Download

1 / 38

380 likes | 387 Views

Boom-Bust Cycles and The US Housing Market. From the Perspective of the Austrian School Will Geary. Austrian School of Economics. School of economic thought that espouses free markets and laissez-faire capitalism

E N D

Boom-Bust Cycles and The US Housing Market • From the Perspective of the Austrian School • Will Geary

Austrian School of Economics • School of economic thought that espouses free markets and laissez-faire capitalism • Early founders include economists Carl Menger, Ludwig von Mises, and Nobel laureate Friedrich Hayek • Later proponents include Murray Rothbard and presidential candidate Ron Paul

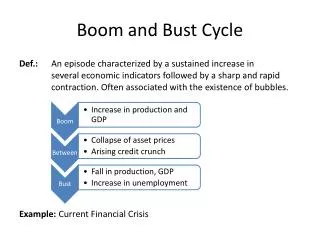

Austrian Business Cycle Theory High Interest Rates Low Interest Rates Discourage borrowing Contraction of credit Contraction of money supply Stimulate borrowing Expansion of credit Expansion of money supply

Austrian Business Cycle Theory • Interest rate and the availability of credit impacts producer and consumer expectations about the future • Lower interest rates encourage firms to borrow the newly expanded bank money and invest it in future projects • Lower interest rates encourage consumers to take out loans and purchase things they other wise might not be able to (houses, cars, etc)

Austrian Business Cycle Theory • Easier borrowing can lead to rapid expansion, spending and investment, i.e. a “bubble” • Remember, this bubble is artificial. The rapid growth is not due to increased productivity, but an expanded credit supply

Austrian Business Cycle Theory • For a period of time, things look good • Incomes rise, business are able to acquire capital and people are able to live above their means • However, the boom turns out to be unsustainable and eventually crashes

Austrian Business Cycle Theory • The Fed eventually realizes the bubble it has created and raises interest rate to curb its growth • People begin demanding their money back from banks, individuals default on their loans, lenders slow or even stop lending, and companies go bankrupt due to a lack of capital to finance previous bad investments • This is known as a “credit crunch”

Austrian Business Cycle Theory • In response to the bubble bursting, the credit crunch and the resulting recession, the Fed lowers interest rates to expand the credit supply and encourage borrowing • Remember: this cycle began with artificially low interest rates in the first place!

Austrian Business Cycle Theory Lower Interest Rates Recession Cheap Credit Credit Crunch Distorted Expectations Bubble Bursts Overexpansion & Malinvestment Raise interest rates to slow bubble Bubble Created This system will last only as long as the Fed is able to keep lowing the interest rate, which is currently at an all-time low of 0.25%!

Austrian Business Cycle Theory Natural Interest Rates (blue) = what interest rates theoretically should be, or would be if it weren’t for the Fed Market Interest Rates (red) = what interest rates actually are in the presence of the fed

Austrian Business Cycle Theory 10 Year Gov’t Security Interest Rates - Federal Funds Effective Rates Source: research.stlouisfed.org Positive blue line = Fed has set interest rates lower than they would/should be Negative blue line = Fed has set interes rates higher than they would/should be Gray bars represent recessions

Dot-Com Bubble • A period from 1995-2000 of mass speculation and over-investment in the blossoming Internet sector • Website based startups were able to acquire lots of investor capital due to the novelty of the ‘dot-com’ concept and a low interest rate in 1994 of 2.96%

Dot-Com Bubble Source: econstats.com NASDAQ peaked on March 10, 2000, at a record high price of 5,048.62

Dot-Com Bubble • The Fed was aware of the rapidly expanding tech bubble before it burst • In January 2000, the Fed increased the federal funds rate from just under 3% to 6.5% in hopes of curbing its growth • Collapse begins in March 2000

Dot-Com Bubble • Stock market crash from 2000-2002 • Total depreciation in market value of Nasdaq stocks estimated at $5 Trillion • Nasdaq bottoms out at 1,270 in March 2003, down from 5,048 three years earlier Aftermath:

Dot-Com Bubble The Fed’s Response: • 11 successive interest rate cuts • From 6.5% in Jan 2000 1.75% by 2004 • This is a new all-time low federal funds rate • This seemed to be an effect response, given that the recession was much milder than analysts had expected

Perhaps some of the pain of the dot-com bubble collapse was simply rolled-over into the housing bubble?

Housing Bubble • A period from 2001-2006 during which US housing prices skyrocketed, until crashing in in July 2006 • Prompted by historically low interest rates that were intended to ease the blow of the tech bubble crash in 2000

Housing Bubble • Low interest rates mean more borrowing, more spending and less saving • This manifests itself in a higher demand for housing and rising home prices • Exacerbating things, homeowners tend to feel and act wealthier when the value of their homes increases

Housing Bubble • Household debt grew from $705 billion in 1974 (60% of disposable income) to $14.5 trillion in 2008 (134% of disposable income) • In 2008, the average household owned 13 credit cards, 40% of which carried a balance -- up from 6% in 1970 • National mortgage debt grew from 46% of real GPD during the 1990s to 73% in 2007

Housing Bubble %YoY Change in Case-Schiller HPI vs Federal Funds Rate

Housing Bubble • Exacerbated by an increase in risky lending • Subprime mortgages = mortgages for those with low credit scores (<640 FICO score) • Many believe that these risky loans, and the lenders who utilized them, are to blame • However -- risky loans are not the root of the problem but an explainable result

Housing Bubble • Artificially low interest rates create a price distortion that leads to a false sense of security and a higher appetite for risk • Since home prices are skyrocketing, bankers could always count on selling off homes for a profit if their risky subprime loans were to default

Housing Bubble • Eventually, the Fed realizes the bubble it has created and wants to slow it down • In 2006, Fed raises interest rates from 1% to over 5.25% • Result: credit contraction, loans and capital no longer as easily available, people start defaulting on mortgages, etc

Housing Bubble • In July 2006, Subprime mortgage industry collapses • Over 25 subprime lending agencies go bankrupt • High foreclosure rates and plummeting home prices • Investment banks that made huge bets on subprime industry (Lehman, Bear Stearns) are hit hard

Recap Federal Funds Rate Fed hikes up interest rates 6.5% Fed hikes up interest rates 5.25 Dot-Com Bubble Bubble bursts, subprime industry collapses Stock market crash and recession 2.96 ? Housing Bubble 1.0% Fed slashes interest rates 1994 2000 2004 2006

Current Financial Crisis • Three large investment banks fail: Lehman Brothers, Bear Stearns, Merrill Lynch • Each bank had placed a lot of confidence in the housing market and related financial products, such as mortgage-backed securities (MBS) and credit default swaps (CDS)

Current Financial Crisis • How does the Fed respond to the crisis? • Cuts federal funds rate from 5.25% in 2006 to 2% in April 2008, and again to an all time low of 0.25% in December 2008 • Injects almost $1 trillion as a ‘stimulus’ • Prints additional $600 billion to purchase bad mortgage backed securities from Fannie Mae and Freddie Mac

Current Financial Crisis Federal Funds Rate Fed hikes up interest rates 6.5% Fed hikes up interest rates 5.25 Dot-Com Bubble Stock market crash and recession Bubble bursts, subprime industry collapses ? 2.96 ? Housing Bubble Recession 1.0% Fed slashes interest rates 0.25 1994 2000 2004 2006 2008 2010

What Next? • I think the Fed is currently in the process of creating the next bubble, with the FFR still at an all-time low of 0.25% • I predict the bubble will manifest itself in ‘green,’ eco-friendly stocks, i.e. renewable energy • What will the Fed do when this bubble bursts and interest rates are at zero (i.e. can’t be cut any lower)?

Works Cited • Bocutoglu, Ersan, and Aykut Ekinci. "Austrian Business Cycle Theory and Global Crisis." Mises.org. Ludwig von Mises Institute, 5 Feb. 2010. Web. 29 Nov. 2010. <http://mises.org/daily/4072>. • "Effective Federal Funds Rate." St. Louis Federal Reserve. 2 Nov. 2010. Web. 29 Nov. 2010. <https://research.stlouisfed.org//fred2/data/FEDFUNDS.txt>. • "Flow of Funds Accounts of the United States." Federal Reserve. N.p., 17 Sept. 2010. Web. 29 Nov. 2010. <http://www.federalreserve.gov/releases/z1/Current/data.htm>. • Kliesen, Kevin. "The 2001 Recession: How Was It Different and What Developments May Have Caused It?" St. Louis Federal Reserve. N.p., Sept.-Oct. 2003. Web. 29 Nov. 2010.<https://www.research.stlouisfed.org/publications • Murphy, Robert. "Did the Fed, or Asian Saving, Cause the Housing Bubble?" Mises.org. Ludwig von Mises Institute, 19 Nov. 2008. Web. 29 Nov. 2010. <http://mises.org/daily/3203>.