WGOP (Talukdar) Report w.e.f Feb 1st,1966 • Kept inland refineries on import parity • looked into and recommended down stream recoveries • Net back for indigenously produced product will not be higher than import and if any better terms are offered this would apply to foreign companies also.

Pricing fundamentals • History: OPC (Shah) Report - Early 70s w.e.f Jun 1st,1970 • Equalised ex refinery prices by transplanting port prices/ port refinery prices on inland refinery prices • The revision in the prices of finished products should be linked to the variation in the cost of crude. • Rationalised FSP and C&F surcharges

Pricing fundamentals • Cartel Formation- OPEC • The oil producing countries formed a cartel known as Organisation of Petroleum Exporting countries. • The members are Iran, Iraq, Kuwait, Saudi Arabia, Qatar, U.A.E, Venezuala, Nigeria, Indonesia, Algeria, Libya, Ecuador, Gabon

Pricing fundamentals • History Mid 70s • OPC(Dr.S.Krishnaswamy) w.e.f 14.7.75 • Govt takes over the entire industry. • Esso, Shell, Caltex& Boc leave • Import parity no longer mandatory • Cost plus becomes the basis of pricing

Pricing fundamentals • APM-OPC • All Refineries Primary Pricing Points • Standard production pattern is the basis • Ex Refinery prices fixed on weighted average price of crude • Deviations in pooled price of crude adjusted in COPE • COPE compensated through C&F surcharge

Pricing fundamentals • APM -OCRC w.e.f 1.4.84 • All Refineries Primary Pricing Points • Secondary Pricing Points at Ports & Pipeline Tap off points • COPE for adjusting the pooled FOB cost and the actual cost of crude import • C&F surcharge for adjusting adjusting product import cost & incidentals • FSP Surcharge for movements • PPA for cross subsidy & price adjustments • 12% post tax returns on networth

ADMINISTERED PRICING MECHANISM PRICING FUNDAMENTALS FOR PERIOD BEFORE APRIL 1998

APM : Pricing fundamentals • Oil Price Committee : Nov 1976 • Recommended the Retention Price Mechanism vs Import Parity prevailing then • Oil Cost review Committee: July 1984 • Recommended continuation of Retention Price Mechanism with updations and minor modifications.

APM : Determination of Ceiling Selling Prices • The following are the stages: • Fixation of retention price per MT of crude throughput for each refinery. • Determination of standard throughput, product pattern and fuel & loss for each refinery. • Allocation of total cost of production of a refinery to individual products. • Determination of ex-refinery transfer price. • Fixation of ceiling selling price.

APM : Fixation of retention price per MT of crude throughput for each refinery • The following are the stages: • Delivered cost of crude oil • Standard refining cost • Return on investment

Delivered cost of crude oil • Comprised FOB, freight, insurance, wharfage, duties for imported crude oil. • Indigenous crude oil prices fixed by Govt. • Weighted average pooled FOB cost based on indigenous and imported crude worked out , uniform for all oil companies. • Other elements, viz., freight, insurance, ocean loss, wharfage, landing charges, duty etc rates fixed for each refinery. • Variations in actual FOB/other elements adjusted in pool account.

Standard Refining Cost • Fixed for each refinery considering actual expenditure in past and adjusted for cost escalations in future. • Specific to refineries based on plant design, investment, secondary processing facilities etc. • Expenditure on bad debts, loss on sale of assets/stores, interest, bonus etc inadmissible. • Increase in refining cost compensated only for major variations like LTA, variation in rates of chemicals, utilities etc.

Return on Investment • ROI was provided under Networth concept. • Gross capital employed comprising Net Fixed Assets and Normative Working Capital was apportioned between Networth and Borrowings based on individual company. • NFA based on value after depreciation. • Normative Working Capital • Cost of 45 days crude throughput for imported crude and 35 days for indigenous crude on pooled FOB cost • Networth:12%post tax return • Borrowing:interest based on average borrowing rate of company.

APM : Determination of Standard Throughput, product pattern and fuel and loss for each refinery • Fixed considering crude availability, secondary processing facilities and other technical factors. • Determination was important since refinery got full compensation for cost at this level of throughput and production.

APM : Allocation of total cost of production to individual products: retention price of products. • Set of indices developed keeping index of SKO as 1. • Indices based on supply/demand position of products, international prices and to discourage production of surplus products.

APM : Determination of Ex-refinery Price • Ex-Refinery Price is price at which products to be transferred to marketing companies. • Ex-Refinery prices based on weighted average of retention prices of various formula products plus a constant amount to meet under-recoveries on freight/transportation. • Difference between ex-refinery price and Retention price required to be surrendered/claimed from the pool.

APM : Determination of Transfer Price • For Non-Formula products, Govt fixed Transfer Price . • Difference between transfer price and Retention price adjusted in pool accounts. • For Speciality products requiring further processing, transfer price of the feed was fixed by the Govt.

APM : Determination of Ceiling Selling Price • Ceiling Selling Price. • Ex-Refinery price. • Marketing Margin. • C&F Surcharge • Freight Surcharge • Excise Duty. • Dealers’ Commission etc.

ADMINISTERED PRICING MECHANISM PRICING FUNDAMENTALS FOR PERIOD AFTER APRIL 1998

ADMINISTERED PRICING MECHANISM PRICING OF INDIGENOUS CRUDE OIL

APM : Pricing of indigenous Crude Oil • Refineries required to procure imported crude at actual prices: No adjustment with pool accounts. • Compensation for indigenous crude manufacturers fixed by OCC every month as a percentage of actual FOB cost of imports. • 1998-1999 75% 1999-2000 77.5% • 2000-2001 80% 200102002 82.5% • Currently 82.5% with a cap of Rs. 5570/MT

APM : Pricing of indigenous Crude Oil • Import parity cost of indigenous crude oil fixed by OCC every month. • For Product Sharing Contract (PSC) operators, price payable is FOB cost, freight, insurance, port charges, customs duty etc. • For PSU oil producers, compensation is at 82.5% of the import parity cost of the indigenous crude oil , based on FOB cost computed by IOC IT on the basis of bench mark crude Bonny Light and Escrovos following Gross Product Worth Method(GPW)

APM : Pricing of import parity cost of indigenous Crude Oil under GPW method • Landed cost of product yield of the crude is compared with that of benchmark crude and discount/premium equal to difference in product value is applied to FOB cost of benchmark crude to arrive at FOB cost of indigenous crude. • FOB cost of bench mark crude as per Platts for previous month.

APM : Pricing of import parity cost of indigenous Crude Oil under GPW method • Landed cost of product calculated as under: • FOB as per Platts for previous month. • Ocean freight: WS/AFRA for max size of vessel for West and East Coast separately. • Wharfage and landing charges. • Ocean Loss as per actual on crude imports during last Qr. • Marine Insurance: Same as above. • Customs Duty at applicable rates.

APM: Computation of Tariff Adjusted Import Parity Prices(TAIPP) • Till July 1999, TAIPP common for all refineries was based on average cost of actual imports. During second preceding month. • Since July 1999, TAIPP for each refinery is calculated based on notional landed cost of imports at the nearest port consisting of: • FOB:Average FOB as per Platts and Premium/Discount as per Argus for previous month.Adjustment for quality for MS, HSD. • Freight to the port based on WS/AFRA. • Insurance as per policy

APM: Computation of Tariff Adjusted Import Parity Prices(TAIPP) • Notional landed cost of imports at the nearest port consisting of (Continued) • Landing Charges: Port charges at port,. In case of Private ports, lower of rates applicable to port and the nearest govt port taken. • Ocean loss: Based on actuals for previous year. • Customs duty : as per tariff.

Tariff Adjusted Import Parity TAIPP) SAMPLE CALCULATION FOR HSD • C&F prices(Average for previous month) $ 201 • Insurance $/MT 0.11 • CIF value Rs/MT 9442 • Landing charges Rs/MT 35 • Customs duty @20% 1896 • Ocean loss 0.3% Rs/MT 28 • TAIPP Rs/MT 11401

APM: Computation of Ex-Refinery Gate Price(RGP) • Ex Refinery Gate Price (RGP) • Tariff Adjusted Import Parity Price (TAIPP) • Minus Surcharge to adjust for difference between import parity cost of indigenous crude and price payable for indigenous crude. • Minus Adjustment factor for refineries prior to 1.2.98 @ 0.1% of TAIPP considering depressed international refining margins.

APM: Computation of Surcharge element. • Indigenous crude cost differential • Indigenous crude producers are paid 82.5% of average FOB of imported crude with a cap of Rs. 5570/MT. • Refineries are to bear import parity cost of indigenous crude . • The difference between import parity cost of indigenous crude and price paid to oil producers is recovered by pool from refineries as surcharge.

APM: Computation of Surcharge element. • Pipeline freight • Even after de-regulation P/L continues under APM. Since inland transportation is not charged in prices,refineries are not required to bear this and transportation cost on crude is paid to P/L by OCC. • The transportation cost on crude processed for production of decontrolled products is recovered from refineries.

APM: Computation of Surcharge element. • Return on working capital on inventory of crude oil in P/L • Return of 12% post tax on cost of crude inventory in P/L proportionate to the production of controlled products.

APM: Computation of Surcharge element. • Sales Tax on indigenous crude • Since refineries are to bear import parity cost and no sales tax on imported crude, sales tax paid by refineries on indigenous crude oil reimbursed through surcharge.

Surcharge working for controlled products: Sample Calculations for Koyali • Differential for indigenous crude • Import parity price of ind.crude (Rs/MT) 8348 • Prices to be paid for ind.crude suppliers 5570 • Amount to be recovered from refineries 2778 • Quantity of indigenous crude TMT 1000 • Total amount to be recovered Rs.Crores 278 • Sales tax paid on ind.crude Rs/Cr - 4 • P/L freight on crude for decontrolled prod 3 • WC return on crude inv in P/L of cont.prod - 4 • Total amount of surcharge Rs.cr 273

Surcharge working for controlled products: Sample Calculations for Koyali • Despatches of controlled products TMT 429 • Surcharge Rs/MT 6365

Ex-Refinery Gate PriceSAMPLE CALCULATION FOR KOYALI: SKO • TAIPP Rs/MT 11401 • Less Surcharge 6365 • Less Adjustment factor (0.1%) 11 • Ex-Refinery Gate Price Rs/Mt 5025

APM: Computation of Ex-Storage Point Prices • Ex-Storage Point price at PPP consists of the elements fixed by MOP&NG reviewed monthly • Tariff Adjusted Import Parity Price(TAIPP) • C&F surcharge for adjusting product import cost & incidentals • FSP Surcharge for movements • PPA for cross subsidy & price adjustments • Marketing Margin

APM: Pricing basis • Other Elements • State Surcharge • Excise duty • Freight • Sales Tax & other local levies

APM: Pricing basis • APM - Margins • Operating expenses subject to review by OCRC (Oil Industry Cost Review Committee) • Margins to be recovered via RTP (Refinery Transfer Price) or selling price, as relevant • For marketing the common cost elements are installation, administration, distribution

PRICING OF MS/HSD BASIC PRINCIPLES

Pricing Structure of APM products: MS & HSD • Ex-Storage Point Price RS PER KL MS HSD • TAIPP : 9565.96 10851.07 • MKTG MGN 239.20 195.91 • C&F S/C 948.00 838.00 • FSP S/C 351.00 344.00 • PPA 7894.85 (294.38) • EX ST. PRICE 18999.01 11934.60

Pricing Elements in APM for MS & HSD • Elements and principles • Ex-storage point price • State surcharge • Siding charges • PL charges • Railway freight • RPO Surcharge(MS:60, HSD:20) Fixed by OCC to accommodate dealer comm and investment on facilities, only for retail • RPO charge(MS:4.36,HSD:0.27) Fixed by OCC to finance local delivery chgs

Pricing Elements in APM for MS & HSD • Elements and principles • Assessable value • Add Excise duty amount @16%for MS,12%for HSD • Add additional excise duty of Rs. 1000/KL • Less RPO S/C & Charge • Net depot price • Add excisable portion of RPO charges (MS:4.36,HSD:0.27) • Add non-excisable portion of RPO charges~FDZ charges(MS:44,HSD : 44)

Pricing Elements in APM for MS & HSD • Elements and principles • Add road bridging charges • Depot Shrinkage allowance • Delivery charges beyond FDZ MS@Re.0. 67/KL/KM, HSD@ Re.0.67/KL/KM • Entry Tax • Octroi at Depot • Toll,Goods,Transit Tax • Octroi at destination • Net RPO Price for consumer

Pricing Elements in APM for MS &HSD • Elements and principles • Central Sales Tax • Sales Tax • Surcharge on Sales Tax • Cess • Selling Price for consumer • Dealers’ Commission:(MS:402, HSD:251) • Retail Selling Price

LPG PRICING DOMESTIC PACKED CYLINDERS