Download

1 / 0

0 likes | 157 Views

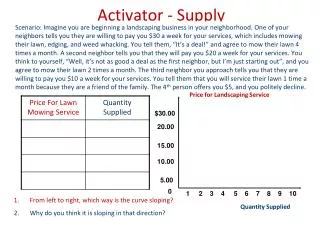

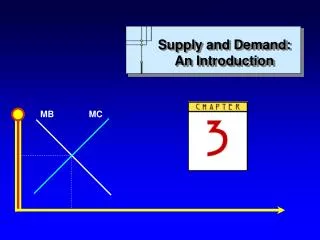

Ch. 5: Supply. Sec. 1: What Is Supply?. Supply- anyone who provides goods & services is a producer manufacturers, farmers, airlines, utility comp., pet sitter Key words – if prices to low – some not willing to take on expense of growing and transport

E N D