Download

1 / 69

700 likes | 971 Views

Checking Account Simulation. Understanding Checking Accounts. What is a Checking Account?. Tool used to transfer funds deposited into the account to make a cash purchase Could also be named a transaction account Common financial service used by many consumers Available at banks.

E N D

Checking Account Simulation Understanding Checking Accounts

What is a Checking Account? • Tool used to transfer funds deposited into the account to make a cash purchase • Could also be named a transaction account • Common financial service used by many consumers • Available at banks

Checking Accounts continued • Services and fees will vary depending upon the financial institution • Research the financial institution and type of account before choosing • Many financial institutions offer telephone and internet banking services to customers

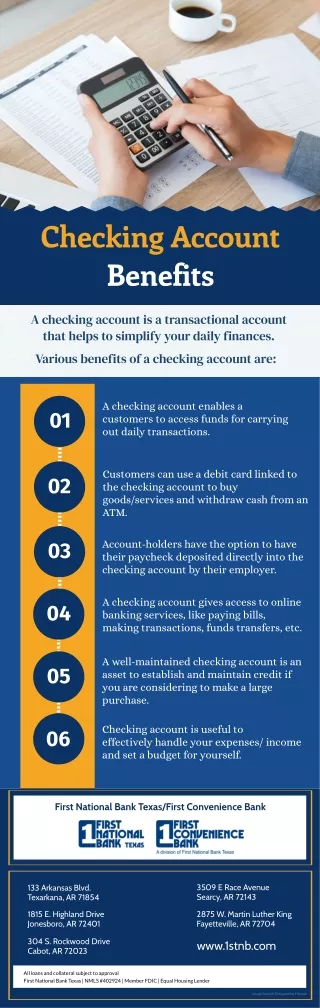

Benefits • Can help to manage money • Written record of expenses • Check register • Makes bill paying more convenient • Reduces the need to carry large amounts of cash • Most liquid of cash management tools • Considered cash

How Do They Work? • Money is deposited into the account with a deposit slip • Pay the transaction by: • Writing a check • Using an ATM and/or debit card • Using electronic banking

Characteristics • Funds are easily accessible through: • A check • Automated teller machine (ATM) • Debit card • Telephone • Internet

Piece of paper pre-printed with the account holder’s: Name Address Financial institution Identification numbers To completed check, fill in the: Amount Payee To whom the check was written Date Signature What is a Check? • Used at the time of purchase as the form of payment

Bouncing a Check • Check written for an amount over the current balance held in the account • ‘Bounces’ due to insufficient funds • Assessed a substantial fee by both the financial institution and the payee • Can cause harm to credit report • Financial institutions report to credit bureaus the account holder’s failure/success to manage his/her checking account properly • Used as a guide for future inquiries for credit

Other Checking Components • Register • Place to immediately record all monetary transactions for a checking account • Written checks, ATM withdrawals, debit card purchases, deposits, fees, etc. • Checkbook • Contains the checks and the register to track monetary transactions

ATM Fees • ATMs are owned by different financial institutions • Fees may be charged to the account for ATM use • Fees range from $0.50 to $5.00 • Usually free to account holders of the financial institution

ATM Card • Card given to account holder to make financial transactions at ATMs • In the shape of a credit card, but can only be used in designated places • Must use personal identification number (PIN) to access the account • A protected number given or chosen by the account holder to allow access to the account

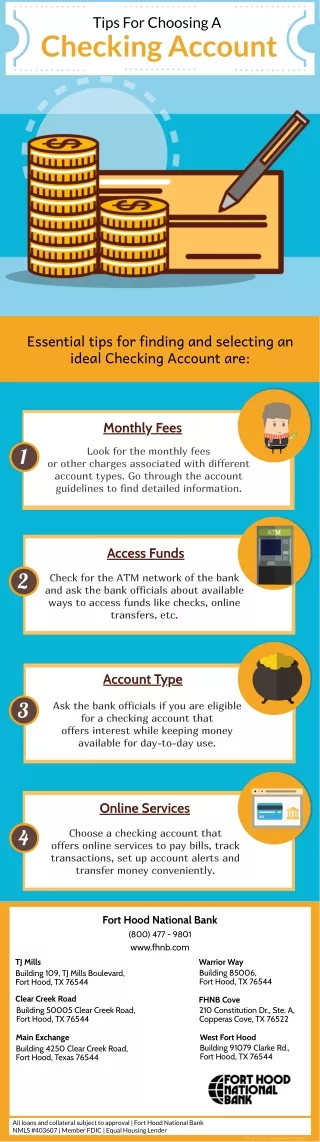

Types of Accounts Available • Financial institutions offer different types of checking accounts • All have own characteristics • Research all of the requirements and restrictions before opening the account • Basic types/guidelines include: • Regular checking • Free checking • Special checking • Interest-Earning checking

Regular Checking • No monthly charge if minimum balance is maintained • No interest is given • Unlimited check writing

Free Checking • No charges or fees for using the account • No minimum balance required • Unlimited check writing • Usually for a specific group: • Students • Seniors

Special Checking • Generally for people who write only a few checks and keep a low balance • Basic account which pays no interest • Monthly service charge or fee for each transaction • May have restrictions on number of transactions each month

Interest-Earning Checking • Pays interest on money in account • Usually the lowest interest rate of all the cash management tools • Minimum balance required • Unlimited check writing • Called a share draft at credit unions

Opening a Checking Account • Most applications are completed on a computer to process quickly • Customer may have to complete a brief hand-written application to be entered into the computer by new accounts personnel • Customer must have: • Picture identification • Name, address, phone number, and social security number

Opening continued • If customer is approved, he/she completes a signature card • Contains account information about the new account and his/her signature • Used to verify the signature for each signed transaction for the account to prevent fraud • Completion of the signature card means the customer agrees to all terms and conditions of the account

Opening continued • If offered, customers may choose to have an ATM and/or debit card for the account • May be required to complete another form • An initial deposit must be made • Amount will vary among different financial institutions and type of account

Ordering Checks • New customers are provided starter checks to use until the ordered checks arrive • Generic checks with account number and financial institution pre-printed • Customer information is hand written • Many businesses do not accept starter checks • Take this into consideration before making the initial deposit • Ordered checks may take 5 to 10 business days to arrive

Ordering continued • Personal information on checks • Name • Address • Optional: phone number, driver’s license number • DO NOT put the account holder’s social security number on the check for security reasons

Ordering continued • Design of the check is customer’s choice • Customer pays for checks • Price depends on the style • Style of the check does not change how a check works • Some financial institutions may offer basic checks free of charge • Single or duplicate checks are available

No records of written checks Each check must be logged in the register immediately to track transactions Provides a written record of each check with the carbon copy Convenient in case the check was not recorded into register immediately Ordering continued SingleDuplicate(carbon copy)

Endorsing a Check • Endorsement • Signature on the back of the check from receiving person approving it for deposit • A check must be endorsed to be deposited • Three types • Blank • Restrictive • Special • Safest way to endorse the check is to wait until going to the financial institution to deposit or cash the check

Blank Endorsement • Receiver of the check signs his/her name • Anyone can cash or deposit the check after has been signed

Restrictive Endorsement • More secure than blank endorsement • Receiver writes “for deposit only” above his/her signature • Allows the check to only be deposited

Special Endorsement • Receiver signs and writes “pay to the order of (fill in person’s name)” • Allows the check to be transferred to a second party • Also known as a two-party check

Making a Deposit • Deposit slip • Contains the account holder’s account number and allows money (cash or check) to be deposited into the correct account • Located in the back of the checkbook • Complete a deposit slip to make a deposit • Give to financial institution along with cash and/or check • Checks must be endorsed to be deposited • Deposited amount must be recorded in the check register to keep the balance current

Completing a Deposit Slip • Date • The date the deposit is being made

Completing a Deposit Slip • Signature Line • Sign this line to receive cash back

Completing a Deposit Slip • Cash • The total amount of cash being deposited

Completing a Deposit Slip • Checks • List each check individually • Identify each check on the deposit slip by abbreviating the name of the check writer

Completing a Deposit Slip • Checks • If more checks are being deposited than number of spaces on the front, use the back • List each check • Add the total, enter it on the front

Completing a Deposit Slip • Total from Other Side • The total amount from all checks listed on the back

Completing a Deposit Slip • Subtotal • The total amount of cash and checks

Completing a Deposit Slip • Less Cash Received • The amount of cash back being received • This amount is not deposited into account

Completing a Deposit Slip • Net Deposit • The amount being deposited into the account • To calculate the amount, subtract the cash received from the subtotal

Writing a Check • To pay for items using a checking account • A check is given as a form of payment • Must be completed and given to the person or business • Pre-printed items on a check • Name and address of account holder • Name and address of financial institution • Check number • Identification numbers (account, routing)

Writing a Check • Personal Information • Account holder’s name and address • May include a phone number, not required • DO NOT list a social security number for safety reasons

Writing a Check • Check Number • Numbers used to identify checks • Printed chronologically

Writing a Check • Date • The date the check is written

Writing a Check • Pay to the Order of • The name of the person or business to whom the check is being written

Writing a Check • Amount of the Check in Numerals • The amount of the check written numerically in the box • Write the cents smaller and underline • Write the numbers directly next the dollar sign to prevent someone else from adding numbers to change the amount

Writing a Check • Amount of the Check in Words • The amount of the check written in words on the second line • Start at the far left of the line, write the amount in words, followed by ‘and’, and the amount of cents over 100; draw a line from the end of the words to the word ‘dollars’

Writing a Check • Memo • Space used to identify the reason for writing a check; optional • Good place to write information requested by a company when paying a bill, generally the account number

Writing a Check • Signature • The account holder’s signature agreeing to the transaction

Writing a Check • Identification Numbers • First - routing numbers to identify the account’s financial institution • Second - account number • Third - check number

Check 21 • Check Clearing for the 21st Century Act (Check 21) • Current trend that changes how money is withdrawn from customers account and deposited into businesses account

How Check 21 Works • Prior to Check 21 • Paper checks physically moved from customer to business to various banks and the transfer of money from customer’s bank to business’ bank took days • After Check 21 • Paper checks are scanned into a computer system at the place of business and immediately returned to the customer. This electronic copy of the check is called a substitute check. The substitute check is then transferred electronically to various banks and the transfer of money customer’s bank to business’ bank takes hours