Download

1 / 1

10 likes | 84 Views

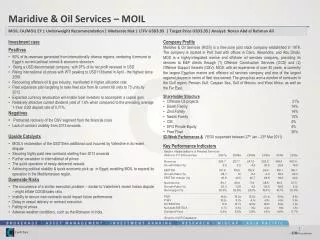

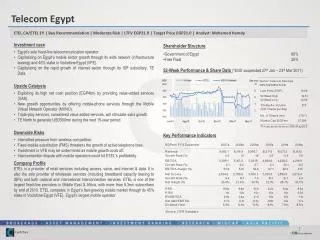

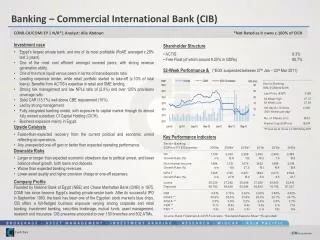

Lecico Egypt. LCSW.CA/LCSW EY | Buy Recommendation | Moderate Risk | LTFV 21.8 EGP | Target Price EGP21.4 | Analyst: Yasmin Ghanem. Investment case Internationally competitive business model with a geographically diverse sales portfolio of over 55 countries.

E N D

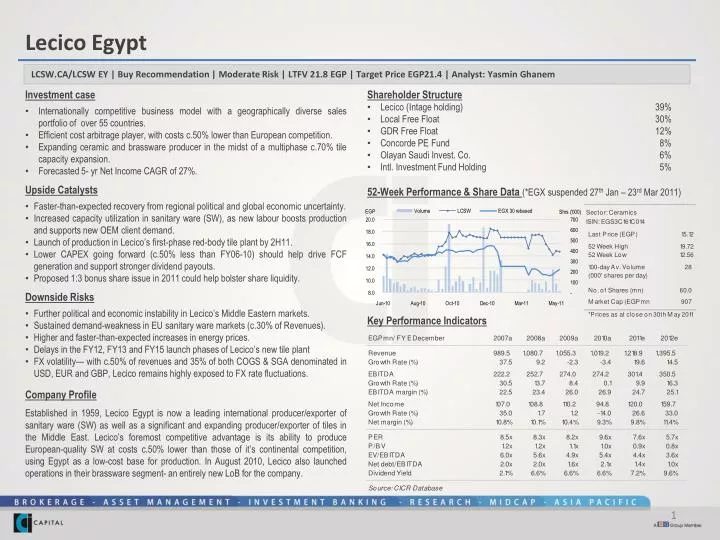

Lecico Egypt LCSW.CA/LCSW EY | Buy Recommendation | Moderate Risk | LTFV 21.8 EGP | Target Price EGP21.4 | Analyst: Yasmin Ghanem Investment case • Internationally competitive business model with a geographically diverse sales portfolio of over 55 countries. • Efficient cost arbitrage player, with costs c.50% lower than European competition. • Expanding ceramic and brassware producer in the midst of a multiphase c.70% tile capacity expansion. • Forecasted 5- yr Net Income CAGR of 27%. Upside Catalysts • Faster-than-expected recovery from regional political and global economic uncertainty. • Increased capacity utilization in sanitary ware (SW), as new labour boosts production and supports new OEM client demand. • Launch of production in Lecico’s first-phase red-body tile plant by 2H11. • Lower CAPEX going forward (c.50% less than FY06-10) should help drive FCF generation and support stronger dividend payouts. • Proposed 1:3 bonus share issue in 2011 could help bolster share liquidity. Downside Risks • Further political and economic instability in Lecico’s Middle Eastern markets. • Sustained demand-weakness in EU sanitary ware markets (c.30% of Revenues). • Higher and faster-than-expected increases in energy prices. • Delays in the FY12, FY13 and FY15 launch phases of Lecico’s new tile plant • FX volatility— with c.50% of revenues and 35% of both COGS & SGA denominated in USD, EUR and GBP, Lecico remains highly exposed to FX rate fluctuations. • Shareholder Structure • Lecico (Intage holding) 39% • Local Free Float 30% • GDR Free Float 12% • Concorde PE Fund 8% • Olayan Saudi Invest. Co. 6% • Intl. Investment Fund Holding 5% • 52-Week Performance & Share Data (*EGX suspended 27th Jan – 23rd Mar 2011) Key Performance Indicators Company Profile Established in 1959, Lecico Egypt is now a leading international producer/exporter of sanitary ware (SW) as well as a significant and expanding producer/exporter of tiles in the Middle East. Lecico’s foremost competitive advantage is its ability to produce European-quality SW at costs c.50% lower than those of it’s continental competition, using Egypt as a low-cost base for production. In August 2010, Lecico also launched operations in their brassware segment- an entirely new LoB for the company.