Download

1 / 17

170 likes | 299 Views

OECD Views on Tax Competition: A Critical Appraisal. Montreal 17 September 2007 Richard J Hay STIKEMAN ELLIOTT LLP. Presentation Summary. key elements of tax competition OECD and the politics of tax competition “Harmful tax competition” OECD and tax havens

E N D

OECD Views on Tax Competition: A Critical Appraisal Montreal 17 September 2007 Richard J HaySTIKEMAN ELLIOTT LLP

Presentation Summary • key elements of tax competition • OECD and the politics of tax competition • “Harmful tax competition” • OECD and tax havens • DTAs as an antidote for the cross-border tax barriers

Elements of Tax Competition • rate • base (income or consumption, scope) • reach (worldwide or territorial) • model (redistributive?) • international interface

OECD • consensus process • 30 sovereign members • US / Europe are the principal constituencies • generally pro competition in its work • non-members are designated as “participating partners” in its work on tax competition

US Policy on Tax Competition • US states have long tradition of competition in tax / company law • US taxes are 27% of GDP • Europe averages 38% of GDP in tax • 2001: Republican criticism of OECD Harmful Tax Competition Initiative triggers change of policy (and Report name) • 2002-2004: US concern over corporate “inversions” into Bermuda

EU Policy on Tax Competition • diverse and complex • tax competition seen as compensation for geographic or structural differences (Madeira, Ireland, Luxembourg) • “offensive” or “defensive” measures? • EU “Code of Conduct” condemns “ring fencing” (contrast US / OECD position) • “salami slicing” is permitted • general low tax rates are acceptable (e.g. Ireland)

OECD Approach to Tax Competition • 1998: Harmful Tax Competition Report • concerns over “poaching” the tax base that “rightly” belongs to another country • countries are free to design their own tax systems… • “which abide by internationally accepted standards” • tax information exchange (on request)

“Harmful” Tax Competition • eroding the tax bases of other countries • diverting mobile investment from one country to another • “distorting” trade and investment patterns • failing to provide tax data for enforcement by other countries • project focus on information exchange by havens

OECD and Tax Havens • 1987: “Any country can be a tax haven in relation to a particular situation. Attempts to provide a definition are bound to be unsuccessful” • 1997: no or nominal taxes are a necessary (but not sufficient) indication of tax haven. Havens are identified and listed • 2002: commitments to transparency and information exchange • 2006: OECD Report on Level Playing Field

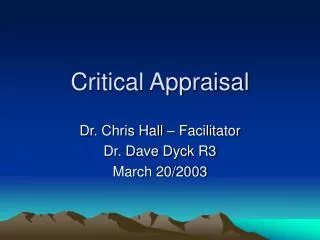

Top Global Economies, GDP per person2006 estimate, $‘000 SOURCE: CIA World Factbook

The Rap Sheet on “Tax Havens” • world tax rates are forced down by “unfair” tax competition • havens are predatory, distorting global economic activity • havens impoverish developed countries, jeopardising tax funding for public services • havens shift tax burdens from corporations to individuals

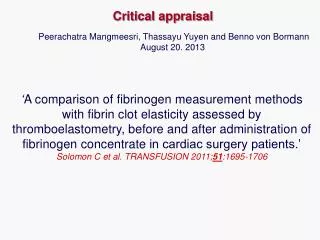

Corporate taxes% of GDP Average corporate tax rate* 4.0% 40% 3.5% 35% 3.0% 30% 2.5% 25% 2.0% 20% 1975 80 85 90 95 2000 05 Sources: OECD; Institute for Fiscal Studies *Unweighted average More for lessCorporate tax rates versus Revenues in developed countries

Tax Competition: Boon or Bane? • effective competitors are always an irritant to other market participants • competition is a healthy, liberalising force • tax competition promotes discipline and efficiency in public sector expenditure • does competition from low tax jurisdictions increase economic activity in neighbouring states?

Tax Competition and Double Tax Agreements • tax competition and barriers to cross border commerce • tax information exchange agreements vs. DTAs • will tax havens normalise relations with OECD states as they adopt international tax and regulatory standards? • should tax barriers be lowered for tax havens to permit full tax competition? • Canadian proposals are seen as novel and interesting

DTAs and Low / No Tax Jurisdictions • should OECD countries do DTAs with low/no tax centres? • the UAE experience • DTA relief is generally available between OECD countries for untaxed income in “participation” regimes, and for tax exempts • OECD may find it easier to work with its “participating partners” if there is an exchange of value

OECD and Tax Competition • “fair” tax competition is encouraged, but what is fair? • differing views in a complex political context • “level playing field” is a greater problem than anticipated • will OECD encourage its members to lower tax barriers for smaller countries as they facilitate tax information exchange?

QUESTIONS & ANSWERS Richard Hayrhay@stikeman.comSTIKEMAN ELLIOTT LLP | www.stikeman.com