Download

1 / 32

320 likes | 491 Views

Business Entity Formations. Nema Koohmaraie and Matt Hinrikus UNL College of Law – Entrepreneurship Legal Clinic. Disclaimer.

E N D

Business Entity Formations Nema Koohmaraie and Matt Hinrikus UNL College of Law – Entrepreneurship Legal Clinic

Disclaimer • The content of this presentation is intended solely as a brief summary of entity choices available to individuals starting a business operation. The information provided during this presentation shall not be construed as legal advice • We are not tax experts. Consult your accountant or tax attorneys to supplement the tax considerations

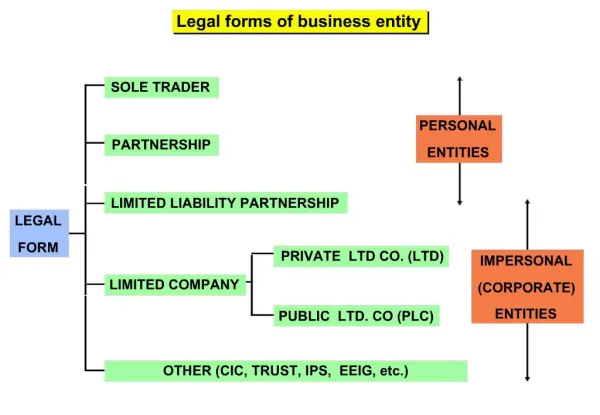

Discussion Points • Overview of Business Entity Structures • Benefits & Values of Entity Formation • Types of Entities • Sole Proprietorship • Partnership – General or Limited • Corporation – C-Corp. or S-Corp. • Limited Liability Company (LLC) • Differences

Benefits of Entity Formation • Corporate Shield – a.k.a., liability protection • Appearance of Legitimacy • Means to raise capital from outside investors • Method of combining valuable assets • E.g., intellectual property • Business continuity and planning

Sole Proprietorship • Composed of one individual who owns and operates a business – Default entity • No separation or distinction as between the owner and the business • No statutory requirements to create • Trade Name Application if going to conduct business in something other than the name of the owner • Applicable licenses or permits

Sole Proprietorship • Taxation • Owner of the business reports income or loss directly on his or her personal income tax return • Liability of Owner • Owner of the business is personally liable for debts & obligations of business and for negligent acts committed by themselves and their employees if acting within the scope of employment

Partnerships • An association of two or more persons to carry on a business for profit as co-owners • Two Types • General Partnership • Limited Partnership

General Partnership • Partnership Formation • Default entity • Automatically forms when two or more individuals are carrying on a business for profit as co-owners • Operations • Partnership Agreement; OR • Revised Uniform Partnership Act (governing law)

General Partnership • Taxation • Partnership files an informational income tax return, but the Partnership itself does not pay income taxes • Pass-Through Entity • Income or loss is attributed to the owners/partners equally • Note: Sharing of profits or losses can be determined by the Partnership Agreement

General Partnership • Liability of Owners/Partners • Shared liability by all partners • Joint and Several • Any one partner can bind other partners • Contract • Negligence

General Partnership • Advantages • Simple and Inexpensive to create • Partners report their share of profits or losses on their own income tax return • Disadvantages • Partners are personally liable for debts & obligations of the business

Limited Partnership • Formation • Must file a Certificate of Limited Partnership with Secretary of State • Operations – Two Types of Partners • General Partners: Active investor and actively involved in the day to day operations and management • Limited Partners: Do not participate in day to day operations and management – passive investors

Limited Partnership • Taxation • Based on value of individual contributions • Tax liability is not equal among partners • Liability of Owners/Partners • General Partners: Subject to personal liability for debts & obligations of business (similar to General Partnership) • Limited Partners: Not subject to personal liability for debts & obligations of business

Limited Partnership • Advantages • Limited partners are not personally liable for business debts (generally) • General partner can raise capital from the passive investors (limited partners) without giving up management in business • Disadvantages • General Partners are personally liable for business debts

Alternatives • Is there a way to limit the liability of all owners while allowing easy transferability of ownership interests? • YES – Corporations or Limited Liability Companies

Limited Liability Entities • Our purpose today Corporations or LLCs • Legal entity, separate & distinct from the owners • Created by statutory law • Limited liability of business owners • Not liable for debts incurred by the business • Unless exceptions apply – Piercing Corporate Veil

Requirements • Must file with the Nebraska Secretary of State • Articles of Incorporation (Corporations) • Certificate of Organization (LLCs) • Must draft and execute – governing document • Corporate Bylaws (Corporations) • Operating Agreement (LLCs)

Limited Liability Entity or Not • Increased Likelihood of incurring liability • Selling products or services • Hiring more employees • Entering into contracts – e.g., leases, loans, sales • Multiple owners • Additional investors

Corporation or LLC • Things to Consider: • Financing needs • Investors, Venture Capitalists, Angel Capitalists tend to prefer corporation status • Management • Board of Directors & Officers (Corporations); OR • Member- or Manager-Managed (LLCs) • Tax & Liability

Corporations • Corporate law is state law • Approx. 50% of corporations incorporate in Delaware • Internal Affairs Rule: the laws of the state of incorporation govern internal corporate affairs • Foreign Business Rule: if incorporated in a state other than where conducting business, must qualify/register to operate business in the “foreign” jurisdiction

Corporations • Operations • Shares of Stock = Ownership Interest = Shareholder • Board of Directors = primary decision makers • Election process is established in the Articles or Bylaws • Can reserve certain decision-marking authority to Shareholders • Officers = day to day decision makers • Elected by Board of Directors • President, VP, Secretary, Treasurer, etc.

Corporations • Liability of Owners/Shareholders • Separate legal entity, distinct from Owner/Shareholders • General Rule: Entity is liable for corporate debts & obligations • Exceptions: • Piercing the Corporate Veil (PCV) • Personal Contractual Guarantees

Corporations • Two Choices: • C-Corporations (C-Corp.) • S-Corporations (S-Corp.)

C-Corporation • Taxation • Double Taxation • First, taxed at the corporate level – corporation reports and pays income taxes • Second, taxed at the individual level – shareholders report and pay income tax on any distributions paid out to them

S-Corporation • Corporation that makes a valid election to be taxed under Subchapter S of Chapter 1 of the Internal Revenue Code • File Form 2553 • Taxation • Pass-Through • No taxation at corporate level • Only taxed at individual level if shareholders are paid distributions

S-Corporation • Restrictions on S-Corporation • Domestic Corporation • Allowed only 1 class of stock • Maximum of 100 shareholders • Shareholders must be U.S. citizens or residents • Profits and Losses allocated proportionately

Limited Liability Company • Flexible structure: Can take the form of a General Partnership, but provides the limited liability of a corporation • Formation • Must file Certificate of Organization with Nebraska Secretary of State

Limited Liability Company • Operations • Operating Agreement (governing contract) • Nebraska Limited Liability Company ct (governing law) • Management Structure • Member-Managed – Default • All members (owners) have decision-making authority in day to day operations of business • Manager-Managed • Must be elected in the Operating Agreement • Decision-making authority is given to one or more persons

Limited Liability Company • Taxation – various possibilities • Default: Pass-Through entity • Election • C-Corporation treatment: taxed at corporate and individual levels; OR • S-Corporation treatment: Pass-Through entity • Liability • Neither members or managers are subject to personal liability for debts & obligations of business

Limited Liability Company • Advantages • Owners have limited liability for business debts even if they participate in management of the business • Profit and Loss can be allocated differently than ownership interest • Choice of taxation structure • Disadvantages • More expensive to create than a Partnership or Sole Proprietorship

Summary • Business Entity Formation matters greatly • Tax Implications • Liability of Owners • Future Financing & Investor Preference • Internal Operations • Default Rules

Contact Us • Write us: Entrepreneurship Legal Clinic University of Nebraska College of Law 7 McCollum Hall Lincoln, NE 68583-0902 • Give us a call: 402-472-1680 • Visit our website: http://law.unl.edu/eclinic