Download

1 / 6

60 likes | 263 Views

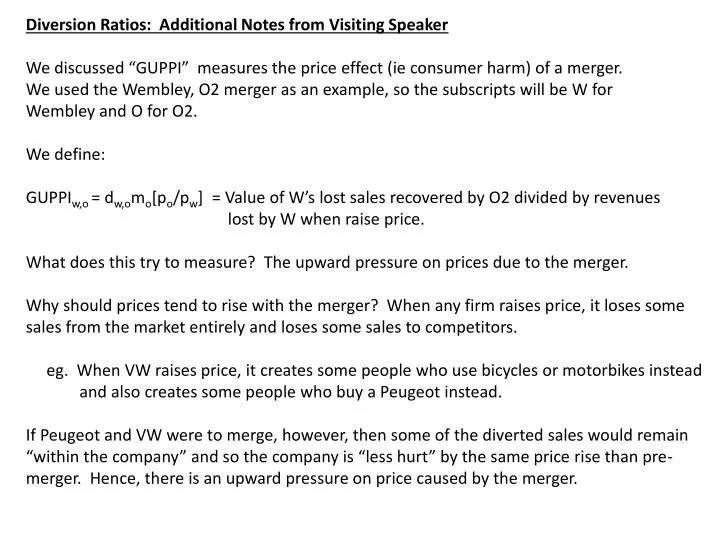

Diversion Ratios: Additional Notes from Visiting Speaker We discussed “GUPPI” measures the price effect ( ie consumer harm) of a merger. We used the Wembley, O2 merger as an example, so the subscripts will be W for Wembley and O for O2. We define:

E N D

Diversion Ratios: Additional Notes from Visiting Speaker We discussed “GUPPI” measures the price effect (ie consumer harm) of a merger. We used the Wembley, O2 merger as an example, so the subscripts will be W for Wembley and O for O2. We define: GUPPIw,o= dw,omo[po/pw] = Value of W’s lost sales recovered by O2 divided by revenues lost by W when raise price. What does this try to measure? The upward pressure on prices due to the merger. Why should prices tend to rise with the merger? When any firm raises price, it loses some sales from the market entirely and loses some sales to competitors. eg. When VW raises price, it creates some people who use bicycles or motorbikes instead and also creates some people who buy a Peugeot instead. If Peugeot and VW were to merge, however, then some of the diverted sales would remain “within the company” and so the company is “less hurt” by the same price rise than pre- merger. Hence, there is an upward pressure on price caused by the merger.

Derivation of GUPPI Let Qw (Po,Pw) = demand function of Wembley (pre-merger) Qo (Po,Pw) = demand function of O2 (pre-merger) A Wembley price increase raises O2’s pre-merger sales, and the firm gets a profit margin on each of these sales. Hence, the “benefit” to the O2 of Wembley’s lost sales is: Where the marginal cost of O2 is co. And the revenues lost by Wembley when it raises its price are: In other words, the revenue effect on Wembley is the product of the lost sales and the price on each of these sales.

The ratio of these two quantities is the GUPPI: = } {} = = diversion ratio (of total sales decrease of Wembley that are recovered by new partner) X margin on sales X price ratio.

π P**w P*w Price Pre-merger optimum Post-merger optimum The GUPPI essentially measures the slope of the profit function at the pre-merger point. The larger is the slope, the farther to the right the post-merger price will lie. The problem is that the GUPPI doesn’t tell us exactly how far to the right the new price will lie. This is because the shape of the profit function matters…and the GUPPI only reflects the local shape. The merger may create a large change, though. In practice, linear demands often are used. In this case a 5-10% GUPPI will be enough to generate sufficient price rises that merger will be viewed as problematic (causing a 5% or greater rise in price.)

A full-fledged merger simulation (as we discussed earlier in term with fish and shampoo) would give an idea of the precise shape of the profit function…but is costly. Hence, GUPPIs are used to get a first look at whether a full simulation model would be worth the cost. If the GUPPI is too high (5% or more) then probably not… Wembley specifics Ancillary Income: If O2 has ancillary activities (like restaurants and parking) then the profit margins at the O2 may be, effectively, higher than otherwise would be. This tends to raise the mo term in our expression for the GUPPI. If this term rises, then we should expect the post-merger price rises at Wembley to be *larger* than the basic GUPPI predicts. We could formalise this idea as follows: Pre-merger, Wembley maximises (WRT Pw) : Post-merger, Wembley maximises (WRT both P) : + Where Δμo = ancillary sales from services at the venue.

We can manipulate the first order condition with respect to Pw to get the modified GUPPI that is appropriate to this case. The modified GUPPI behaves quite differently: To get the 5% “modified” GUPPI that is the “trigger” for a negative evaluation by competition authorities, and for an ancillary profit measure of £10k per event, for example, to get a 5% upward price pressure, we would need a “basic” GUPPI Of 11%. And for an ancillary profit of £40k per event, we would need a “basic” GUPPI of 39% to get a 5% upward price pressure. The intuition is that the ancillary revenues create an incentive for the firms to price the event low in order to pull customers in and then profit from the ancillary services. Hence, the change in business model projected for Wembley to ancillary service revenue from solely event revenue will tend to create a downward pressure on event prices. Factoring this into the upward price calculation makes a big difference to how much we predict the O2-Wembley merger will affect ticket prices for customers.