Download

1 / 55

670 likes | 1.12k Views

CHAPTER 16 Auditing the Production and Personnel Services Cycle Spring 2007. Production Cycle. Debit Credit. Merchandise Inventory Raw Materials Inventory Purchases Mfg. Overhead Direct Labor Indirect Labor. Accounts Payable Payroll Payable.

E N D

CHAPTER 16 Auditing the Production and Personnel Services Cycle Spring 2007

Production Cycle DebitCredit Merchandise Inventory Raw Materials Inventory Purchases Mfg. Overhead Direct Labor Indirect Labor Accounts Payable Payroll Payable

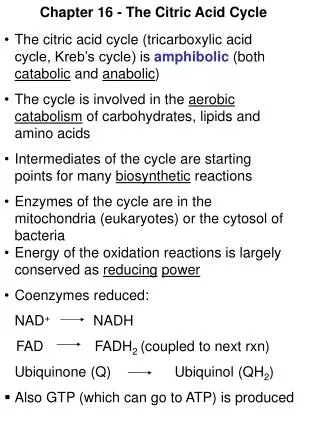

Expenditure Transaction Classes and Accounts: Cash Disbursement & Adjustments DebitCredit Accounts Payable Payroll Payable Cash

Production Cycle Raw Material Direct Labor Work In Finished Cost of Process Goods Sales BS BS IS Overheads Sale Trans

General Audit Strategy • Assess Inherent Risk • Use Knowledge of Business and Industry to Perform Analytic Procedures and Assess Analytic Procedures Risk • Assess Control Risk • Evidence of effectiveness gained while obtaining an understanding of internal controls • Evidence of effectiveness of management controls • Evidence of effectiveness from direct tests of programmed controls • Design Appropriate Substantive Tests of Details

Production Cycle: Initial Audit Procedures Understanding Business Aspects of Cycle • Who are key suppliers? • What is the manufacturing process? • What is the relative proportion of costs in the manufacturing process? • Materials • Labor • Overheads • What is the company’s competitive advantage? • What is a normal inventory turn?

Production Cycle: Initial Audit Procedures Cost Structure (Fixed vs. Variable Cost) • How much does costs of goods sold change as sales change? • High fixed costs and low variable cost create a significant contribution margin after fixed costs have been achieved – Economies of Scale. Reverse also in effect. • Low fixed cost and high variable cost represents a higher correlation between Sales and COGS fluctuations – Profit fluctuations are minimized.

Production Cycle: Initial Audit Procedures • Consider Management Incentives to Manage Earnings through Inventory and COGS • Methods related to the Production Cycle • Physical inventory counts • Special sales relationships • Inventory costing • Reserves • Write-offs

Production Cycle: Initial Audit Procedures Analytical Procedures • Inventory turnover • Inventory growth to cost of sales growth • Finished good produced to raw materials used • Finished goods produced to direct labor • Product defects per million

Assertion Completeness Existence & Occurrence Valuation Rights and Obligations Presentation and Disclosure Specific Audit Objective Completeness Cutoff / Timeliness Validity Cutoff / Timeliness Valuation at Historical Cost / GAAP Valuation at Net Realizable Value Posting and Summarization Ownership Classification Disclosure Production Cycle Audit Objectives

Production Cycle: Initial Audit Procedures • Understand what controls are in place to ensure these audit objectives are being met. • See flowchart 16-5 on page 751

Production Cycle: Understand (and maybe test) Internal Controls Control Environment • Assignment of Authority and Responsibility • Accountability • Control consciousness relative to the value and portability of inventory. • Involvement of the internal audit function in review of: • The existence of inventory • The complete recording of all inventory transactions • The valuation of inventory

Production Cycle: Understand (and maybe test) Internal Controls Mgmt Risk Assessment • How management monitors ability to meet cash flow requirements • How management monitors inventory shrinkage • How management controls manufacturing costs • Impact of cost increases on entity

Documents Production order Materials issues slips Time ticket Move ticket Daily production reports Completed production reports Files Perpetual inventory files Raw Materials WIP Finished goods Standard cost master file Production Cycle: Understand (and maybe test) Internal Controls Information System

Production Cycle: Understand (and maybe test) Internal Controls We also need to know… • Reports: • Reports used in decision making • Exception reports • Understand how reports are used to manage and control the entity • Timeliness of review of reports • Business decisions made with reports • Follow-up on issues raised in reports

Assessing Controls • Determine first if general controls are adequate • Are there controls that address the necessary audit objective • Once you have assessed which controls you are looking for and client says they are in place, then they can be tested (often using sampling)

Production Controls (completeness) Completeness • Establish initial control over inventory through prenumbered production orders, materials issue slips, time slips, etc. • Compare quantities of material and labor used in the manufacturing process, with final production and expected value of final production given input. • Inventory move tickets are accounted for • Management review of quantity variance

Production Controls (completeness) Cutoff • Computer should ensure recording of transactions at the appropriate time • The most important cutoff issues are the date received (compared to the date the purchase is recorded) and the date shipped (compared to the date the sale is recorded). • Secondary issue of transfer from raw materials to work in process (based on material requisition) and work in process to finished goods (based on completed production report).

Production Controls (existence) Validity • Company should maintain perpetual inventory • Periodically count inventory and compare with perpetual records • Annual counts v. Cycle counts

Production Controls (valuation) Valuation at Historical Cost • Costing process of RM, WIP and FG is based on move tickets • Exception report compares actual cost with standard or expected costs Valuation at N.R.V. • Track each item in finished goods inventory • Report of slow moving goods in inventory • Report comparing sales prices, margins, and costs for each item in f/g inventory

Production Controls (valuation) Posting and summarization • Run to run totals • Inventory reconciliations • At month end, sum of individual items in inventory x cost of item should match general ledger

Production Controls (rts & oblig) Ownership • Controls over consignment goods • Perpetual inventory of consignment in - count • Perpetual inventory of consignment out – regular confirmation or count at customer site • Inventory held at off-site locations – how is it accounted for? Reconciled?

Production Controls (pres & discl) Classification • Move tickets/time tickets and production reports should provide the basis for determination of work in process and finished goods. • All move tickets/time tickets should be accounted for on a regular basis. Disclosure • The auditor rarely finds controls over disclosure and must test substantively

Inventory: Determining Detection Risk How much substantive tests of details? • Determine detection risk for each audit objective based on audit risk model after assessing: • Inherent risk • Control risk • Risk that analytic procedures would fail to detect material misstatements.

Inventory: Standard Substantive Tests Initial procedures • Agree/tie-out beginning balance to prior year workpapers • Agree/tie-out ending balance of perpetual records or other inventory schedules to the current period general ledger

Inventory: Standard Substantive Tests Analytical Procedures • Perform detailed AP, typically by product or line (“disaggregated analytics”) • Calculate the number of days it takes to turn inventory. • Compare sales to anticipated sales volume. • Determine proportion of variable and fixed costs. • Determine cost, volume, and profit relationships. • Compare company performance with industry (inventory turnover and profitability).

Inventory: Physical Inventory Observation • What does the Physical Inventory Observation give us comfort over? • Existence/Validity/Cut-off • Completeness/Cut-off • Valuation • Ownership

Inventory: Physical Inventory Observation Physical Inventory Observation Year End Inventory Observation Subsequent tests of Recording of Inventory What if the inventory observation takes place at a date different than year end? Must perform rollforward/rollback testing.

Observation Obtain a list of all tag numbers (or other count media) used and not used to count inventory. Observe warehouse and ascertain that all inventory was counted. Subsequent Tests Trace test counts into the final inventory accumulation. On a test basis compare count media used in physical inventory to recording on final inventory valuation report. Inventory: Physical Inventory Observation Physical Inventory Observation: Completeness

Observation Obtain a list of the last shipments and last receivings for 3 to 10 days prior to cutoff date. Subsequent Tests Check cutoff for sales and purchases based on cutoff information obtained during inventory observation. Inventory: Physical Inventory Observation Physical Inventory Observation: Cut-off

Observation Obtain a list of all tag numbers (or other count media) used and not used to count inventory. Check the accuracy of the client’s inventory counts on a test basis. Subsequent Tests Trace sample of items from final inventory accumulation to count sheets Confirm inventory in public warehouse, etc. On a test basis compare final inventory valuation report to count media used in physical inventory. Inventory: Physical Inventory Observation Physical Inventory Observation: Existence/Validity

Observation Test counts Subsequent Tests Recalculate totals and extensions of inventory quantities times price. Examine vendor’s invoices, production cost calculations, etc. supporting prices for inventory items on a test basis. Inventory: Standard Substantive Tests Physical Inventory Observation: Valuation

Observation Look for indications of slow-moving, damaged, or obsolete inventory. Subsequent Tests Review inventory turnover by stock number Compare inventory costs with sales prices subsequent to year end Inventory aging Make judgment about the adequacy of inventory obsolescence reserve Inventory: Standard Substantive Tests Physical Inventory Observation: Valuation @ NRV

Inventory: Standard Substantive Tests Physical Inventory Observation: Posting and Summarization • Reconcile physical inventory counts to the ending inventory balances. Significant reconciling items should be tested.

Observation Inquire about consignments in / out Observe the counting of consignment-in inventory Subsequent Tests Examine consignment agreements and contracts Ascertain that consignment-in inventory is not counted in valuation Confirm consignment-out inventory with customer Inventory: Standard Substantive Tests Physical Inventory Observation: Ownership

Observation Ascertain that physical inventory clearly and correctly identifies quantities of raw materials, work in process, and finished goods inventory. Subsequent Tests Vouch inventory classification to information obtained during inventory observation. Inventory: Standard Substantive Tests Physical Inventory Observation: Classification

Inventory: Standard Substantive Tests Disclosure • Physical Inventory observation is not useful • Instead, at the end ascertain that all financial statement disclosures are present by reference to disclosure check list.

Personnel Services Cycle DebitCredit Direct Labor Indirect Labor Some Other Expenses Payroll Payable Payroll Taxes Payable

Personnel Services Cycle:Key Issues • How important is labor to the organization? • Software company • Education • Sales vs. Manufacturing? • How automated is the manufacturing process? • Handcrafted goods • Mass produced goods

Personnel Services Cycle: Understand (& maybe test) Internal Controls Control Environment • Accountability & Hiring practices • Control consciousness regarding personnel function, initiating new individuals on payroll, and care with payroll changes. Mgmt. Risk Assessment • Control over new employees • Number of classes of employees • Different types of compensation agreements? Hourly, Salary, Number of pay ranges? • System design to capture various compensation agreements

Documents Personnel authorization Time cards / tickets Payroll register Payroll checks Labor cost distribution summary Payroll tax returns Files Personnel data master file Employee earnings master file Payroll transaction file Personnel Services Cycle: Understand (& maybe test) Internal Controls Information System

Personnel Services Cycle: Understand (& maybe test) Internal Controls We also need to know… • Reports: • Reports used in decision making • Exception reports • Understand how reports are used to manage and control the entity. • Timeliness of review of reports. • Business decisions made with reports. • Follow-up on issues raised in reports.

Personnel Services Cycle: Key Functions • Personnel Department • Authorizes new individuals • Authorizes salary / rate changes • Review of all personnel and rate changes

Personnel Services Controls (Completeness) Completeness • Establish initial control over time cards, etc. • Computer match of time cards with P/R transactions, & generate exception reports for differences. • Computer match of P/R transactions w/ # of expected salary transactions, & generate exception report of differences. Cutoff • May be a problem if pay period differs from year end. • Management (controller) review of payroll and develop accrual entry for accrued payroll.

Personnel Services Controls (Existence) Validity • Personnel department controls employee master file (new employees on master file). • Employee number with check digit. • Batch total compares payroll with expected number of payroll transactions.

Personnel Services Controls (Valuation) Valuation at historical cost • Limit test on individual payroll transactions • Batch totals on total hours Valuation at N.R.V. • N/A Posting and Summarization • Run to run totals • JE of accrual

Personnel Services Controls (Valuation) Classification • Management review of payroll charged to budget area • Accounting department review of payroll accruals Disclosure • Tested through substantive tests

Personnel Services: Determining Detection Risk • Set detection risk based on: • Inherent risk (usually low for understatement) • Control risk • Results of analytic procedures

Personnel Services: Standard Substantive Tests Initial substantive procedures • Determine detail for accrued payroll liabilities and agree to general ledger. • Best way to test accrued payroll is to vouch the subsequent payment.

Personnel Services: Standard Substantive Tests Analytical Procedures (lots of good ones!!!) • Payroll cost as a percent of sales; compare with industry data • Sales / Revenue per employee; compare with industry data • Payroll expense per employee • Changes in payroll costs per store/division • Compare headcount changes to knowledge of business & industry • Compare key payroll data with prior year or budget • Compare accruals with prior year (consider changes in volume of activity)