Download

1 / 18

180 likes | 199 Views

Understand the relationship between REITs and portfolio diversification in Capital Asset Pricing Models, examining unique vs. systematic risk, market portfolios, and asset returns. Explore the benefits of REITs for diversifying investment portfolios.

E N D

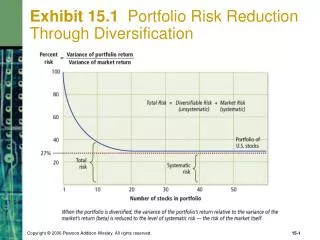

Capital Asset Pricing Models (CAPM) A. Risk compensation 1. unique vs. systematic risk 2. idiosyncratic vs. nondiversifiable B. Appropriate market portfolio 1. stock and/or bond markets typically used 2. real estate estimated to comprise 50% of US stock of wealth vs 20% for stocks • stock market risk may be diversifiable

C. market risk and beta 1. Rf = risk-free return 2. Rm = market return 3. Rre = real estate return

Definitions • Expected Portfolio Return (2 stocks): • Weighted average of each stock’s expected return.

Definitions • Portfolio Variance: • sum of share-weighted averages of the variances of stock returns plus the covariances among stock returns.

Definitions • Covariance: • absolute measure of the extent to which 2 stocks move together over time. • Positive Covariance - 2 assets move together • Negative Covariance - 2 assets move apart • Gives contribution of stock to overall portfolio risk

Definitions • Correlation: • relative measure of the extent to which 2 stocks move together. • Perfectly Positive = +1 • Perfectly Negative = -1

Definitions • Portfolio Variance – reprise

Portfolio Diversification • Now consider the “market” portfolio. • How many stocks are in the market? • Assume market composed of “N” stocks.

Portfolio Diversification • Out of the “N” stocks in the market, let’s assume that #2 represents the return on REITs. • How do you measure the REIT contribution to the overall portfolio risk? • Answer: Covariance

Portfolio Diversification • Let’s look at the “N” stock market variance/covariance matrix • Gives contribution of each stock to portfolio risk.

Portfolio Diversification • The Marginal Risk of REITs = • Covariance of REIT and market divided by overall market risk.

Portfolio Diversification • Note that:

Portfolio Diversification • Thus: Note:

Portfolio Diversification • So what’s the point? • Compound Annual Returns (1981-2001): • REITs 10.79% • S&P 500 11.59% • Russell 2000 11.44% • NASDAQ 11.18%

Portfolio Diversification • So what’s the point? • 20-year Standard Deviation of Annual Returns (1981-2001) • REITs 16.5% • S&P 19% • NASDAQ 29%

Portfolio Diversification • So, what’s the point? • Correlation: • REIT & S&P500 0.25 • REIT & NASDAQ 0.13 • REIT & Russell 2000 0.40

Portfolio Diversification • So, what’s the point? • REITs provide diversification benefits to portfolios.